Why ALL landlords MUST use Rent to Own / Lease Options

First of all, for those who aren't familiar with this concept. Rent-to-own, or more formerly called a lease option. This means the tenant is also the buyer, what I like to call a tenant-buyer. They are going to rent the property just like a regular renter but they have a vested interest and plan to purchase the property at, or before the option period is complete. This typically ranges anywhere from 2-5 years. By this time, the buyer has improved their credit, earned a buyer's credit (typically 25%) and equity in the home. The bank is much more willing to give them a loan, at this point.

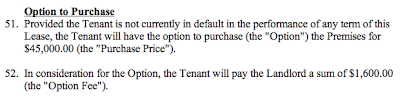

For most sellers, it sounds like a scary proposition but it is actually a very common practice. In fact it is included in most lease agreements, it's right beneath the terms of the contract:

The screenshot is from a form created with:

"Wait a minute" you say, "it sounds like the tenant-buyer has all the fun!" *buzzer sound* Wrong!

Here are the benefits to the seller:

- Low maintenance-

- It's the tenant's responsibility up to $300/mo.

- That's just an example, many people opt for more, or less, it's up to you!

- Less incidents-

- The tenant treats your home like their home so less damage is done to the property, overall.

- They settle in and take pride of ownership.

- More rent money-

- You are acting like the bank so you set the terms and add interest as you see fit.

- They are willing to pay more than market rent because you are doing them a favor.

- More upfront money-

- Instead of a refundable deposit, you get an option payment!

- This is a non-refundable amount (more than twice the rent) just for considering a RTO.

- More backend money-

- Again, you have given the buyer an opportunity they would not have had without you, you can charge what the property will be worth, most people figure 5% annual growth.

- All you are giving them is 25% as a buyer's credit towards the end purchase.

And the list goes on and on...

However, I see there are still skeptics out there saying, "I could just sell it for all that trouble."

But, before you settle for that option consider this:

Traditional sale-

A house is on the market for $100,000. Let's say it could even sell for that minus 6% for agent fees, 3% for tax and title and another 1% for closing costs. You are at $90K for your $100K home. That's not even figuring in marketing and the time it takes to sell it.

Landlord route-

You can rent it for about $750/mo (market rent) depending on where you live. Assuming a 5% annual raise in rent, you'd be getting about $28K over 3 years. You have to fix every little maintenance problem that comes up. Conservatively, you can assume about $5K over 3 years and that's assuming nothing goes haywire. Now, you netted about $23K minus your mortgage insurance and taxes. You are somewhere around $20K for 3 years and had to deal with a tenant. Heaven forbid, the housing market has taken another dive and your property is upside down, again...

Rent-to-Own-

You can rent it with an option to buy and your tenant will pay a premium for the opportunity. They will treat it like their own causing you less aggravation and damage. Don't forget the maintenance is covered up to $300/mo!! No more maintenance! That's worth at least $5K over 3 years, probably more. Also, you can get $950/mo instead of the market rent of $750. Then, after 3 years of collecting a lot of rent, they cash you out at FULL price! 15% more than it was worth 3 years ago. It's recession proof!! Let's add it up: $31200 rent less mortgage insurance and taxes + $1900 option payment + $5000 no-maintenance + $107800 sale less buyer's credit = $145900!!

As you may know, I went to school for a long time but I am not great at math. But rent-to-own adds up to me!! I will choose RTO all day long!

Are you a seller?

I have pre-qualified buyers lined up to rent-to-own your home!

Ready to make some money?

Thanks for reading!

As always, sharing is caring

Jen "Doc" Chandler

415-SELLIT5

Comments