Brandon Turner's Failure at Open Door

It's been an ugly ride at Open Door Capital for the former face of BiggerPockets and the OG host of the podcast.

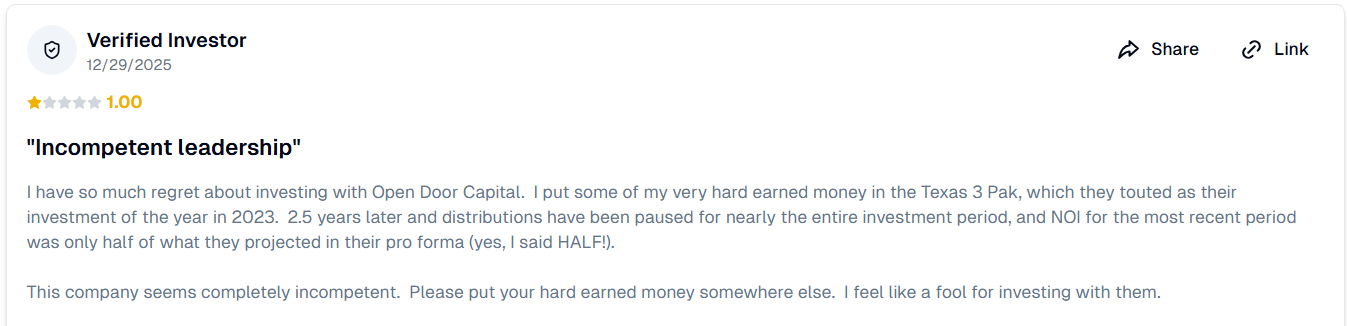

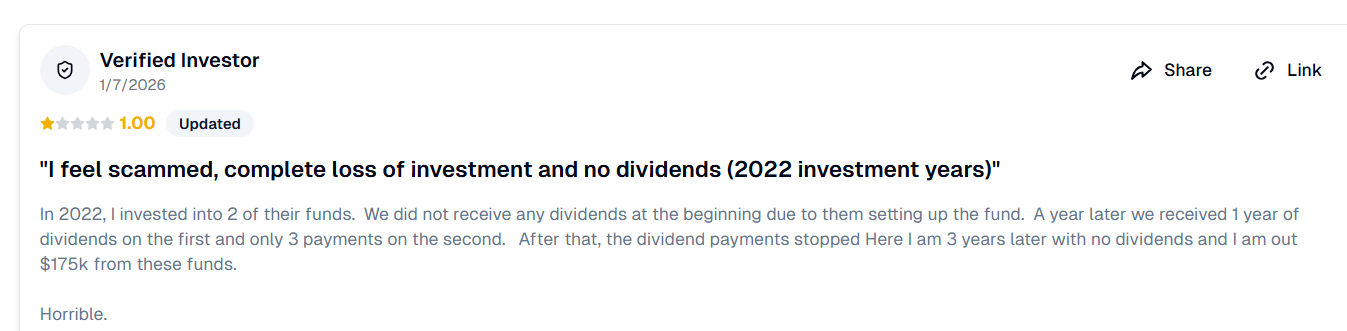

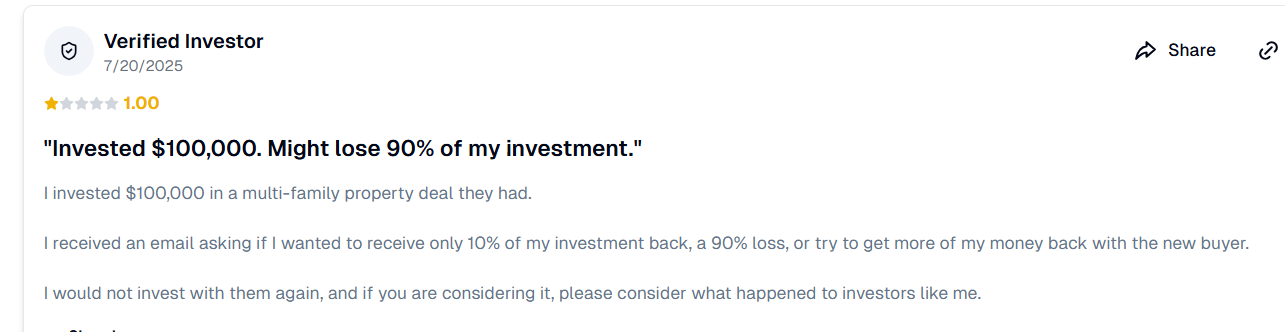

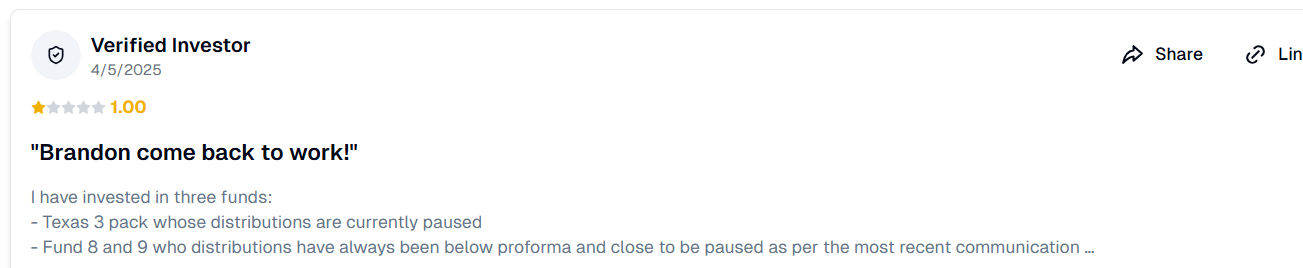

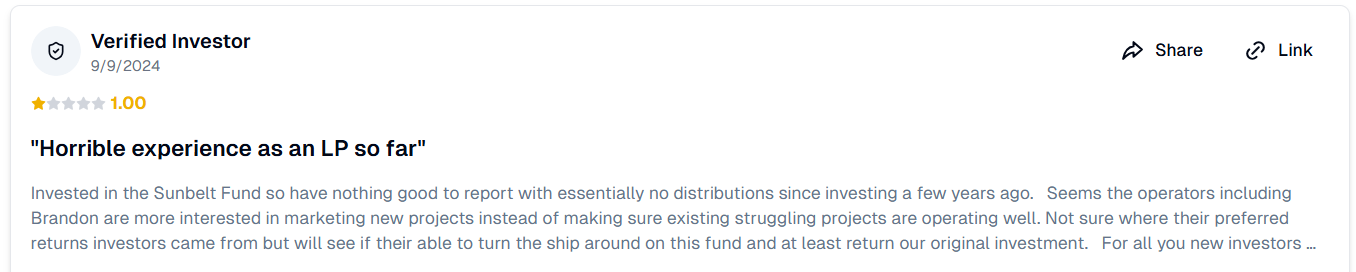

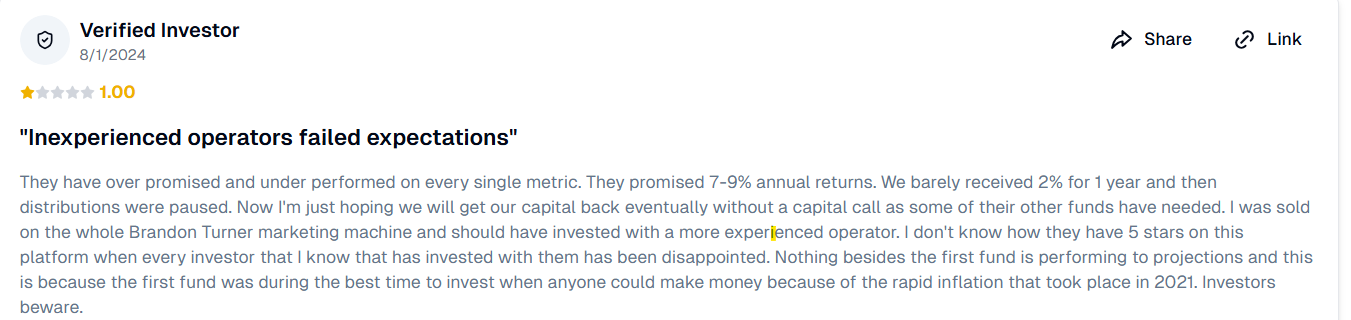

Here are some of the recent reviews from verified investors on Invest Clearly:

Most Popular Reply

- Attorney

- Philadelphia

Never invested with ODC and my knowledge of the syndication firm is limited to what I've read on Bigger Pockets but what’s the point of this post besides being deliberately provocative? ODC’s underperformance has been discussed extensively on BiggerPockets. Yet these threads predictably devolve into the same pattern. LPs who performed poor or no diligence at all and often cannot clearly articulate the business plan they invested in show up to point fingers, threaten SEC complaints, and talk lawsuits without being able to identify wrongdoing or fraud beyond the obvious. A weak investment thesis & underqualified management paired with aggressive underwriting.... What could possibly go wrong???

Rather than rehashing the same forum content yet again, let's try something different and reframe the discussion in a way that actually adds value for other BiggerPockets readers. This should be treated as a case study in how not to perform diligence before investing in a syndication & what red flags to look for and how to properly analyze syndication opportunities before making an investment. This has the opportunity to add real value.

Otherwise, the next voices to chime in will almost certainly be current LPs, and judging by the reviews you shared, it is difficult to see how additional commentary from investors who did not understand the strategy at entry will materially advance the discussion or add meaningful value. Unless you believe the people whose reviews you posted will advance the discussion in a meaningful way.....

1. Multiple reviewers explicitly stated they invested based on Brandon Turner’s name recognition from BiggerPockets. From what I can gather, his background was primarily single family investing alongside his responsibilities at BiggerPockets.

I would equate that to remembering your elementary school math teacher was good at teaching multiplication tables and then, years later, deciding to hire him/her as your financial advisor.

2. Several comments also criticize ODC for poor risk management due to the use of high leverage and adjustable rate debt. But this was not hidden or discovered after the fact. The capital stack and loan terms appear to have been known before anyone invested, and that risk was explicitly accepted at entry.

What is telling is the reversal that follows. When performance lags, the investor who knowingly bought into a highly levered, floating rate strategy suddenly disclaims all accountability and reframes the outcome as a GP failure to manage risk. That is not a risk management critique. It is hindsight revisionism.

3. Another reviewer claimed they were promised a 7% to 9% return. Which is it, 7% or 9%? And more importantly, I highly doubt there was a promised return at all.....maybe preferred? Projected? Targeted? . Beyond that, what sensible person invests equity in a real estate syndication believing they are getting a 7%-9S% guaranteed return?

Get my point that hearing from these investors adds little value to the forums? That's what your post intends to attract.