Madison Wisconsin 2020 Q1 Report

Hi everyone! I't is that time again for another quarterly report. Hard to believe we're only at Q1 considering how long the last month has felt. It is going to be interesting to watch how the country handles COVID-19 and the ways it will impact our industry. For now though, we look at the numbers and see if we can gain any insight.

I'm always open to feedback so please leave any questions and/or comments regarding the report, especially if there is something you feel is missing or could be expanded.

Data Source and Methodology

All data comes from the Statistical Reporting section of our local MLS. These numbers do not include any FSBO or other "off-market" sales which do not appear on the MLS.

The data includes all Single Family, Condos, and Multi-Family from 2000 to the present. In the past I identified 7 indicators that I believe give the best picture of our market. These indicators are:

- Total Units Listed

- Total Units Sold

- Average Sale Price

- Average Days on Market

- Percent Sold

- Percent Expired

- Gap (Difference between Percent Sold and Percent Expired)

For this report I will also be adding an eighth that I will touch on at the end. It is my attempt to quantify Demand.

Using these indicators, I compare the median value (using data going back to 2000) against what the most recent Q1 shows. I find the median to be a better metric than the average, since some of these indicators swing wildly depending on the time of the market.

Summary

We started the year hot, but due to the impacts of the virus, we cooled at the very end of the quarter. I'm cautiously optimistic due to Demand Levels remaining within expected ranges.

Q1 Looks Strong on Paper

Q1 2020 follows the trend set by Q4 2019 and strongly outperforms the previous year. Listings, Number Sold, Percent Sold, and AVG Sale Price all rose significantly. Meanwhile, DOM and Pct Expired hit record lows, helping to set a record high Gap this year as well.

What kind of impact should we expect to see from COVID-19?

What we've seen over the last 2-3 weeks is that the total listed and total sold are both down significantly. The other indicators haven't shown much change, I think mostly due to these being lagging indicators. Still, it appears that the drop in both listings and sold properties remains proportional to this point. Meaning, there are still buyers in this market. If we do not see an extended period of lockdown, and are able to get the majority of people affected by this crisis back to "normality" fairly quickly, then we should see very typical numbers in the rest of the indicators.

This is the real key indicator I am going to be watching going forward. If the Demand Level begins to change, this could have a significant impact on price.

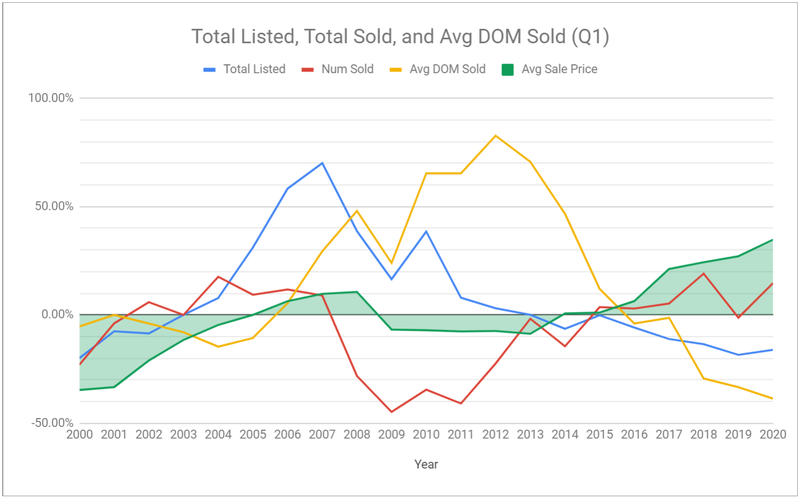

Let's take a quick look at the two charts I used last time to get a feel for demand level.

Last time, I identified Total Listings as the first one to watch. Just like with Q4 2019, we see Total Listed rise for the first time in 5 years. However, that rise is not significant, and will likely disappear throughout the year as more and more sellers choose not to sell in this environment.

Despite the small increase, we see Total Sold spike back up near to the highs set in 2018. On top of that, AVG DOM dropped to its lowest level ever.

To me, the above graph suggest that Demand Level appears to still highly favor sellers.

This graph continues the narrative that Demand Level highly favors sellers. Percent Sold and Percent Expired are still traveling in opposite directions, causing the Gap between the two to hit record high levels.

Still, most of these metrics are lagging. Let's take a look at a leading metric to see where Demand Level is headed.

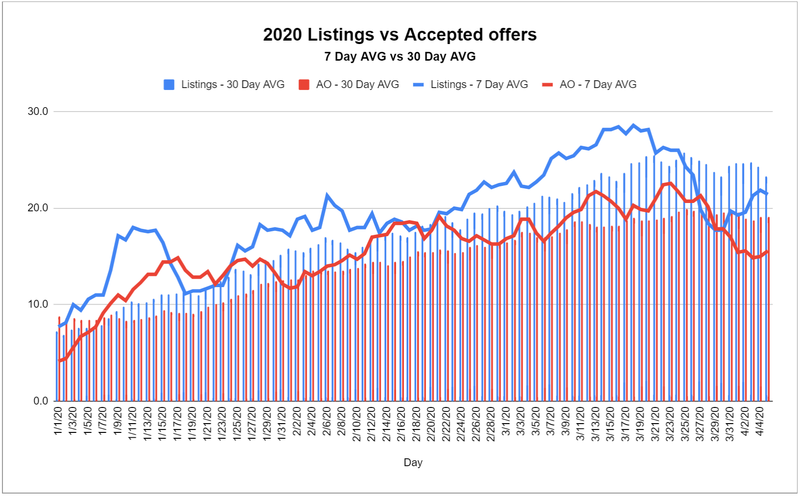

Current Demand Level

Going back to the beginning of 2018, this graph shows us the Total Listings vs Accepted Offers, and then the Gap between the two. We are at an interesting point for this graph. If you look at the numbers for mid-late March of 2018 & 2019, we see a similar pattern to what is developing in 2020. There is a small plateau, followed by a final surge of listings and offers which typically peaks in late May. The question we have is, will we see the pattern continue or have we already peaked in listings and offers?

My inclination is that we have not peaked. However, I don't think we hit anywhere near the numbers we've seen from the past 2 years. To put it into pandemic terms... The curve will be flattened.

Why do I think this? Let's look at Accepted Offers. In both 2018 and 2019, we see AVG Accepted Offers for the period from late March to early July remain above 20.0 the vast majority of the time. Contrast that will 2020, where the AVG Accepted Offers have yet to even hit 20.0, let alone try to stay above.

In addition, the 7 Day AVG for both listings and Accepted Offers shows a very different picture than the 30 Day AVG.

Both 7 Day AVG's (the solid lines) show steep declines starting around 3/25, and continuing through to the end of the month. The beginning of April shows some recovery for both, but mostly in Listings. If Listings continues to rise while AO's remain flat (or fall) then I expect to Price become affected.

This is why the Q1 numbers are, to me, only "good on paper". It wasn't until the last 7-10 days of the quarter that we start to see an impact of the shutdown...

Final Thoughts - What To Look For Moving Forward

For now, Demand Levels remain within an expected range. We may see fewer Listings and AO's then a normal year, but unless they diverge significantly from here then Price should remain stable.

I'm cautiously optimistic about the Real Estate landscape, but April with go a long way to either bolstering or eroding that optimism.

Please Leave Feedback

Always happy to hear where I can improve things, or even just to hear which areas in particular you find most helpful. As always, if you are in another market, such as Milwaukee, Sheboygan, Janesville, etc. and would find similar analysis for your market helpful, feel free to reach out with a specific inquiry.

Most Popular Reply

Thanks for an in-depth explanation of the markets as of Q1 2020 in Madison! It's nice to have someone break down the data and give their opinions. So far it appears that the real estate market is holding up and is being driven by demand. I understand it may be difficult to predict numbers and thus drive demand down. Do you believe prices will remain stable over the next couple years here in Madison? If not, when do you see them falling?