- Real Estate Agent

- Nashville, TN

- 180

- Votes |

- 365

- Posts

The New Fed Wants It Both Ways.

Hello fellow BP Compatriots!

This week, we’re talkin’ oil backs down below $100/barrel, home builders pull permits, and the new Fed Chair telegraphs what he has in mind for the future.

Also: Nashville Class A rentals just turned positive, 6+ months ahead of peer Sun Belt cities.

Let’s get into it.

--------

Today’s Interest Rate: 6.65%(flat from this time last week, 30-yr mortgage)

Same level as last Friday, after a four-day +23 basis point repricing the week before that. The bond market looked at this week’s incoming data and decided to wait.

--------

The Weekly 3 in News:

- --Kevin Warsh, sworn in as Fed Chair on Friday May 22, delivered a first speech promising “inflation lower, growth stronger, real take-home pay higher.” The framing was deliberately bilateral. Hawkish commentators expected an inflation-first message; they did not get one. (CNN, May 22; Invezz, May 22)

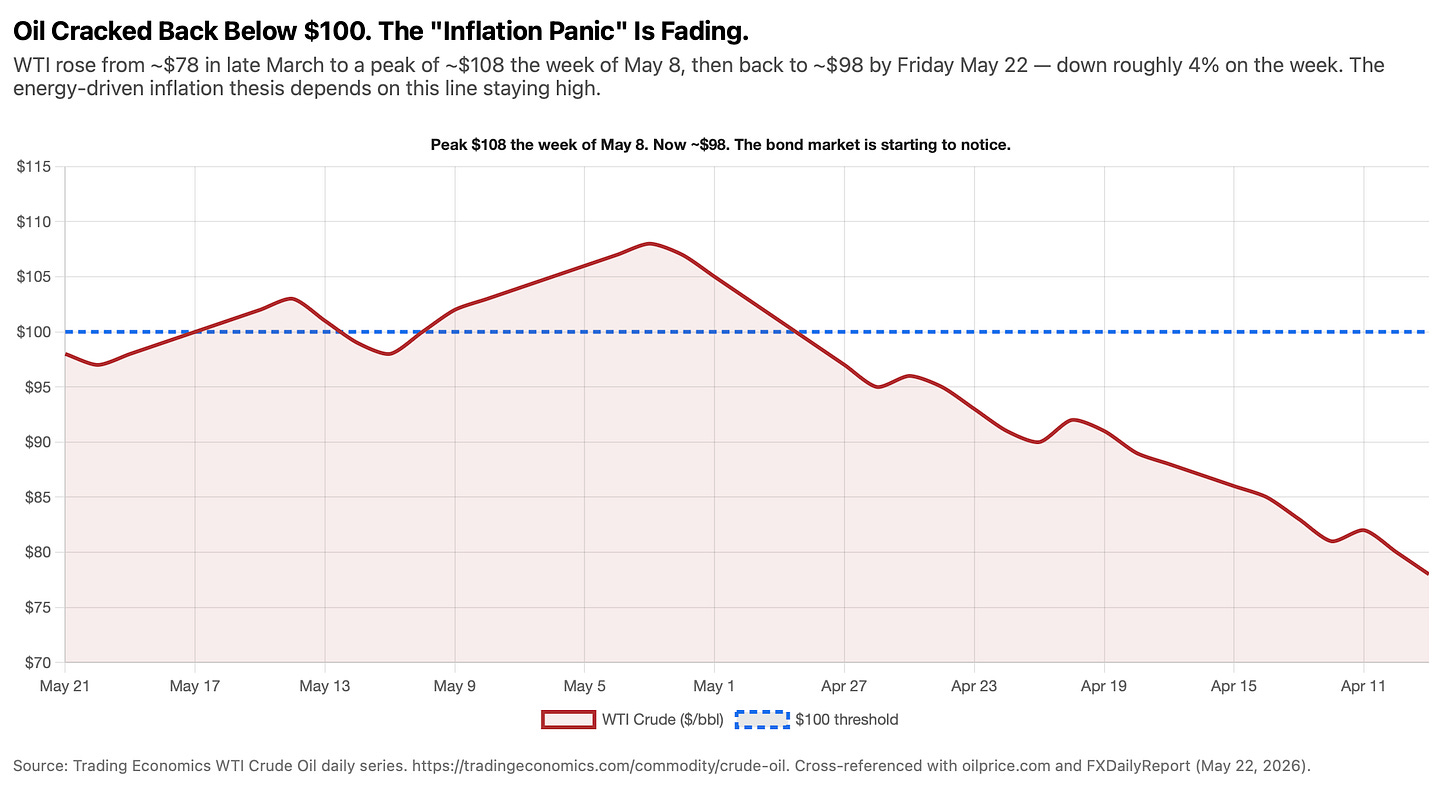

- --WTI crude closed Friday around $98 per barrel, down roughly 4% on the week, after Iran de-escalation headlines midweek and a Khamenei statement Friday on enriched uranium. The peak two weeks ago was ~ $108. (Trading Economics WTI; FXDailyReport, May 22)

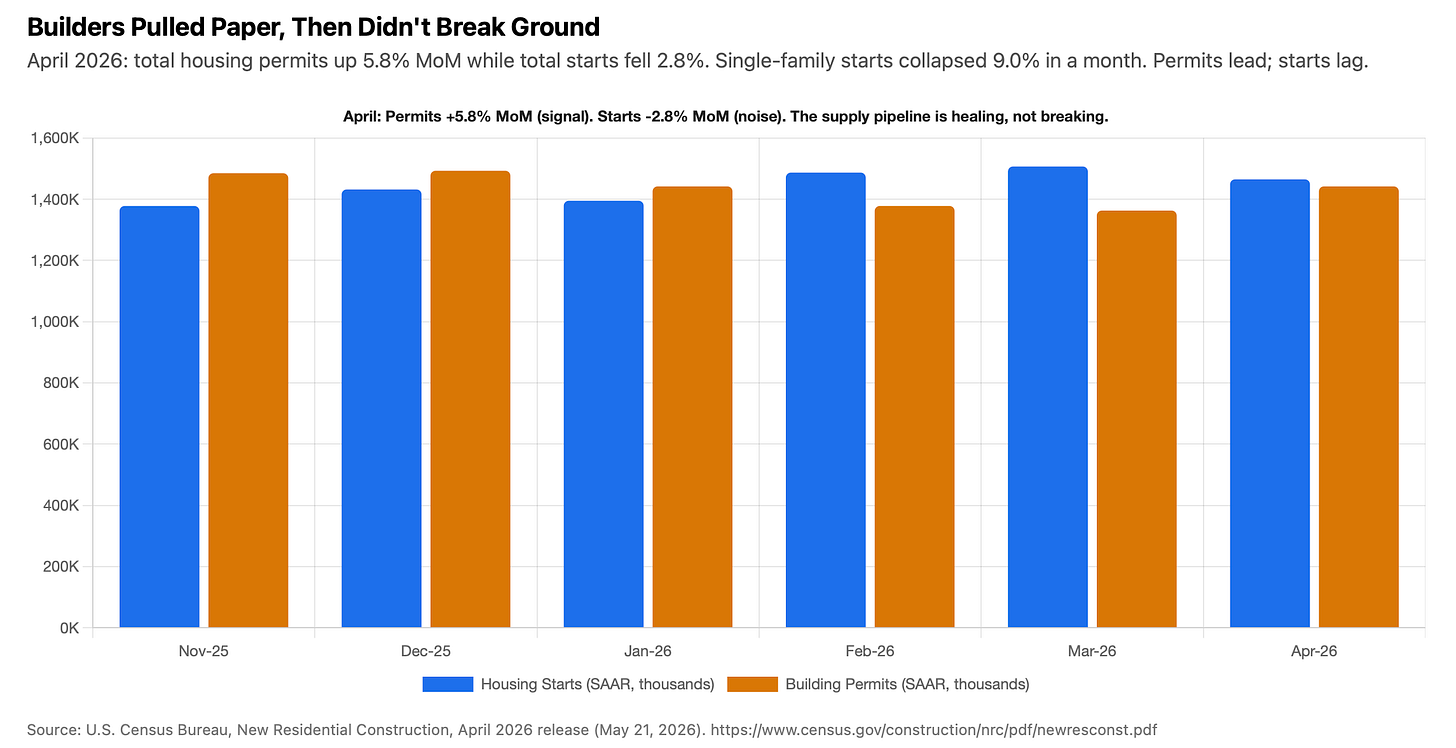

- --April housing starts came in at 1.465M annual run rate, down 2.8% MoM; new single-family starts collapsed 9.0% MoM. But April permits printed at 1.442M, up 5.8% MoM. Builders pulled paper (ie got approved building permits) at a brisk pace and then didn’t break ground, fearful of higher for longer interest rates. (Census, May 21)

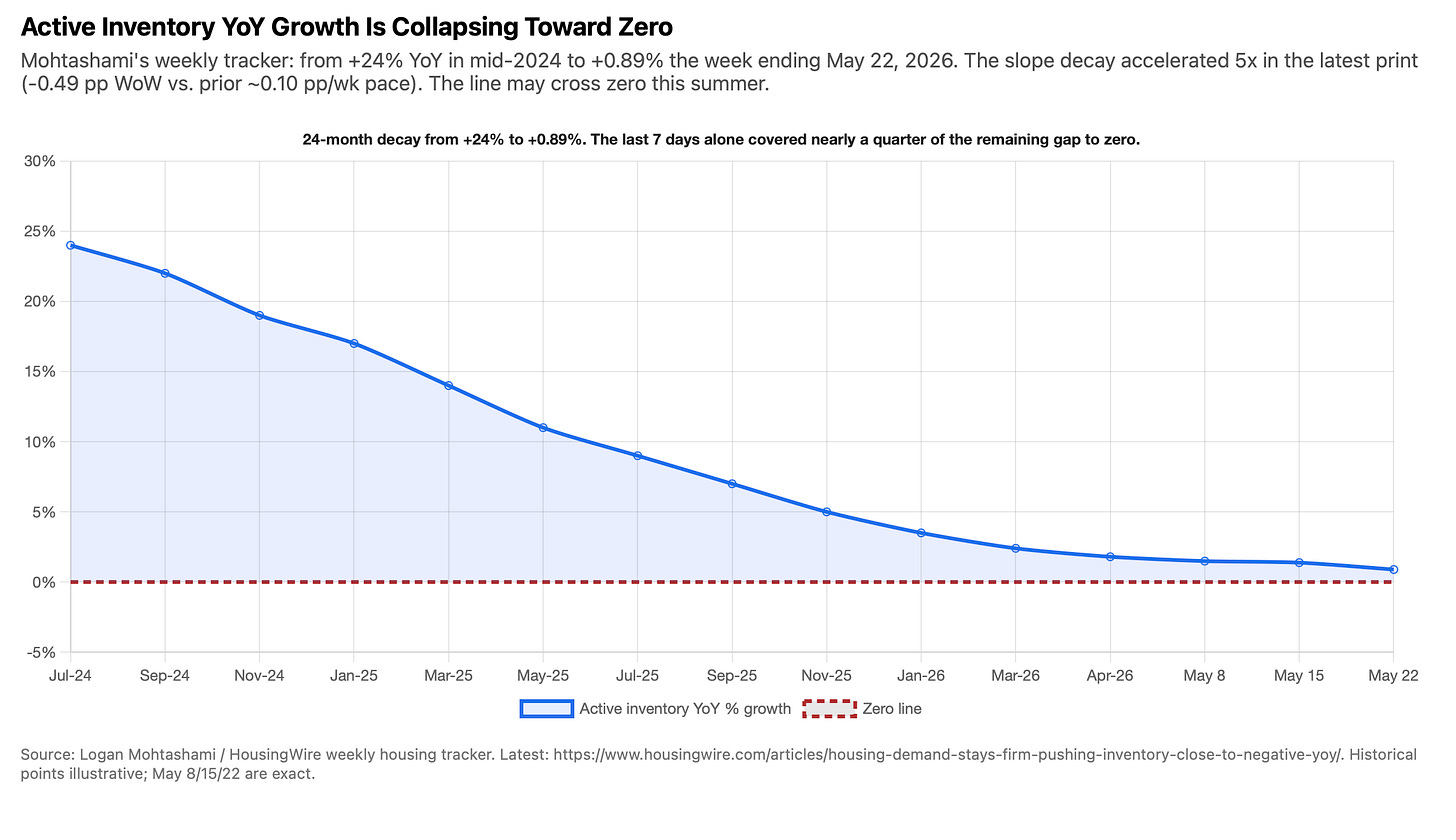

-- Bonus! Housing Analyst Logan Mohtashami’s weekly inventory tracker is showing lower inventories: +1.38% YoY a week ago to +0.89% YoY for the week ending May 22, the biggest single-week deceleration in months. Active inventory rose 16,373 units this week against 20,037 in the same week of 2025. Pending sales are up 9.8% YoY. In summary: demand is intact; but sellers are pulling back and not putting their home on the market. (HousingWire, May 23)

A Few Fun Things Happening in Nashville This Week- --Full Moon Pickin’ Party, Percy Warner Equestrian Center, Friday May 29 from 6 to 10 PM. First Pickin’ Party of the 2026 season. Bluegrass under the stars: Backroads Grass, Amy Alvey & The Home Team Advantage, The Green Hillsbillies. $25, kids under 12 free. Proceeds benefit Friends of Warner Parks. (Warner Parks)

- --Music City Rodeo + headliner trifecta at Bridgestone, Thursday through Saturday May 28 to 30. PRCA ProRodeo every night, then a country headliner. Thursday is Miranda Lambert, Friday is Charley Crockett, Saturday is Jon Pardi. Three nights of rodeo and country royalty in the building that anchors downtown. Tickets at musiccityrodeo.com. The kind of week that reminds you why Nashville is THE live music capital.

-- Bonus - Local Rodeo

Nearby Cheatham County had it’s rodeo this past weekend, which I attended. It was a full-on mud bowl, and it was fantastic.

Was at a party before hand, and I even got up on the bull.

Obligatory picture below.

Didn’t do too bad. But wow, it’s not as easy as it looks.

Ok, enough of that, now back to business…

--------

Builders Pulled Paper. They Didn’t Break Ground.

Fresh April housing data dropped Wednesday, and the headline was easy to misread.

Total housing starts were at a annual run rate (SAAR) of 1.465 million, down 2.8% month-over-month, but up 4.6% year-over-year. Single-family starts were at 930,000, down 9.0% MoM, a meaningful drop. Multifamily 5+ starts rebounded modestly to 529,000 after a soft March. (U.S. Census, May 21)

But building permits came in at 1.442 million, up 5.8% MoM, down only 0.2% year-over-year. (Census, May 21)

This is a bearish signal on new deliveries.

Key Takeaway: permits lead starts; starts lead deliveries; deliveries determine the supply that competes with the asset we as investors own. Thus, lower numbers like this are bullish/inflationary for rents.

So what happened in April?

Mortgage rates spiked: the 30-year per rose from a low around 6.31% in mid-April to 6.56% by early May, while the MND daily index touched 6.66% on May 13. (Freddie Mac PMMS; MBA Weekly Survey)

Builders who had been planning to break ground in April looked at their rate-locked cost-of-capital, looked at their pipeline, and chose to wait.

Maybe a few weeks, maybe a few months.

The paperwork still got pulled because permits run with longer lead times, but the shovels didn’t hit the dirt.

This pattern is consistent with what builders historically do in a volatile interest rate environment.

They preserve optionality. They keep the land entitled, the paper filed, and the capital deployed on existing in-progress projects.

When rates settle, they start. When rates rise further, they don’t.

For our purposes, the most important takeaway from a 9.0% MoM single-family starts drop is not “the homebuilding industry is collapsing.” It is “the supply that would otherwise hit the market in 2027 may now be smaller than the consensus expected.”

Permits at 1.44M SAAR is consistent with roughly 1.3 to 1.4M annual deliveries in the 12 to 18 months ahead. That is meaningfully below the 1.5 to 1.6M needed to maintain a balanced national market, given household formation that the Joint Center for Housing Studies estimates at roughly 1.0 to 1.2M new households per year plus the replacement demand of an aging stock.

Plus, the permits print is not the only data point. April NAHB Housing Market Index improved (see below), inventory is collapsing (see below), and purchase mortgage applications, while down 4% WoW, are not down on a YoY basis.

--------

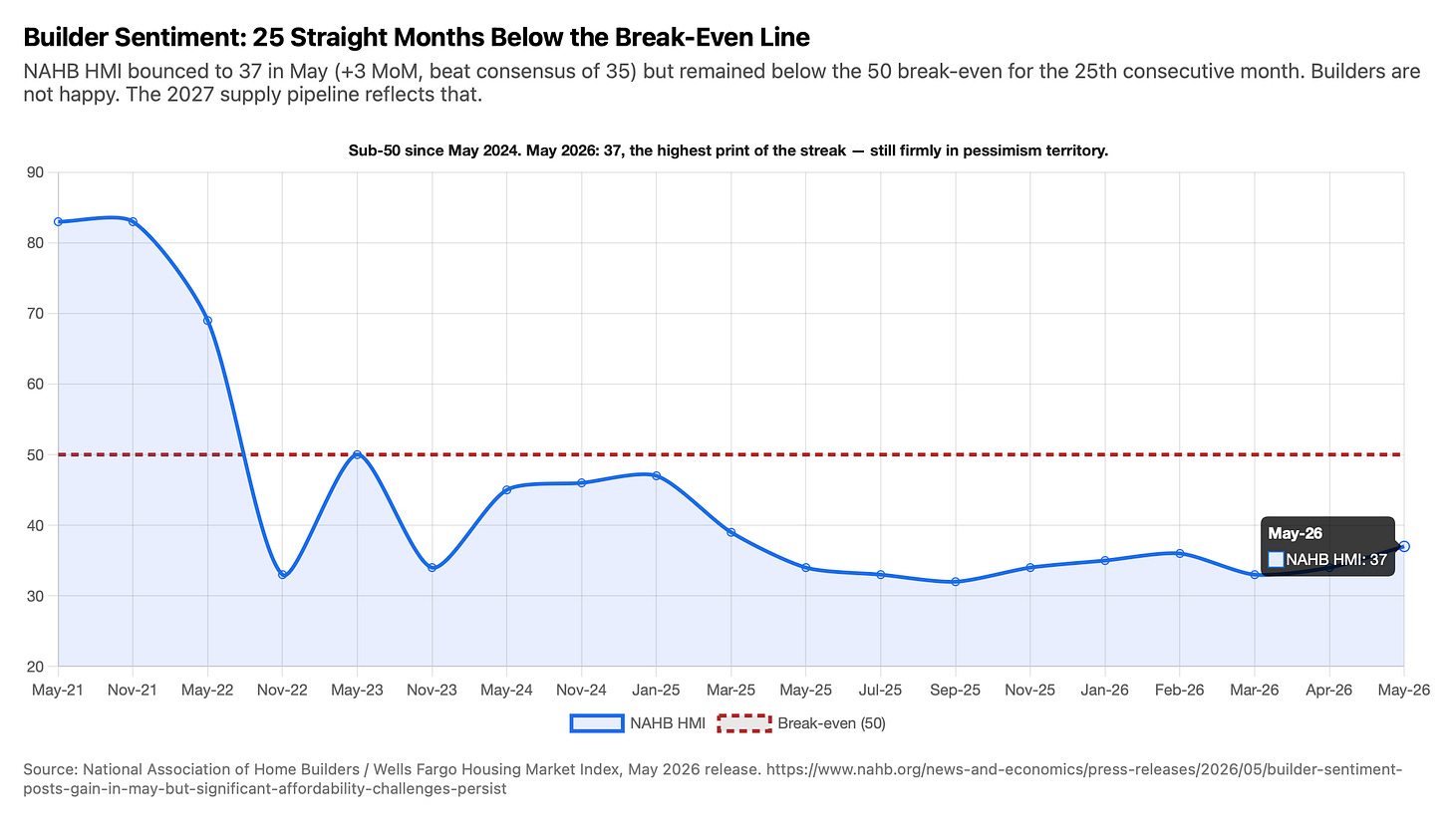

Builder Sentiment Up. Just Not Above 50.

The NAHB Housing Market Index for May printed at 37, up 3 points month-over-month, beating consensus of 35. (NAHB, May 18) Current sales conditions rose 3, future sales rose 3, traffic of prospective buyers rose 3.

That sounds like a good print, and on the margins it is.

But it is also the 25th consecutive month with a reading below the 50 break-even line that separates “more builders optimistic than pessimistic” from its opposite. The last time the HMI printed above 50 was in mid-2023. (NAHB historical data)

Fewer Price Cuts?

The underbelly of the May report is even more interesting.

The share of builders cutting prices fell from 36% in April to 32% in May, the lowest in seven months. But the average price cut grew from 5% to 6%. Translation: fewer builders are discounting, but the ones who are have to discount harder. (NAHB, May 18) Sales incentives ran at 61%, the 14th consecutive month at or above 60%. The structural mismatch between asking price and what the consumer can afford is still the dominant feature of the new-build market.

My Take: This is the picture you would expect at the trough of a building cycle. Builders are not happy. But they are also no longer panicking, and the marginal builder is no longer accepting heavily discounted offer prices. That second piece is a leading indicator for a pricing power come back, which is bullish for existing rental stock because the squeeze on the build side translates into less competition for renters in 2027.

--------

Is the Bond Market Finally Admitting it Was Wrong?

Two weeks ago, in my article Forget Inflation. Watch the Labor Market., my argument was that the bond market had repriced the rate-cut trade on the back of an inflation print that was really an energy volatility story.

Whew, say that 3 times fast.

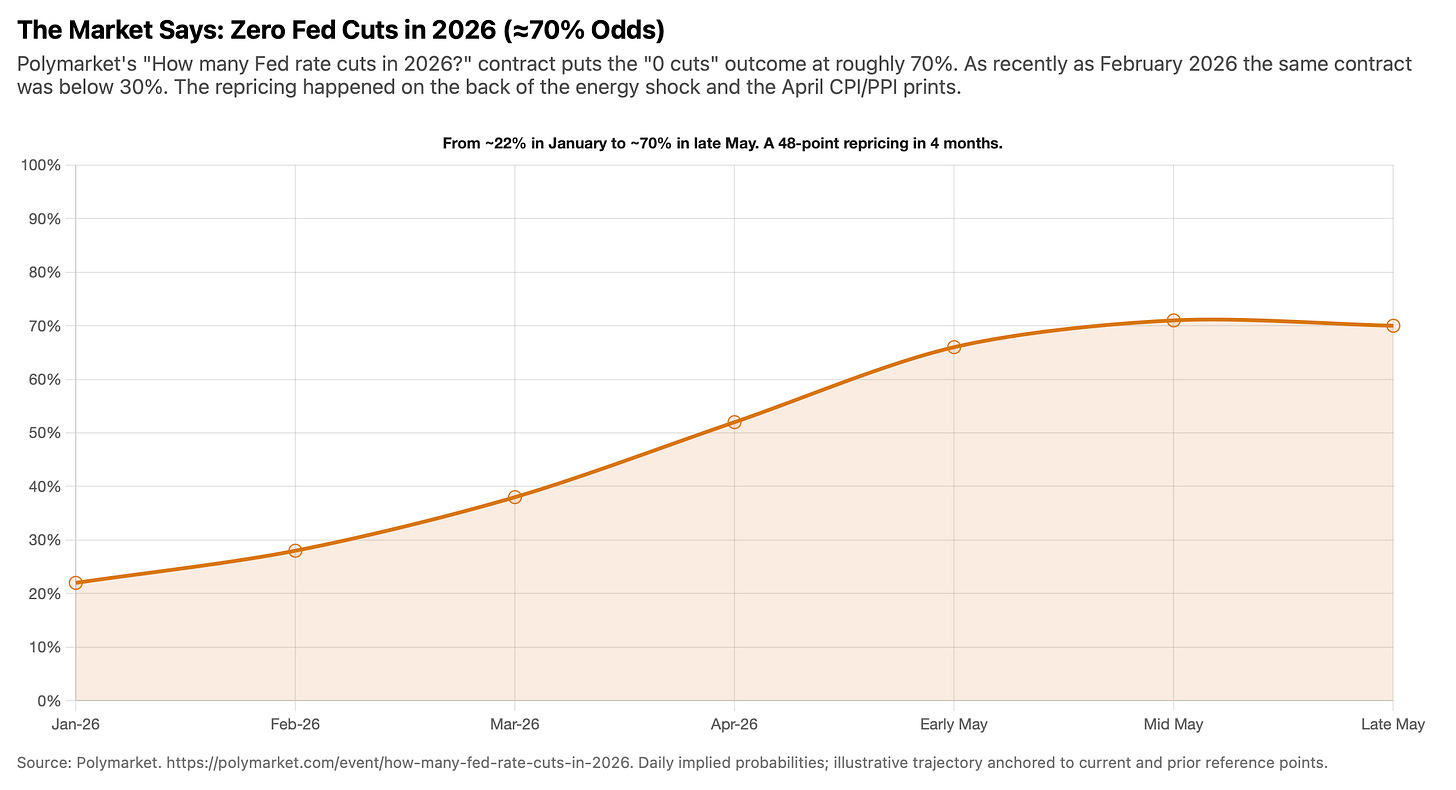

April CPI inflation was running at at 3.8%, April PPI at 6.0%, and the bond market priced “zero cuts in 2026” at roughly 70% likelihood. (BLS CPI release, May 12; BLS PPI release, May 13; Polymarket)

This week, we got three pieces of evidence that support my theory: the bond market may be offsides (and thus interest rates will come down).

1)) Oil receded back below $100.

WTI peaked at roughly $108 the week of May 8, then drifted lower into Friday May 22 as Iran de-escalation headlines hit the tape and Saudi Arabia’s production posture eased. Friday’s close was approximately $98, down 4% on the week. (Trading Economics WTI)

That matters because the entire bond-market case for “no cuts in 2026” was built on the assumption that energy stays elevated through summer and that the headline CPI prints continue to run hot. If oil sits at $98 through June, the May and June CPI prints will be cooler than April’s, perhaps materially so.

The risk premium embedded in oil right now is best framed against the Scary Movie 7 thesis from March: the Strait of Hormuz tax on world oil prices has been a structural anti-feature since at least the 2010s. The energy spike of the last six weeks was that tax compounding with a tighter inventory backdrop, not a fundamental shift in inflation or prices.

As the headline risk eases, the tax declines. As the tax declines, the inflation prints should cool.

2)) Warsh’s first speech as Fed Chair.

Sworn in at the White House on Friday May 22, Kevin Warsh delivered remarks that were striking for one reason: what they did not say.

He did not promise inflation as job one and he did not commit to keeping policy restrictive until inflation hit 2%.

He framed his Fed as growth-friendly: “inflation can be lower, growth stronger, real take-home pay higher.” (Invezz, May 22; CNN, May 22) He also explicitly framed his future Fed reign as “reform-oriented,” which is the language a Chair uses when he intends to depart from his predecessor’s framework.

The bilateral framing matters because Warsh inherits an FOMC with four members who have been openly against cutting rates (and potentially politically opposed to the current Administration).

A committee with that internal structure does not produce bold moves. It produces small, hesitant ones, and Warsh’s bilateral rhetoric appears to be an attempt to thread that needle and keep the dovish wing engaged, while the hawkish wing manages downside inflation risk.

The bond-market implication, which I wrote about two weeks ago, is that Warsh may move on the balance sheet before he moves on the funds rate. Accelerating quantitative tightening would tighten financial conditions without forcing a politically expensive rate hike. Two-sided risk language plus QT acceleration is a reasonable read of the June 17 setup, in my humble opinion.

3)) Inventory growth is collapsing.

Contrary to popular belief, weekly active-inventory housing numbers are still showing inventory dropping.

Last week it stepped down from +1.49% the week of May 8, to +1.38% the week of May 15, to +0.89% the week of May 22. This single-week deceleration of 0.49 percentage points is roughly five times the prior pace. (HousingWire, May 23)

Why does this matter for rate-cuts?

Because the bond market’s inflation worry is largely a shelter cost worry. Shelter is nearly 33% of the CPI inflation number, and shelter inflation lags both actual rents and home prices by roughly 12 months. If active for-sale inventory growth flips negative this summer, the cooling shelter print that the Fed has been waiting for would arrive later, not sooner, and at a higher base than the consensus had built into models.

That is hawkish for shelter inflation, which sounds bad for future interest rate cuts.

But here is the second-order effect:

If shelter inflation stays sticky for structural reasons (low inventory) rather than cyclical reasons (overheated demand), the Fed has to weigh the cost of holding restrictive policy against an inflation print it cannot fix with restrictive policy.

This is the moment the Fed historically pivots toward growth, and lowers rates.

My Thought Process: Why Rate Cuts are in Order.

My Thought Process: Why Rate Cuts are in Order.

First, the front end of the bond market may be mispricing 2026.

Polymarket is telling us that folks see a 70% chance of “zero cuts,” true. But I think this looks like a momentum trade by traders who have not yet reset to the new inflation information. If oil sits at $98 through June, the CPI prints cool, and Warsh signals balance-sheet acceleration at the June 17 meeting, the cut-count contract should drift back toward “one or two cuts in 2026.” All this within the next four to six weeks.

Second, mortgage rates have probably topped for this cycle.

The 30-year mortgage at 6.65% is consistent with a 10-year Treasury yield near 4.55%, and the 10-year peak this month was approximately 4.62%. If the long-run inflation expectation does not get repeated in June, the 10-year sinks lower from here, and the 30-year sinks with it. That does not mean rates “crash”; that means the asymmetric risk on rates increasing from this level is way down and overall rates are modestly down, as opposed to the consensus now which is modestly up.

Third, the operator’s window has shifted from “wait for clarity” to “buy first, ask questions later.”

The clearest tell of a market bottom is when the macro picture is contradictory and the consensus is wrong. Right now the macro picture appears contradictory: we have 8 straight weeks of S&P gains (Motley Fool, May 22) against a 74-year-low consumer sentiment, a hawkish FOMC dissent count against a growth-friendly new Chair, inflation that’s hot, but driven by an energy shock that may already be unwinding.

Markets do not give you certainty; they give you contradiction, and they reward people who position correctly during contradiction.

I think this is where we are.

--------

Nashville Corner: Super Bowl LXIV Coming to Nashville in 2030!

The Titans will have a new stadium next year and that usually brings one big new thing: a super bowl hosting opportunity.

And Nashville just clinched it.

Yes, Nashville has been selected to host the Super Bowl 2030, and Legendary CBS broadcaster Jim Nantz is fired up!

On the city hosting the game, Nantz espoused the magic of the music city, saying,

Nantz predicts the game will be "the greatest event" ever hosted, with massive pregame show live from downtown Broadway, similar to the 2025 celebration in New Orleans’ French Quarter. (Tennessean)

Fun fact, Nantz is a Tennessean, as of 2021. He, of course, has a little something different in his country home outside the city.

Pretty slick.

--------

My Skeptical Take

After last week’s inflation numbers, I am - let’s call it - 20% more positive than I was the week previous.

The bond market priced the inflation panic of two weeks ago, and this week three quiet data points appeared that may begin to unwind that stance.

At the same time, housing inventory growth is collapsing toward zero on a YoY basis, with the latest week showing the biggest deceleration in months.

Case in point: here in Nashville, Class A rent just turned positive, six to twelve months ahead of peer Sun Belt metros.

None of these is a single-data-point case for the rate-cut trade reawakening.

But all of them, in combination, may be.

The macro picture this week was genuinely contradictory: equity markets at record highs, consumer sentiment at a 74-year low, builder sentiment 25 months below 50, mortgage rates near a yearly high, oil cracking lower into the Memorial Day weekend, a new Fed Chair signaling reform. Contradiction is the bottom-formation pattern. Clarity is the top-formation pattern.

Earl Nightingale, the motivational broadcaster who put the line on tape in 1956, defined success this way:

The word in that sentence that earns its keep is progressive.

Not the moment of arrival.

The realization. The continuous, compounding work of moving in the right direction.

We real estate operators feel that in their bones.

The thesis this week is not that rates will get slashed at the new Fed’s first meeting June 17. The thesis is that the deals you underwrite this month, the financing relationships you stack now, the amazing broker you contact today, the buy-list you build into Q3, the rent-roll discipline you enforce at every renewal, the underwriting standards you refuse to abandon when other operators do…. those are the progressive realization.

The interest rate cut, when it comes, and it will come, is the moment the rest of the market notices what you have already been building toward.

That is the definition of success that survives a contradictory macro environment.

So the disciplined operator prepares for the reawakening of the cut trade without betting the portfolio on its timing.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

-The Skeptical Investor

—

P.S. Want to talk real estate? I always do, drop me a line here on BP.

- Andreas Mueller