Today I found a way to help increase my returns - here's how

The following post is geared to Tax Lien investing, but it also shows how you can keep your eyes out for data that can help you gain an edge in investing by applying what a new data source can provide.

In tax lien investing, the majority of the liens are redeemed (paid off) by the owner. So the majority of tax lien investors are looking for the interest rate return.

Unlike Certificates of Deposit or Bonds, an investor in liens never knows when the property owner will pay off the lien. Trying to determine an expected rate of return on a lien portfolio is difficult. There are several variables in tax lien investing.

1) Tax liens are purchased in various ways - here are two popular methods;

a) Bid down interest rate - where the rate starts at the highest amount the state allows and the investors bid down with the lowest interest rate bid being the winner. Example - Arizona starts at 16% interest rate and you bid down in increments of a full 1%. You could end up bidding down the interest rate to 0%. You pay the full taxes owed and then earn the interest rate you bid.

b) Premium bidding - The interest rate is set at a specific amount (say 10%) and then you bid a premium over the amount. If the taxes owed are $1,200, you may have to bid $2,400 to win the lien. Then depending on the local statues, you earn interest on only the taxes owed $1,200 or maybe the premium amount also.

So figuring your rate depends on what you bid.

2) How interest is accrued on the lien. Most states will use simple interest accrual. If you buy a lien with an 18% interest rate, in a simple accrual you would be earning 1.5% per month. (1.5% x 12 = 18% per year) If an owner pays the taxes back 2 months after the lien auction, then you earn 3% on your lien in total - not the full 18%.

Some states have a tiered interest rate accrual. You earn 3% for the first 3 months, then 6% for the next 6 months, etc. until a maximum rate is achieved until the property owner pays.

3) There could be a "penalty rate". This is an amount that you receive in full no matter when the taxes are paid off by the owner. Sometimes there is a penalty rate in addition to an interest rate. Florida allows for a penalty rate of 5% due the investor at a minimum, and once the interest rate accrual is greater than 5%, then the investor is paid the higher accrued rate.

Example - win a Florida lien at 18%. It accrues at 1.5% per month. If the owner pays in the second month after the auction (1.5% x 2 = 3%) the investor is paid the 5% penalty rate as a minimum. If instead the property owner waits until month 9 (1.5% x 9 = 13.5%) the investor is paid 13.5% since it has accrued above the 5% penalty rate minimum.

Some states don't accrue interest rates at all and only pay a flat Penalty rate. No matter when the property owner pays, the investor earns the full penalty rate.

Knowing just these few variables, you can see it's difficult to gauge what type of return your tax lien portfolio will get. Most investors and tax lien funds rely on past history of liens to estimate how long (duration) on average their current portfolio of liens will take to redeem. They can then estimate the return based on the months and the average rate.

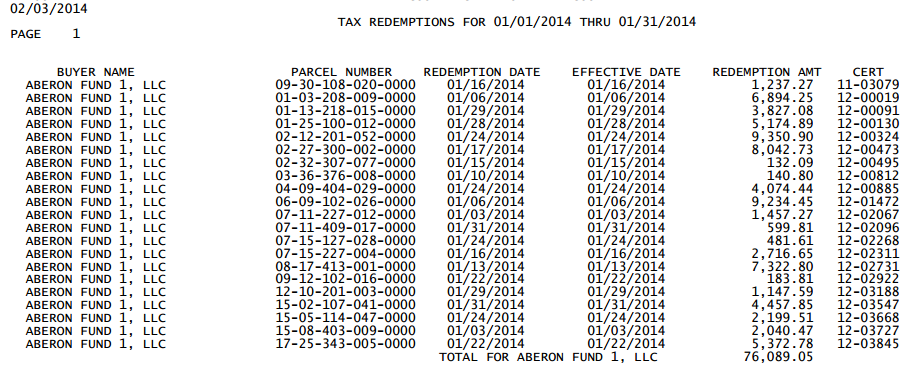

I just discovered for one particular county in Illinois that they publish a monthly listing of which liens paid off that month with amounts, parcel numbers, etc. The most fascinating part, to an investor like myself, is that it groups the paid off liens by the name of the winning bidder.

Why is this fascinating? This tells me what my competition is doing. I can convert this data into a database and learn what types of properties the competition has purchased, and more importantly when the liens paid off. If I wanted, I could learn exactly what the main competition has earned in this specific county.

The other fascinating data this list provides is the historical record of liens and when they are paid off by the owners. Of all the counties I invest in, this is the first time I have access to monthly redemption data. This is important to me for bidding strategies.

"Ok Jerry", you ask, "how can redemption data help you in a bidding strategy?"

Glad you asked. Now I'll tie this in with my explanation of interest rates above.

I can now keep a database of the parcel numbers and when the lien was paid off. There are always property owners that delay paying their property taxes every single year. I have seen tax liens on the same parcel in the auctions each year - yet the liens are always for the most current year - meaning the owner consistently pays their taxes late each year. By building this database of redemptions for this county (in which I have yet to buy liens - but will in the future) I will be able to quickly sort the parcels that are in the auction each year and pay off each year.

The magic is that I will be able to also see how many months later the owner waits to pay the late taxes. After a few years I should have a list of parcels that I can identify where I can earn consistent rates of return and have a pretty good idea of when they will pay off. In effect, very high paying short term CD's.

There is no guarantee that the owner will pay the same month each year, but many people are creatures of habit. There will be some parcels that will have this pattern appear as I collect the data year after year.

An investor can use this redemption data to help ladder a portfolio of tax liens that may have a consistent return.

Comments (2)

Thanks Jerry. Very informative.

Tim Holmes, about 9 years ago

Wow Jerry, More great analysis of the bidding in your markets! As tax sale gets more known it gets more competitive. This kind information and unique strategies is what can help build extra returns.

Ned Carey, almost 10 years ago