Updated about 9 hours ago on . Most recent reply

Warning! RE will keep you poor and the passive income myth

This is a PSA for the majority of new members on here who just read a Rich Dad Poor Dad book or similar and looking for advice on how to build wealth by buying rental properties most likely in C class neighborhoods with the intention of BRRR in 2025 and who have a 9-5 job which is most likely the majority of new members.

During my time in the mid to late 2000s, we had the 1% rule which I followed. I purchased a 100k house in cash in Texas which rented for $1k/month and it tripled to 300k by the time I sold it at the peak in 2023 before the current price drops. I believe this aligns with the national average.

That is 200k in equity divided over 17 years and you get an average rate of appreciation of 10%/year not including the rental income which I will get into. But lets look at that 10% and look at the real rate after selling costs (I didn't want to 1031 exchange into another problem). After, taxes at the federal income rate (65k), recapture of depreciation (17k), agent fees (20k) and what nobody here or book will tell you, is renovation fees. After 17 years of renting a 1984 home, you'll spend $25-50k to renovate it enough to receive full market value and that is if you're lucky enough for your insurance to cover a new roof because a lot of buyers will want a concession for that if it's aging. Otherwise, the new home owner will have issues insuring it.

All said and done, the appreciation drops to 4.3% on average over 17 years (around 75k from 200k), which follows the national average rate of appreciation according to Case Shiller and other sources I believe. But we still have rental income since I did purchase it in cash. That should make up the difference, right?

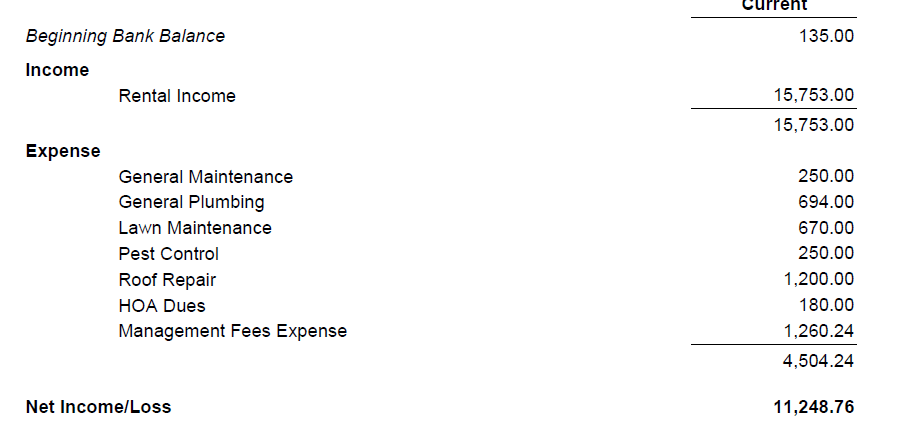

Here's one statement as an example and was a particularly good year with little expenses.

Subtract $4500 in property taxes and $2500 in insurance.

= $4,250 actual income divided by the purchase price of 100k

= 4% cash return on investment.

Take appreciation and cash on cash return and you get

Around 9% total return every year for 17 years or $9000/year I think which = 150,000 total cash return after sale.

Don't get confused with compounding like a stock. The S&P 500 has averaged over 10% I think over the same period.

From the S&P 500 history calculator.

Real Estate = $150k

S&P 500 = $540k

But what about leverage you ask? I would need 4 properties ($600k) to beat the S&P 500. No problem, I'll just put 25% down and buy 4 units.

But I would have a mortgage at 6% for the first 13 years until rates were low enough to refinance. 25% down would be break even so no cashflow. Now you have to reduce each unit by $75,000 (the $350/month for 17 years). So cut the 600k in half and you'll need 7 units to match the S&P 500. Again, after federal taxes, recapture fees, renovations, agent and misc selling fees and rental expenses.

The rental income is eaten up by capital expenses and the fees I displayed. Every increase in rent was eaten up by the state reassessing home values ever year plus growing maintenance on 50-year-old home.

Some arguments against myself is that I could have been more efficient than 50% (income to expense ratio) but 50% is average for an older home in this location as stated by books I have read and my own experience. I could have also renovated earlier and increased rents to market rate but the rental market rate didn't really pop until the last few years and my payback would be 5 years. Another argument is that I could have rolled over the $350/month in cashflow into the S&P 500 and gained an additional 250k over 17 years. This means that I could purchase two properties with 50% down and maybe matched the S&P 500. Remember no passive income with a mortgage at 25% down. I also could have 1031 exchanged but I don't want to exchange it for another low return, high risk burden.

Even with leverage which all the influencers will be quick to mention, just can't beat the S&P 500 without tons of risk and work. Who wants 2-7 units when you can simply put the same amount of money into the S&P 500 and walk away. You just purchased yourself a job.

||||||||||||||||||||||

Here's another myth keeping you poor. Passive Income!

If you're working 9-5. You don't need passive income. What is $100/month or $1000/month to you now when you don't need it?

I realized that passive income is only good when you retire. Nobody needs passive income when you're working. If you have a home mortgage, make sure it's paid off when you retire otherwise the extra income is better off in the market building wealth at a faster rate than your passive income and the capital used to generate it.

Also, it's not passive if you're putting time into it, spending days doing taxes finding all the websites you need to login to and pay all the misc rental taxes, prop taxes, HOAs etc. It's like a dozen. I probably spend a week every year just doing taxes. Then the stress of getting sued, answering emails, storms that blow your tree over and almost murder the tenants, it's not a lot of time but it's enough for me to put a value on my time vs no time nor risk in an index fund.

I purchased a condo for 150k in San Diego in 2012 returning $1000/month. Awesome right?

Again, lets go back to investing that 150k into the S&P 500. That's 150k in cashflow over 13 years and 100k in appreciation = 250k.

But again:

S&P 500 = $1,000,000 (some calculators show 700,000 probably adjusting for inflation)

Real Estate = $250,000

1000/month vs 1M? You could literally just pay yourself out with the million or if you like the psychological idea of passive income, then you can achieve the same result with a dividend fund and receive a check every month but with way less work and less risk. Real Estate just gives you a check that you don't need and its principal grows more slowly.

This is why I'm so bitter with real estate. Leveraged or not, I could have been retired by now had I simply put my money into the market instead of buying real estate. The same money invested 10-17 years ago would have net me well over 10 million dollars by now had I just put it all into the S&P 500, 401k matching with Roth and maybe a couple tech stocks, bonds or dividends for diversification. Of course I have all these things but my portfolio was heavily into RE maybe 90/10. Now I'm shifting into 20% real estate (for diversification and to live in) and 80% market.

In summary, Real Estate is a soul crushing scam that keeps you poor and makes others rich by selling books, videos, seminars and of course forums like this used for advertising and podcasts. It's a billion dollar industry that needs to convince new members that they can build wealth by buying homes that are made for families thus turning real estate into a stock like product which continues to make housing unaffordable for the common family.

Most Popular Reply

- Investor

- Poway, CA

Your math is very incorrect when it comes to the leverage as you used the unleveraged appreciation rate. If you purchased the $100k property at 80% LTV, if the property appreciated to $300k, your return from appreciation is 1000%/17 years. Not only would you not need 4 properties, but one property would far exceed the 10%/year S&P that you used which would result in $101k of growth ver 17 years (just over half of what you would have achieved via the property implying that 0.5 property would be virtually equivalent). Active asset managers likely would have refinanced the property multiple times over that 17 years and achieved far better return than the 1000% return over the 17 years.

The flaw in the leverage calculation is just the biggest flaw.

You chose not to value add until selling. You chose not to use leverage. You chose to sell and pay the gains versus never paying the tax on the gains. You did not discuss the tax advantages of RE with OBBB now allowing 100% bonus appreciation.

It also sounds like your initial underwriting may not have been accurate as to actual expenses. It is important to have accurate underwriting to have an accurate estimate of the cash flow. The cash flow should not be a surprise over a 17 year period.

I agree without leverage, it may be challenging to exceed the S&P. The unleveraged property investment would get whooped by Magnificent 7 or Fab 5.

You purchased a $150k property in San Diego in 2012 and it is only worth $250k? I find this shocking. In 2012, I purchased a property in Escondido for $302k that is worth ~$1.1m today In 2013 I purchase a property for $490k that is worth ~1.3m and another for $390k that is worth ~1.1m today. Neighborhoodscout shows San Diego average appreciation in last 10 years is 115%, but in 13 years you have only achieved 66% appreciation.

https://www.neighborhoodscout.com/ca/san-diego/real-estate

Here is the reality on my active RE investments. My worse appreciating property has gained $2700/month of appreciation. I have 2 properties that have appreciated the over $10k/month over their hold. I have never purchased a property that at stabilization did not depict positive cash flow, but would not be adverse to buying a property with stabilized negative cash flow if the total return was high enough. My underwriting had never been significantly too optimistic.

by the way I have never sold books, course, anything. I have had a very successful protege (8 digit net worth and recently made ~$500k on a property repurpose) and a moderately successful protege and various protégés that are still working to find their way (no charge to any of them).

Now for what I agree with your post: 1) the RE market today may be the most challenging ever. Two recent studies show that renting has never been more favorable versus home ownership in large US cities. 2) active residential investing is not passive. If you want passive RE, be a LP, go NNN, or invest in a REIT. Because active residential RE is not passive, its return should far exceed passive options to compensate for the effort 3) without leverage and/or value add, there likely are many passive options that can match or exceed the return that will be achieved via active residential RE.

good luck