Updated 17 days ago on .

Most recent reply

presented by

- Tax Accountant / Enrolled Agent

- Houston, TX

- 6,414

- Votes |

- 5,368

- Posts

EXPLAINED: The big fat lies about S-corps

- Tax Accountant / Enrolled Agent

- Houston, TX

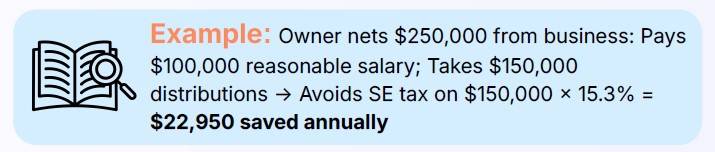

Here is a slide from a recent presentation. And not just some random presentation. It was presented by a self-designated high-end tax strategies firm. And they were "teaching" CPAs and asking us to send them referrals for creating S-corps.

Now, look at the slide again: $23k in tax savings! It would be stupid to forgo it. And you are not stupid.

Neither are such "high-end tax strategies" firms. I'm sure they make a nice income from rubber-stamping S-corps. Not stupid for sure. Not competent and not honest, either.

But who cares if we are promised huge tax savings - and we have no way to verify whether the savings are actually delivered? High-five, everybody is happy. Except us, knowledgeable tax professionals who call out this crap.

1. Avoid S-corps for rental properties!

Before we dive into numbers, let's save valuable time to those of you who don't need to bother with S-corps at all: owners of rental properties. All of them - regular rental houses, STRs (short-term rentals), apartment buildings, office buildings, storage facilities and so on.

*** Never put rental properties in S-corporations! *** There're zero tax benefits, only tax problems.

2. When an S-corp might save you money?

When you work for your business providing services aka labor, AND the business is profitable. And this explains, by the way, why it is pointless for rental properties: no services provided, and we typically show losses rather than income.

With a profitable business, you will have TWO, not one, taxes to pay. Well, possibly more than two, such as state income tax, unemployment tax and other taxes, but we're simplifying.

The first one is income tax. The second one is a combo Social Security plus Medicare tax. In the W2 salary world, it is known as FICA. When you work for yourself, it is known as self-employment (SE) tax. Same tax, just different names.

How much are they? Income tax depends on a whole lot of factors, and there is no simple answer. Anything from 0% to 35% and even higher is possible. SE tax is typically presented as 15%, or 15.3% to be exact. This is not a reliable number, as we will discuss later, but let's write down 15% for now.

Here is a fundamental thing to understand:

*** S-corp does absolutely nothing to mitigate income tax. It is used to mitigate SE tax. ***

3. How does an S-corp save you money?

So, let's say you're a house builder and, using the example from the misleading slide above, you generate a $250k profit for the year, after all expenses. You might owe maybe 20% ($50k) in income tax and 15% ($37k) in SE tax. Ouch. Getting rid of the $37k SE tax would be great.

Except we can't erase it, we can only partially reduce it. And an S-corp can't reduce the bigger one, the $50k income tax, not at all. Clear?

We just distilled the goal of an S-corp as a tax strategy: we're going after minimizing the SE tax. How? By paying yourself a W2 salary.

Without an S-corp, you owe SE tax on the entire $250k. If you set up an S-corp and pay yourself a $100k W2 salary, you owe SE tax on the $100k salary but not on the remaining $150k "owner's distribution."

If we indeed paid a 15% SE tax on everything, the example on the slide would have been accurate: avoiding a 15.3% tax on $150k means $23k in savings. If only...

4. What are the real savings, then?

Let's run this $250k example through real rather than hypothetical tax calculations. To make it as simple as possible, we're assuming that you are single and have no other jobs, businesses or investments. And we're using 2024 tax calculations today. (Every year the numbers change slightly.)

Ready? Let's go. We go with numbers only, not analyzing why they are what they are.

Scenario A: no S-corp; just a sole proprietorship or a single-member LLC; everything goes through Schedule C.

- Income tax: $42k

- SE tax: $28k

- Total: $70k

Scenario B: S-corp, $100k salary.

- Income tax: $42k

- FICA instead of SE tax: $15k

- Total: $57k

Did we save money? Yes! How much? $13k. It's not a bad result, no argument about it. But, geez, this is barely more than half of the $23k promised on the slide! Where is the rest of it?

5. Who stole our promised savings?

The structure of SE tax aka FICA. No, it's not a simple 15.3% shave. It consists of two components: 12.4% Social Security tax and 2.9% Medicare tax.

At around $175k (the actual number slowly rises every year), the 12% Social Security tax stops. The 3% Medicare tax goes all the way to your full $250k profit and will stay with you no matter how high your income grows. In fact, it will even increase at a certain higher income level.

Because the Social Security tax maxes out at the $175k level, an S-corp tax saving power drops significantly once you exceed this level. And we no longer save as much as we were promised by unethical salesmen masquerading as tax strategists. No bueno.

6. And it gets worse when you have another job.

Let's change our example. In addition to your builder's business, you also have a regular W2 job elsewhere. Suppose it pays you another $100k, expecting that you are a dedicated employee and not suspecting that in reality you spend all your time on your builder business, having ChatGPT write your employee status reports for you. (No, I did not suggest cheating on your employer, ChatGPT did.)

To recap: $100k salary from the regular job plus $100k salary from your own S-corp plus another $150k non-salary owner's distribution. Almost enough to buy gas and groceries in 2025 but probably not rent.

Before S-corp:

- Income tax: $85k

- FICA / SE tax: $16k

- Total: $101k

With an S-corp:

- Income tax: $75k

- FICA / SE tax: $13k

- Total: $88k

We still have $13k of savings, but with a completely different breakdown which makes no sense whatsoever: suddenly a reduction in income tax (which I said would not happen) while virtually no SE tax savings (which should have happened).

7. Make sense of this nonsense!

No, I'm not going to dissect the bizarre interplay of many different tax rules here. Taxes are nothing but intuitive. And there is a huge difference between someone who sells you grossly inflated promises with slick presentations and someone who prepares taxes for a living.

Let me assure you that my results are correct, and the fact that we again see the same $13k amount of tax savings is a pure coincidence.

To prove that this was a coincidence, here're some more numbers:

- if your main job pays you $200k, the S-corp savings would drop from $13k to only $10k

- if you have no job outside of your S-corp but are married - S-corp would save you only $8k

- and, ready for a shock? If you have another $100k job while being married, an S-corp for your builder business will cost you $2k MORE in taxes. You heard it right: more taxes with an S-corp than without! Damn.

8. I'm not making $250k yet, I'm only making $100k!

Well, if you can justify a $50k "reasonable salary" against this $100k income, you can avoid the SE tax on the other $50k. And saving 15% on $50k should be $7,500. I'd gladly take $7.5k for a simple formality of switching to an S-corp, wouldn't you?

Except, and I'm truly sorry to burst your bubble, the real savings in this scenario are less than $4,500 - half of what you expected. Why?!?

Because taxes are ridiculously complicated. (Hint for tax geeks: QBI).

Also, we're not addressing what "reasonable compensation" means. If you're considering an S-corp, this is a critically important issue, but it's for a different article.

9. But wait! There is more! Or, in this case, less.

Well, $4,500 from the most recent example is also money. True, but switching to an S-corp is not free. You need to form an LLC, which in Texas costs a modest one-time fee of $300. In California, starting an LLC is cheaper but keeping it will cost you $800 every single year. And this is only when you DIY your LLC. Hiring a lawyer is a lot more.

Next, you need a payroll service. $500-$1,000 per year from online service providers. Then you will need to be filing two tax returns, not one: your S-corp requires a separate tax return, and it's not a simple one. CPA charges for preparing an S-corp tax return start from $500 and can exceed $3,000. Also, professional double-entry bookkeeping is not absolutely required but is highly recommended. It's not easy to learn and not cheap to outsource.

In other words, there is nothing left from your tax savings in the end.

This is not to mention the hassles of running your S-corp properly. If you bought some tools for your business on your personal credit card, usually it's still deductible. Not so if you run an S-corp, then it becomes a problem.

10. Are you saying that S-corps are totally useless?

No. An unmarried business owner generating $500k in net business income will save $35k using an S-corp with a $150k reasonable salary. Then an S-corp becomes almost a no-brainer. Almost, because at this level of income, a C-corp could be a more attractive alternative.

Also, S-corps have purposes outside of reducing SE tax. But I have to stop at some point. That point is now.

If you remember anything from this article, it should be this:

An S-corp may save you some money, but it will be a lot less than you expect. Sometimes it can even increase your taxes. Don't rush into an S-corp. Consult a real expert who does a thorough comparison, not some useless quick estimate on a napkin.

Most Popular Reply

- Accountant

- Chicago, IL

- 752

- Votes |

- 1,575

- Posts

- Accountant

- Chicago, IL

Absolutely spot on Michael. This is one of the best summaries I've read on s corps that lays things out well for the reader.

i can't tell you how many times ive sadly seen rental properties in s corps.

Great breakdown and always appreciate reading your insights!

- Aaron Zimmerman

- [email protected]