Austin Market Report - April 2026

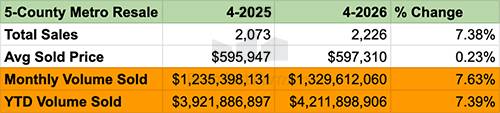

The April 2026 data for the Austin, Texas metro shows a spring market with stronger buyer activity than we saw last year. Pending units increased 17% year-over-year, total sales climbed 7.4%, and total dollar volume increased 7.6% to $1.63 billion for the month.

Pricing remains mixed. Average sold price was essentially flat on a YOY basis, while median sold price was still down 2.9%. Months of inventory dropped from 5.8 last April to 5.3 this April, but average days on market increased from 77 to 85 days. In other words, demand has clearly improved, but buyers are still selective.

Key Highlights

- Total Sales increased 7.4% YOY in the Metro, with Total Volume Sold up 7.6% to $1.63 billion.

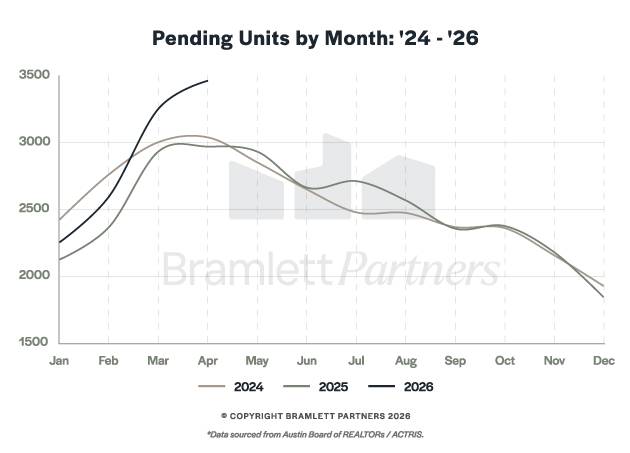

- Total Pending/Under Contract units increased 17% YOY, making it one of the clearest signs of improved buyer activity this month.

- Average Sold Price was essentially flat at +0.2% YOY, while Median Sold Price declined 2.9% to $435,250.

- Months of Inventory declined to 5.3 from 5.8 last April.

- Average Days on Market increased to 85 from 77, showing that stronger buyer activity has not eliminated longer marketing timelines.

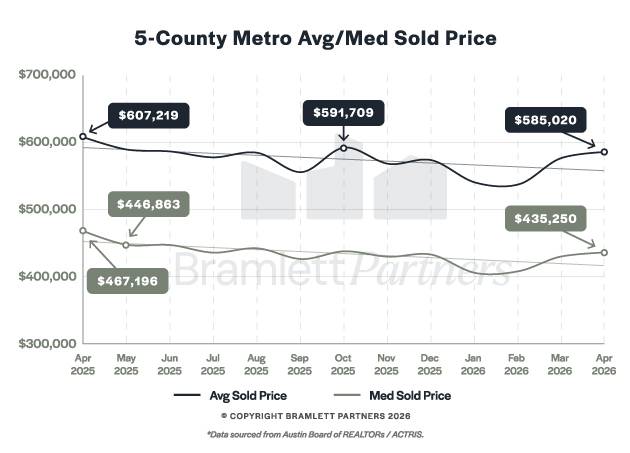

Avg and Median Prices Show Signs of Stabilizing

Average and median sold prices are telling slightly different stories this month. Average Sold Price was basically flat YOY at +0.2%, while Median Sold Price declined 2.9%. Average Sold Price per square foot also declined 3.4%, which suggests buyers are still getting more house for their money than they were a year ago.

The month-over-month trend is more encouraging than the year-over-year comparison. Both average and median prices moved up from the softer winter levels, which is consistent with normal spring seasonality. I would not read this as a major price rebound, but it does suggest that pricing has firmed up from the softer winter levels.

Pending Units Show Real Demand Growth

Pending units are the most important data point this month. Total Pending/Under Contract units increased 17% YOY, and the 2026 pending unit curve is tracking ahead of both 2024 and 2025 through the first four months of the year.

The April increase suggests that buyers are actively engaging with the market, even though rates remain higher than many buyers would prefer. Affordability remains a major constraint, but the contract activity shows that more buyers were willing to move forward in April.

This does not mean Austin has returned to a 2021-style market. Inventory is still healthy, buyers still have options, and pricing remains important. But compared with last year, the demand side of the market is clearly stronger.

New Listings Are Tracking Close to Last Year

New listings in April came in at 5,753, down 0.7% YOY. That is essentially flat, and the 2026 new listing curve is tracking very closely with 2025 so far.

This is an important part of the story. The improvement in demand is not happening because sellers have disappeared. Sellers are still coming to market at roughly the same pace as last year, but more buyers are writing contracts.

At the same time, not every listing is succeeding. Seller Success Rate came in at 64.9%, meaning roughly one-third of listings are still expiring or being withdrawn rather than closing. That reinforces what we’ve been seeing on the ground, where homes that are priced and presented well are moving while overpriced listings are still sitting.

This also matches the hyperlocal nature of the current market. Some areas and price points are seeing stronger activity, while others still feel slow. The market is improving, but it is not improving evenly.

Inventory and Days on Market Still Favor Discipline

Months of Inventory declined from 5.8 last April to 5.3 this April, which is a meaningful improvement. That said, 5.3 months of inventory is still a much more balanced environment than the extremely tight market Austin saw a few years ago.

Average Days on Market also increased from 77 to 85 days. That may seem at odds with stronger pending activity, but it makes sense in the current market. Buyers are active, but they are not rushing into every listing. They are comparing options, negotiating, and passing on properties that feel overpriced or poorly prepared.

For investors, the current market is easier to underwrite than the 2021–2022 market in some ways, but harder in others. There is more inventory, less urgency, and more room to negotiate. At the same time, higher financing costs, insurance, taxes, and flatter resale prices leave less margin for error.

One broader backdrop worth keeping in mind is that the Austin metro is still growing, but growth is increasingly uneven. The city of Austin recently crossed the 1 million resident mark, while many of the fastest-growing areas remain in the suburbs and outer-ring communities. That helps explain why broad metro stats can mask very different neighborhood-level realities.

If you’re a buyer

The spring 2026 market still gives buyers meaningful choice. Inventory remains healthy at 5.3 months, median sold price is still down 2.9% YOY, and many sellers are willing to negotiate. However, the 17% increase in pending units shows that buyer activity has picked up. Well-priced properties are seeing more attention than they were six to twelve months ago, especially in certain neighborhoods and price points.

If you’re a seller

The selling environment has improved, but pricing strategy still matters. The 64.9% Seller Success Rate is the reality check. About one-third of listings are still not making it to closing. Sellers who price realistically, prepare the home well, and respond to feedback are in a much better position than sellers who anchor to older pricing expectations.

Always remember that real estate is hyperlocal and situation-specific. Metro-level data is useful, but neighborhood, property type, condition, pricing, and seller motivation can all change the picture quickly. If you’d like to talk through your plans or a specific property, I’m always happy to help.