- Real Estate Agent

- Nashville, TN

- 180

- Votes |

- 363

- Posts

Affordability Crisis: We did this.

Welcome to the Skeptical Investor weekly article, right here on BP! A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

-------

This week, we’re talkin’ affordability, the new buzzword de jour. How did we get here? I place blame. I’m calling out names. I’m getting a little sassy.

You won’t want to miss this.

*** And yes, yes, I realize much of today’s piece is a little oversimplified, but hell this is a weekly newsletter, not a PhD, so hold your comments for my inbox.

Now, let’s get into it.

-------

Today’s Interest Rate: 6.29%

(👇.07% from this time last week, 30-yr mortgage)-------

The Weekly 3 in News:- - Putting housing prices and affordability in perspective: Home prices rose faster from 1977 to 1979 than from 2020-2022, and with mortgage rates rising from 8% to 13%! And 1943-1947 was actually the hottest home price growth on record in the US. We have actually seen this movie before (Mohtasahmi).

- - More Perspective: owning and holding assets is resilient in any economy. Consider this. Imagine you had the WORST timing ever. You invested the day before the 2000 crash. Then the day before the 2008 crash. Then the day before the 2020 crash. Then the day before the 2022 crash. You’d still be up over 200% today if you held and played the OWNERSHIP game (MarketHustle). Just own assets, I choose real estate.

- - As seen on the interwebs: when investing in someone else’s real estate deal. The devil’s in the details. Always read it!

Happy Monday y’all!

I’m feeling a little under the weather, so, I’m taking it out on my keyboard.

And on top of that, I have to move tomorrow (more on that next week).

So, excuse me for being a little punchy kicky.

And with that, let me tell you a story of how we got here to this affordability crisis.

And how it relates to real estate.

It’s a doosy.

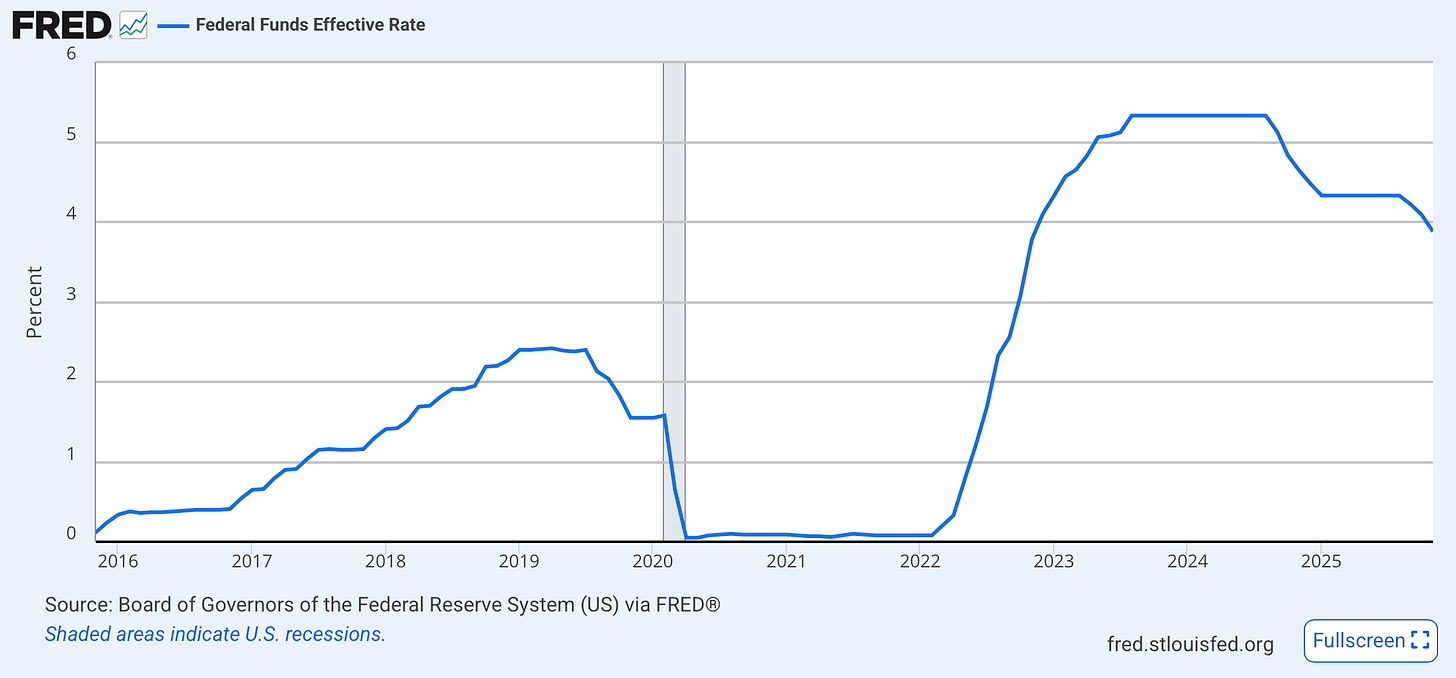

The Fed Cut, But Mortgage Rates Aren’t Down?

What a difference a week makes! After the Fed cut rates again last week, mortgage rates are now down to ….

Hey, wait a minute!

They’re not down at all!

That’s right, and readers of this newsletter knew this.

The bond market had already priced in a Fed rate cut in December. And investors in markets are forward-looking.

For 2026, 2 more cuts are now priced in: one in the Summer and one in the Fall.

Which means,,,,, mortgage rates won’t change much from now to the Spring.

Wait, what?!

That’s right, the bond market has already done much of the Fed’s dirty work for them, lowering rates to near 6%. And because this cut was assumed/priced in, we likely won’t see much shift from here until the next new announcement or significant change in Fed policy stance.

Of course, who knows what will happen in May once the President appoints a new Fed Chair?

TBD on that for now.

Get it? Got it?

Good.

The Fed and the Housing Market

Everybody’s talking about the interest rate cut, but I would like to focus on something else that Jerome Powell said during the press conference, as it relates to affordability, and that is:

And the transcript:

Yeah, so the housing market faces some really significant challenges. And I don’t know that, you know, a 25-basis point decline in the federal funds rate is going to make much of a difference for people. You know, housing supply is low. Many people have very, very low-rate mortgages from the pandemic period and they kept refinancing and caught the really low. So it’s made it expensive for them to move. And, you know, we’re a ways away from that changing. Also, we’re just -- we haven’t built enough housing in the country for a long time.

And so a lot of estimates suggest that we just need more housing of different kinds. So housing is going to be a -- you know, a problem. And, you know, really the tools to address it are -- we can raise and lower interest rates, but we don’t really have the tools to address, you know, a secular housing shortage -- a structural housing shortage.

Gosh, that was depressing.

But, I’d rate this partially accurate.

A few things:

Powell is technically correct. The Fed does not directly control housing supply or mortgage rates, and the Fed doesn’t really have the tools to address a structural housing shortage. The low-interest-rate lock-in problem will persist.

But they do control the base interest rate and liquidity in the economy, especially in real estate, such as through buying mortgage-backed securities.

In other words, the Fed can’t solve the housing affordability problem.

But they sure can **** it up.

And they did.

Affordability: What Happened?

The Fed did this.

(and Congress/Administration, more on that later).

Not on purpose. Not nefariously. But they did it.

And the road to hell is paved with good intentions.

A Quick History

The US government began reacting to COVID-19 on January 7, 2020, when the CDC established its Incident Management Structure to coordinate the response. This followed awareness of the outbreak from the WHO report on December 31, 2019, but January 7 marks the first formal internal coordination action by the US.

And in just a few short months - February to April - the Fed cut interest rates to ~0%.

And then came the money printer.

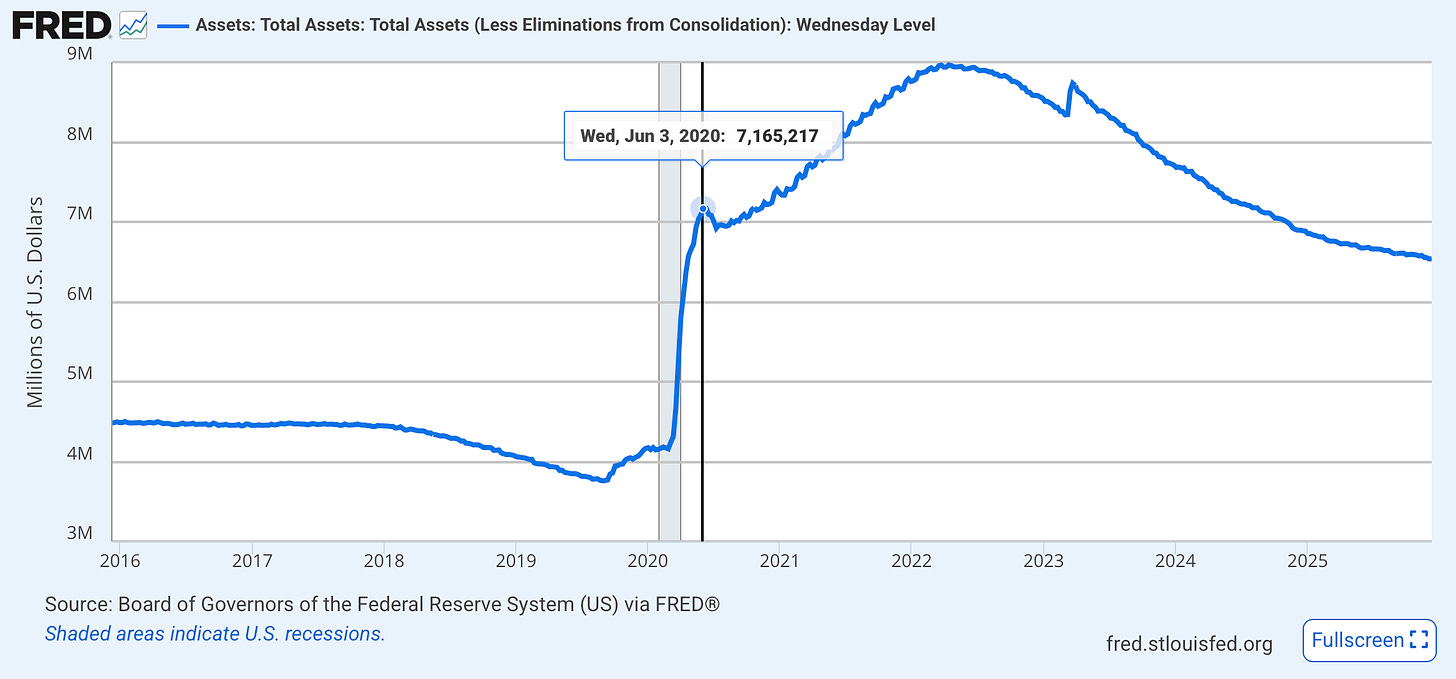

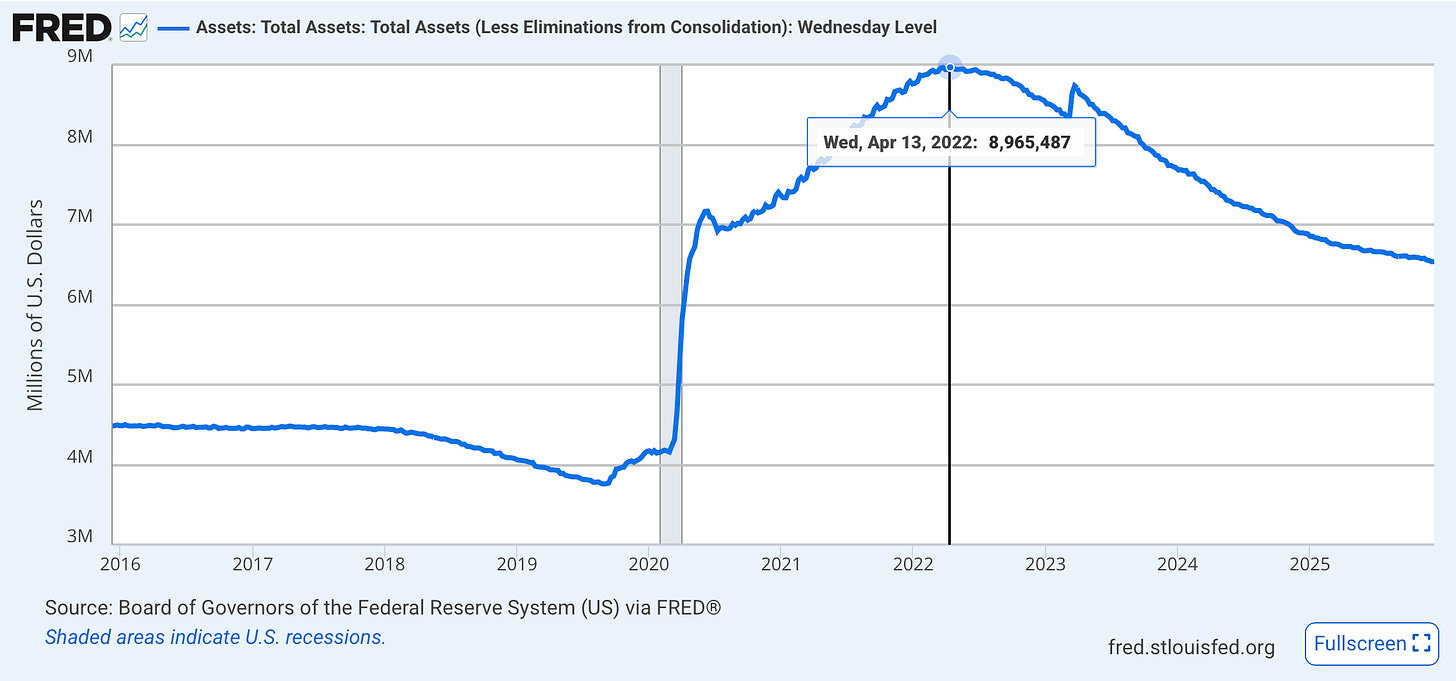

Shopping Spree 1:The Fed added/spent/bought $3 trillion in assets to its balance sheet in Feb 2020.

Treasuries (aka the money printer), bank debt/reserves and, of course, Mortgage Backed Securities (keep reading).

Shopping Spree 2:And then again, Spring 2020-Spring 2022, the Fed started another cycle, a continuous two-year buying spree, injecting another $1.8 trillion of liquidity into the US economy.

Money printer go brrrrrrr.

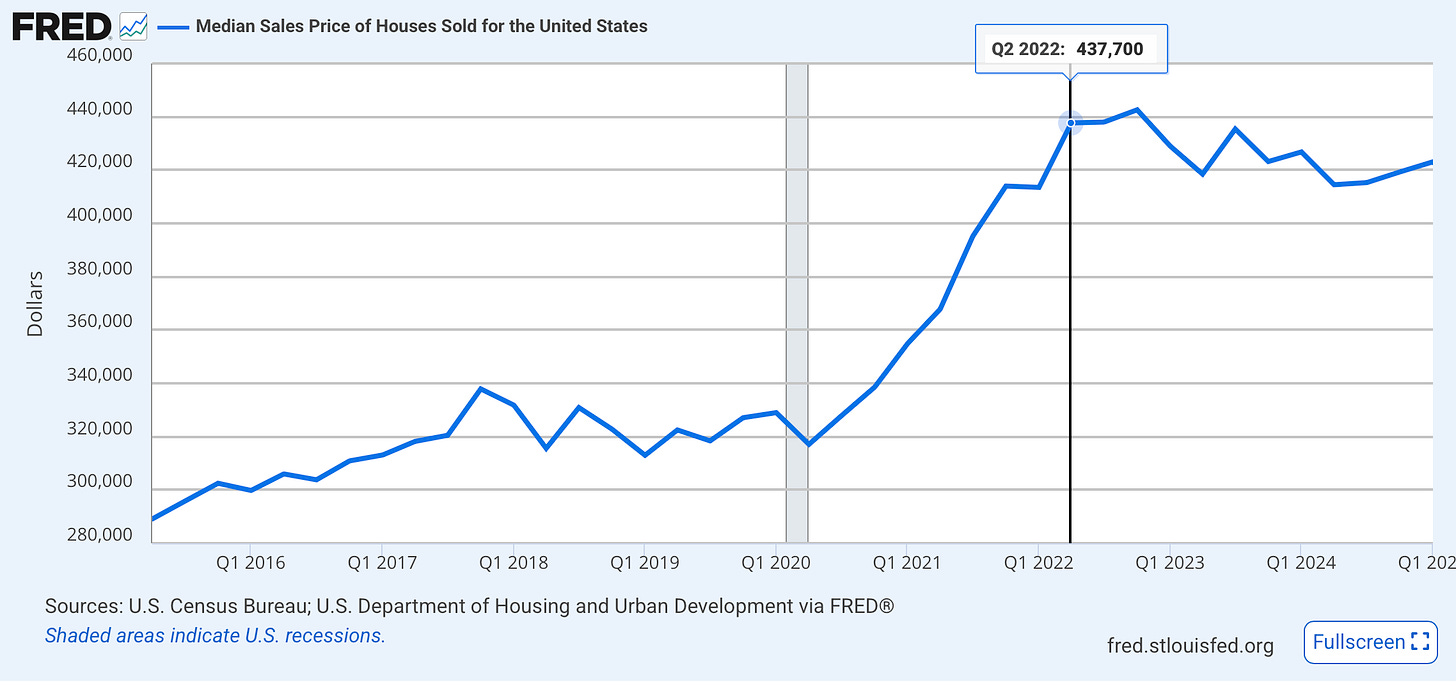

The Effect?Real estate prices rocketed up on demand from low rates, bank liquidity/desire to lend, and all that free money!

Median home prices went up ~20% YoY in 2020 and then again in 2021.

The Stock Market, too, was on an absolute bender, with rates low and money essentially free to borrow.

The Fed couldn’t get enough. Hell, it was even buying corporate bonds of blue-chip companies like Apple (CNBC).

Why?

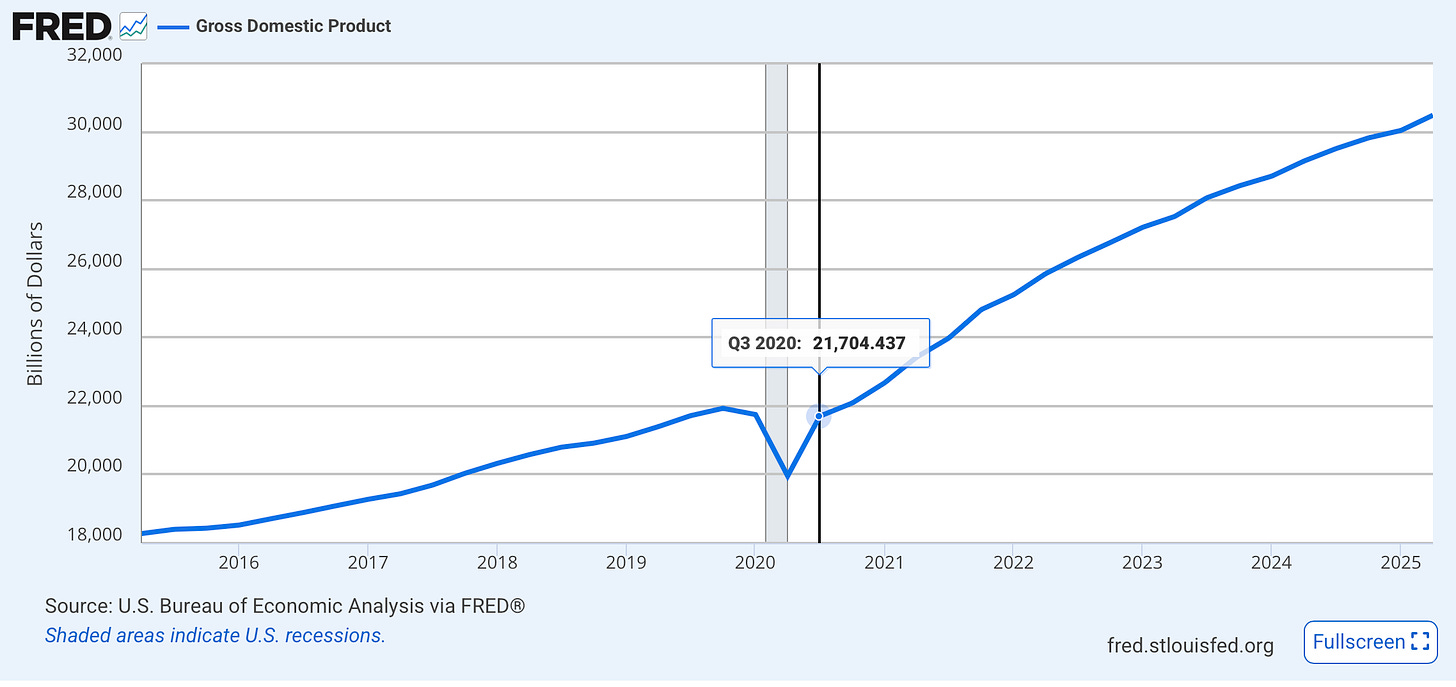

And this, despite the market having fully recovered from the February flash crash by August 2020.

And the broader US economy too had recovered by Q3 2020.

They just kept the printer printing. This was the problem.

For another year+!

But wait wait, there’s more!…

“Hey Fed, hold my beer.” - Congress

At the same time, Congress spent trillions.

$4.6+ trillion to be more precise.

To start, they enacted related to COVID-19 and for economic stimulus in 2020 and 2021, totaling $4.6 trillion (GAO).

More Spending: Infrastructure and Economic StimulusBut we didn’t stop there. We spent trillions more!

Congress then added $2+ Trillion more economic fiscal stimulus/spending in 2021, 2022 and 2023, which will take years to fully filter through the economy and keep prices elevated permanently. Congress and the Administration passed into law:

- --The Infrastructure Investment and Jobs Act - November 2021 - $500 Billion* to $1.2 Trillion*

- --The Inflation Reduction Act - 2022 - $433 Billion* (congress) to $1.2 Trillion* (Goldman Sachs) (*Bil proponents claim to offset spending with $400 billion in taxes and health care savings, but a recent analysis says it will actually cost 3x what was originally predicted by Congress). Important detail: the bill is really targeted at climate change and energy policy, not inflation reduction, as it is named.

- --The CHIPS Act - 2023 - $80 Billion (CBO) - $280 Billion. The total costs is likley more like $280 billion, on “new” direct appropriations of $80 billion.

Now, a trillion is a LOT of money.

A lot a lot.

During the Great Financial Crisis, the government spent less than $1 trillion across two major bills:

2020-2023 was just on another level.

This was total Idiocracy.

This is Why Inflation Up + Home Prices Up = Low Affordbility

This is Why Inflation Up + Home Prices Up = Low Affordbility

The Fed, Congress and both Executives (much on the latter Administration), is why we have an affordability crisis.

This why the price of everything is much much higher today.

But We “Had to Do It.”Now, you can argue it was necessary.

Sure, in the beginning. For the first 8 months of 2020, I’ll give you that.

But to continue spending + easing monetary policy in 2021, then again in 2022, then again in 2023?

No. Just No.

And Congress Tried to Keep it Going!Right in the middle of inflation alley, the Administration and Congress tried, and almost passed…

…checks notes…

…another $3.5 tillion in stimulus!

Thankfully, Senator Joe Manchin (D-WV) declined to support it, and it failed in the Senate. He details the saga in his new book, quite an unexpectedly wild read.

This would have meant even more gasoline on the affordability problem.

A deluge of money just dumped on the red-hot economy.

Thankfully, the US Government injected only ~$10 trillion.

It took a while. But we finally got on the wagon.

-------

My Skeptical Take:

It pains me to put it this way, but, we kinda are where we are.

During the 2020-2021+ time period, we had cheap money, so, people bought assets. A lot of assets. Many folks bought a house. And prices went sky high.

And it makes sense.

Who wouldn’t take advantage of free money?

Who wouldn’t take advantage of historically low interest rates?

But unfortunately, we are in the mess now, and the Fed can’t solve the housing affordability problem.

And if the Fed or Congress start the money printer again or lowers interest rates rapidly, affordability will not be bettered.

In fact, prices will go up with more liquidity in the market.

The cure is time.

It's not a great answer.

I know it's not what you wanted to hear, but that's it.

The market can absorb these structurally, permanently higher prices by growing the economy and ensuring wage growth is robust.

And with only 2 rate cuts likely in 2026, high-er roughly 6% rates will help keep asset prices from inflating (2 cuts in 2026 should be viewed positively, it means the economy continues to be strong).

That's really it. There's no magic pill. Ozempic won't do it.

The Good NewsThe good news is we have taken some of our medicine.

Some of the gas has been let out of high home prices and thre is a wall of worry that is is preventing the “bubble” that everyone’s afraid of.

That’s what we’re seeing play out, and it will keep us on track to a much healthier market in 2026 and beyond.

This natural.

So get out there. It’s time to do the work.

Make offers. Find deals. Real estate is about opportunity, NOT the market.

I’ve made money in much worse markets than this. Especially on the buy side.

After all, in life, you get what you negotiate, not what you deserve.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

-The Skeptical Investor

P.S. Reach out! I always like talking real estate with BP folks. Hope you enjoyed.

- Andreas Mueller