May Jobs Crush Forecasts as Home Price Appreciation Outlook Improves

Alright, let's walk through the key data from last week because there was a lot of it and most of it came in better than expected.

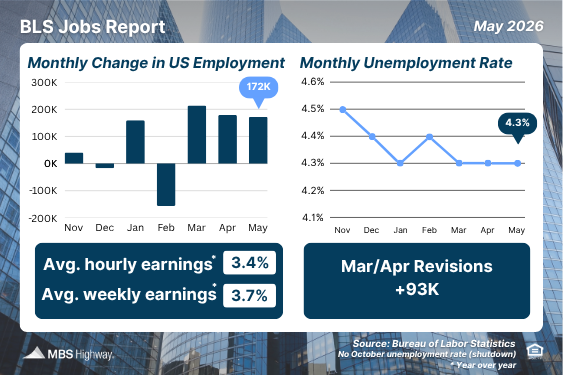

BLS Jobs Report: A Big Beat

The May nonfarm payroll number came in at 172,000, roughly double the consensus estimate of around 85,000. March and April were both revised higher by a combined 93,000 jobs. Unemployment held at 4.3%, and the three month average of job growth is now 188,000, an acceleration from where we had been sitting.

The soft spots worth tracking: full time employment fell 79,000 while part time increased 266,000. Continuing claims are elevated at 1.78 million, which tells me a lot of people are finding jobs available but taking longer to land them. Challenger data showed about 97,000 job cuts in May, with AI driven restructuring cited as the number one cause for the third month running.

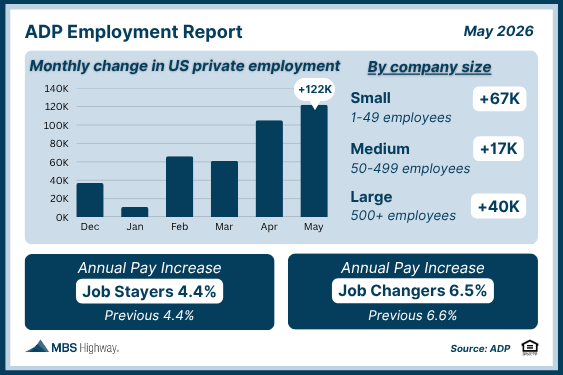

Supporting Data from ADP and Others

ADP private payrolls came in at 122,000 in May, above forecast. Broad based gains across eight of ten sectors, all company sizes participating. Revelio Labs tracked 123,700 job gains in May, nearly double April and the strongest single month since last July. Job openings moved from 6.9 million in March to 7.6 million in April.

Cotality Home Price Update

Month over month: up 0.4% in April. Year over year: up 0.3%. Cotality revised their 12 month forecast to 5.3%, up from their previous call of 5.1%.

On a $500,000 asset, that is roughly $26,500 in equity growth in a year before you factor in any cash flow, debt paydown, or value add. For investors evaluating acquisition timing, the appreciation component of total return is improving even as cap rate compression has made cash flow deals harder to find.

Key Takeaway for Investors:

A strengthening labor market supports rental demand and tenant stability, which matters a lot for your cash flow projections. Layer in a revised appreciation forecast of 5.3% and the total return picture on buy and hold real estate looks meaningfully better than it did six months ago. If you have been sitting on the sidelines waiting for clearer signals before your next acquisition, this week's data is worth paying attention to.

This Week's Calendar

Tuesday: Existing Home Sales. Wednesday: CPI. Thursday: PPI and weekly jobless claims. The CPI print is the one to watch most closely for any near term signal on where rates are heading and how that ripples into MBS pricing.

- Derek Brickley

- [email protected]

- 734-645-7722