Real Estate News Roundup: Demand Outpaces New Construction; Market to Remain Strong Through 2021; Affordability Improving Nationally

A roundup of news and information from around the web about real estate, personal finance, and the economy.

New Construction Home Listings Drop 4% in August, Reversing Course from July's Rebound

The new-homes market is recovering—with sales on the rise—but hurdles including a lumber shortage are still hampering builders

New listings of newly-built homes dropped 4.1% year over year to a seasonally-adjusted rate of 74,000 in August, reversing course after a 3.8% gain in July, according to a new report from Redfin. Meanwhile, new listings of existing homes grew 5.2%. "There's plenty of demand for new homes, but builders are facing a unique and costly set of hurdles as they attempt to satisfy that demand," said Redfin chief economist Daryl Fairweather. "Listings of new homes aren't bouncing back as quickly as listings of existing homes because, unlike individual homeowners, construction companies have to deal with lumber and labor shortages during the pandemic. They're also competing for labor and materials with folks who are renovating their houses during quarantine. The lack of new listings is keeping builders from reaching their full potential in terms of home-sales growth." Sales of newly-built homes were up 8.3% year over year to 73,000, a deceleration from July's 13.5% increase, while sales of existing homes rose 10.5%—outpacing new-home sales growth for the first time since 2015. The supply of newly-built homes for sale sank 33.6% year over year in August to 185,000, while the number of existing homes on the market plunged 38.3%—the largest declines since at least 2013. Access the full report here.

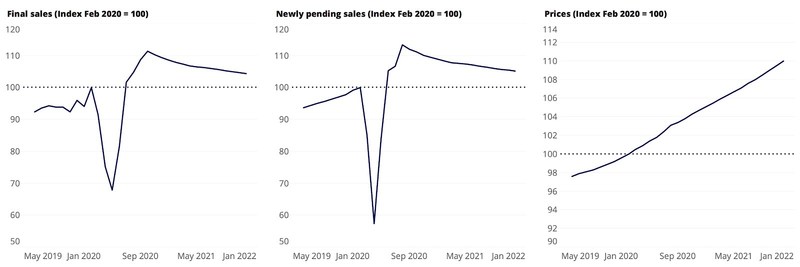

New Forecast Sees Sales Peak This Fall, Stay Above Pre-Pandemic Levels Through the Coming Year

After a remarkably hot summer, home sales are expected to peak this fall then taper off in 2021 while staying above pre-pandemic levels, according to a forecast by Zillow's team of economists in . Key market stats from the week ending Sept. 19 show depleted inventory levels plumbing new depths and prices skyrocketing over 2019 figures.

Forecast: Housing market outlook improves, with major unknowns tempering expectations

- Sales expected to stay high but taper down through 2021: Zillow's team of economists expect seasonally adjusted home sales to peak this fall then gradually decline through 2021. Sales volumes overall are forecasted to remain higher than pre-pandemic levels throughout this year and next.

- Home price outlook adjusted higher for coming year: Seasonally adjusted home prices are expected to increase 1.2% from August to November and rise 4.8% between August 2020 and August 2021. Zillow Research's previous forecast predicted a 3.8% increase in home prices over this time frame.

- Here's why: Zillow's predictions for seasonally adjusted home prices and pending sales are more optimistic than previous forecasts because sales and prices have stayed strong through the summer months amid increasingly short inventory and high demand. The pandemic also pushed the buying season further back in the year, adding to recent sales. Future sources of uncertainty including lapsed fiscal relief, the long-term fate of policies supporting the rental and mortgage market, and virus-specific factors, were incorporated into this outlook.

Click here to find out more. [caption id="attachment_130153" align="alignnone" width="800"]  Per Zillow[/caption]

Per Zillow[/caption]

Affordability Improving Nationally Despite Strong Nominal Price Appreciation, According to First American Real House Price Index

Recent history has shown that in times of economic distress, lower mortgage rates have offset the affordability drag from faster house price appreciation and lower household income, says Chief Economist Mark Fleming

First American Financial Corporation, a leading global provider of title insurance, settlement services, and risk solutions for real estate transactions, today released the July 2020 First American Real House Price Index (RHPI). The RHPI measures the price changes of single-family properties throughout the U.S. adjusted for the impact of income and interest rate changes on consumer house-buying power over time at national, state, and metropolitan area levels. Because the RHPI adjusts for house-buying power, it also serves as a measure of housing affordability. “This demonstrates the ‘downside stickiness’ of house prices during economic decline. In the pandemic-driven recession of 2020, we’ve seen house price appreciation grow faster than in any of the economic declines in our recent past.” “Affordability improved in July as two of the three key drivers of the Real House Price Index (RHPI), household income and mortgage rates, swung in favor of increased affordability, outpacing the rise in nominal house price appreciation. The average 30-year, fixed mortgage rate fell by 0.75 percentage points and household income increased 5.5 percent compared with July 2019,” said Mark Fleming, chief economist at First American. “Declining mortgage rates and rising household income levels both increase consumer house-buying power. So, even though nominal house price appreciation jumped 8.2 percent annually in July, it was not enough to offset the affordability boost from declining rates and rising household income. “While there remains debate regarding the actual end date of the 2020 recession, there is no argument that the economic pain inflicted by the coronavirus continues to linger. Yet, housing affordability nationally has improved, and the housing market remains resilient,” said Fleming. Learn more here.