The Vacancy Math Most CRE Investors Get Wrong (And Why It Kills Your IRR)

Most commercial RE investors I talk to model vacancy as a flat percentage — "I'll assume 5% vacancy" — and call it a day. That single number is hiding a ton of risk.

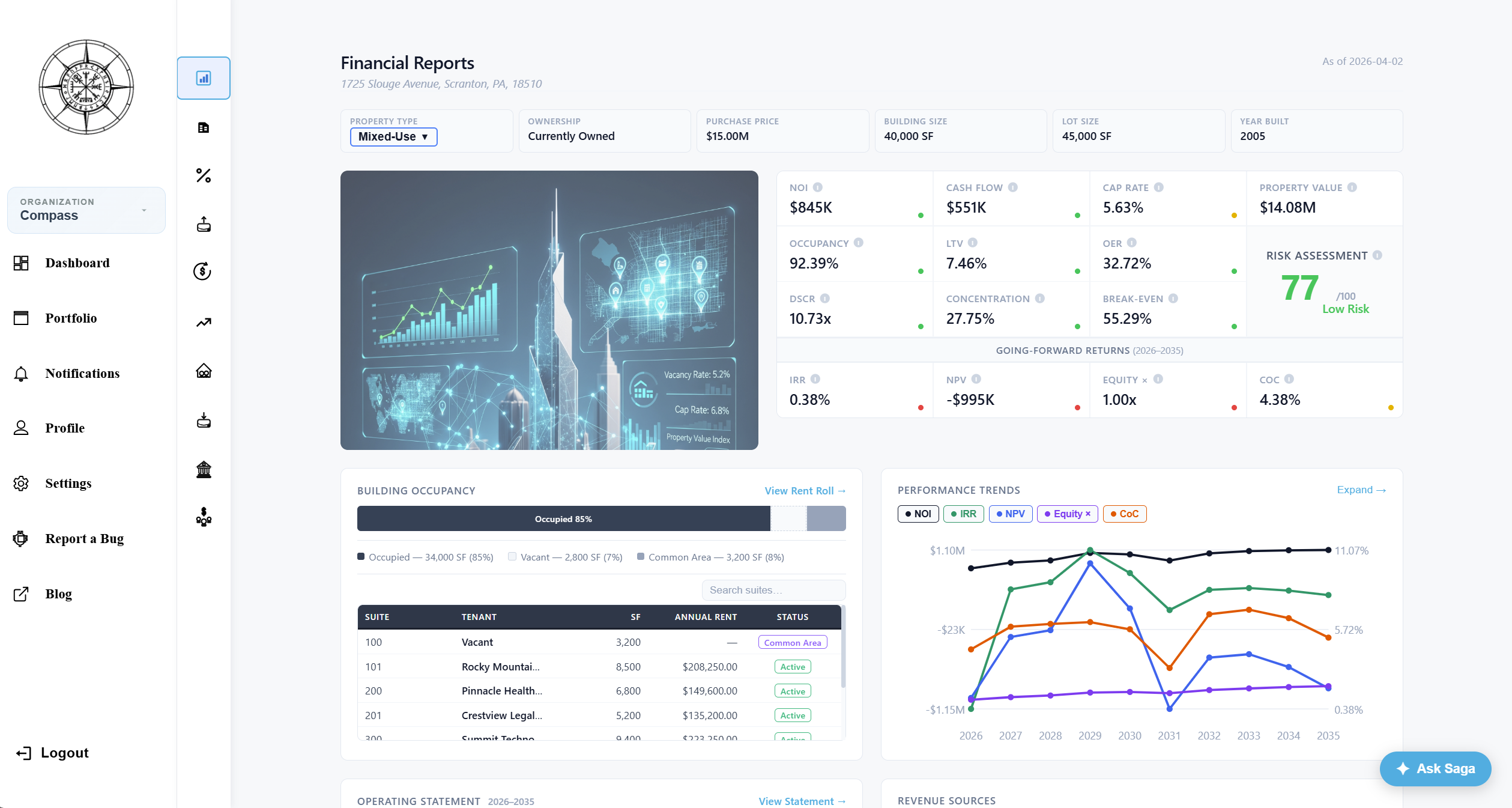

Here's what I mean. Say you own a 40,000 SF mixed-use office/warehouse building with 7 suites. Two leases expire in Year 3, six months apart. What actually happens?

The flat % approach says: 5% vacancy every year = $X lost revenue. Simple.

What actually happens:

- Tenant A's lease expires March 2028. 60% chance they renew (based on market and tenant quality). If they don't, you have 4-6 months of vacancy plus TI/LC costs to re-tenant.

- Tenant B's lease expires September 2028. Different suite size, different renewal probability, different market rate for that space.

- If BOTH don't renew in the same year, you could be looking at 30-40% physical vacancy for 2-3 quarters, not 5%.

- The new leases come in at market rates (which have been inflating), not the old contract rates.

- Meanwhile, your variable expenses (utilities, janitorial) partially scale with occupancy, but your fixed expenses (insurance, property tax) don't care if the building is empty.

That Year 3 "5% vacancy" could actually be a 15-20% hit to your NOI depending on timing, renewal probability, and re-leasing velocity.

What I've started doing instead:

I model each tenant's lease individually — their specific expiration, renewal probability, estimated downtime if they leave, and what the new market rate would be (inflated from today). Then I project that forward across the hold period.

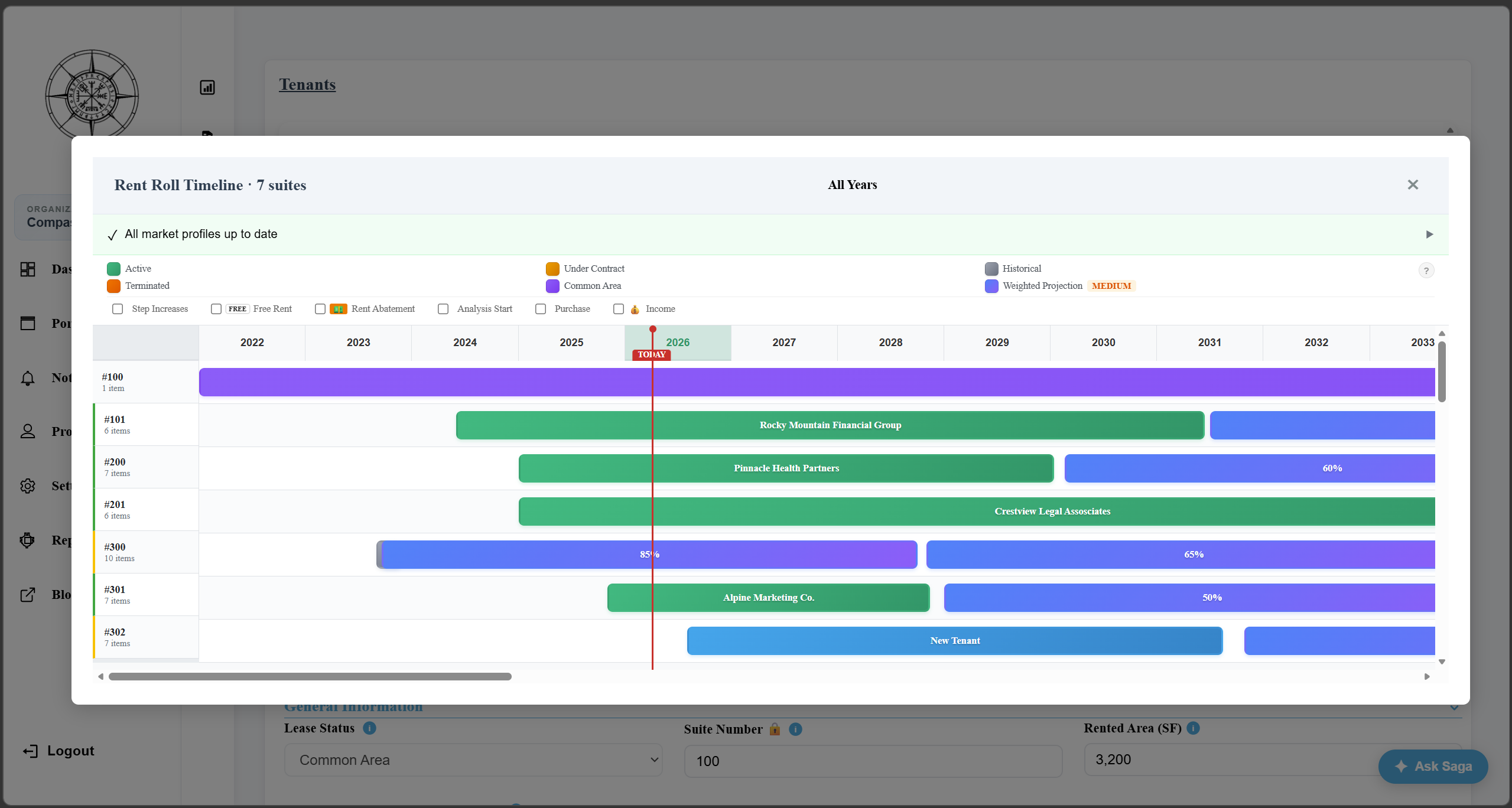

Here is what tenant modeling looks like.

Here is what tenant modeling looks like.

This gives you a year-by-year rent roll projection where you can actually SEE when your risk concentrations are. Two leases rolling in the same year? That's a red flag you can plan for. Staggered expirations? Much safer cash flow profile.

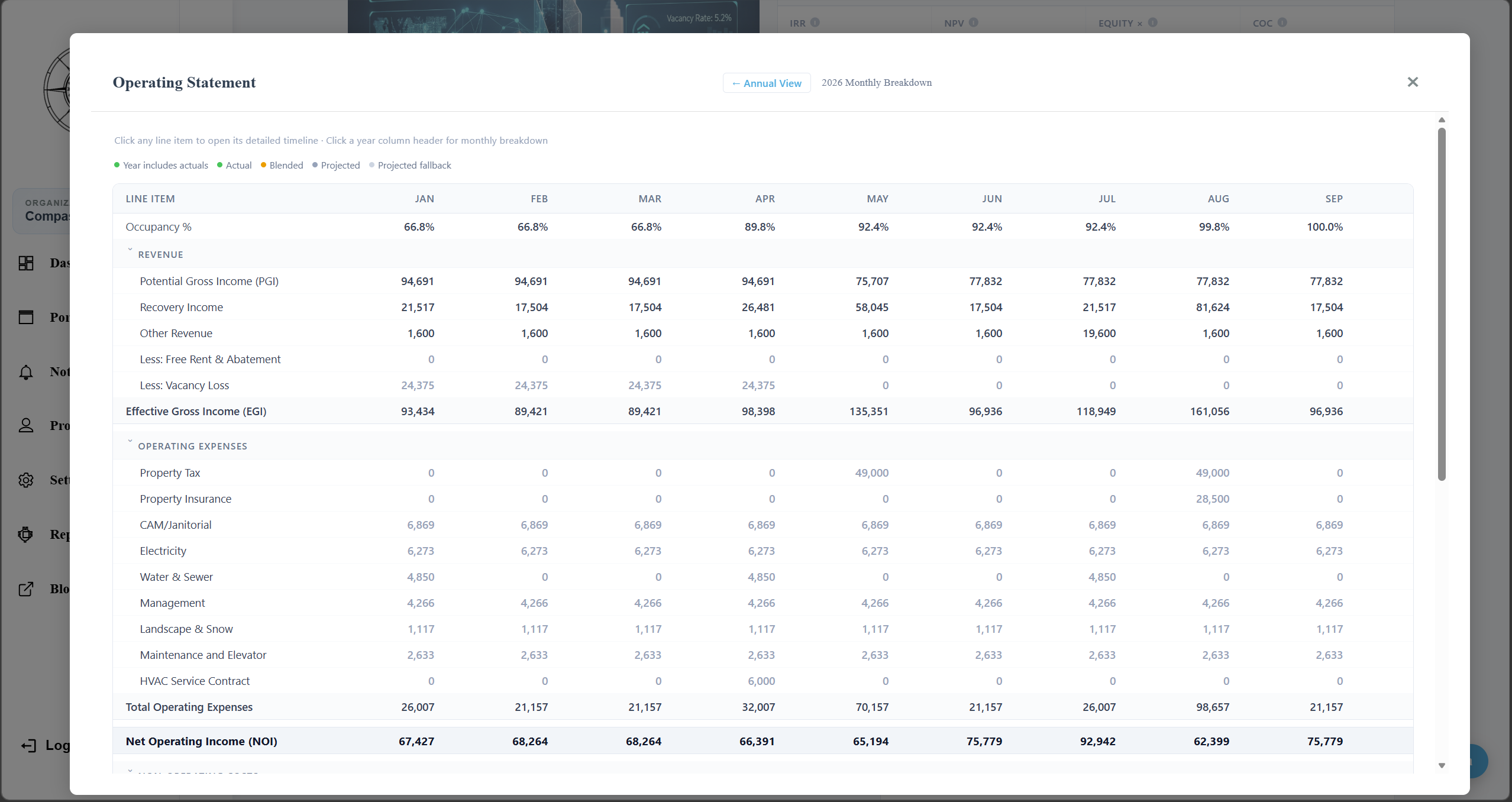

The same logic applies to your expense recoveries. If you have NNN leases, your recovery income drops when suites are vacant. If you have Base Year Stop leases, you're comparing against a base year that might be 5 years old. The interaction between tenant rollover and recovery income is where a lot of deals quietly underperform projections.

None of this is rocket science — it's just tedious to model in Excel because you need each tenant on their own timeline, interacting with market assumptions that inflate over time. I got frustrated enough with my own spreadsheets that I built a tool to handle it, but the core concept applies regardless of what you use:

Model tenants individually, not as a blended average.

Your IRR is only as good as your rent roll assumptions. A flat vacancy rate is just telling yourself a comfortable story.

Anyone else modeling tenant-level vacancy? Curious how others handle the renewal probability piece — do you use a flat assumption or vary it by tenant quality/lease term remaining?

Most Popular Reply

- Cincinnati, OH

- 3,760

- Votes |

- 4,069

- Posts

- Cincinnati, OH

This is why most commercial investors use specialized software packages, not just excel.

Excel is fine for a "quick and dirty" underwriting to see if a deal is worth diving deeper into, assuming the high level investment thesis is met. If I am not "too far" off on a deal, then I go into rDCF, or a lot of major players use Argus, to outline each unit.

To you point, especially compared to Multifamily, commercial deals are far more nuanced than applying blanket property level assumptions.

- Differing lease expirations (varying by years, not months)

- Recovery pools: NNN, gross, modified NNN, NNN + Mgmt & Admin, etc

- Unit size often equates to varying vacancy lengths and TI packages

- Options

- Likelihood to renew percentages

Given how tight many deals are these days, not being able to account for all the nuances that impact operations is a recipe for disaster.