How do you decide whether to sell, refi, 1031 exchange, or hold?

I see a lot of investors struggle with this question, especially after owning a property for several years.

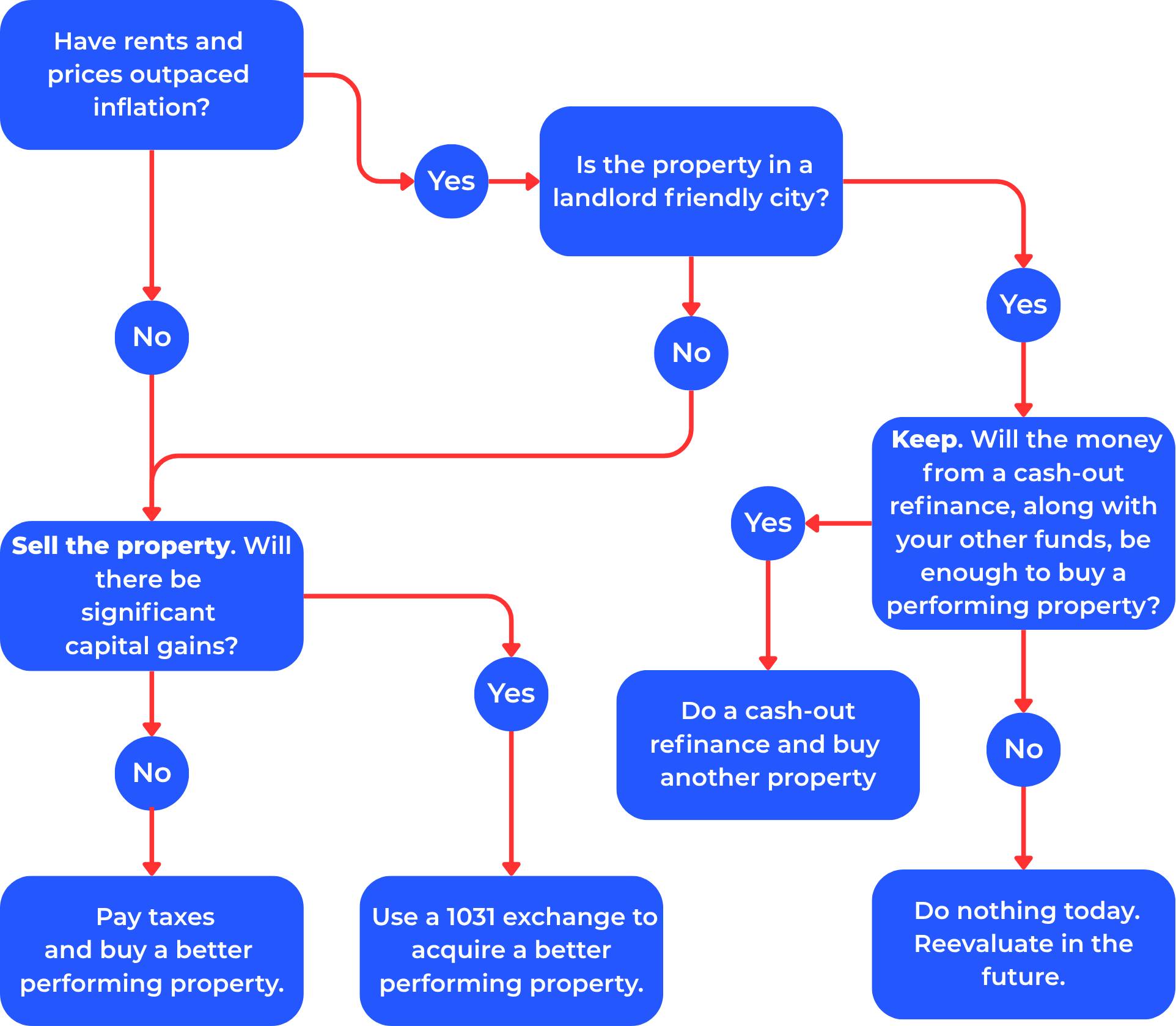

The way I think about it is pretty simple:

Does the property still support your long-term financial goals?

That sounds obvious, but I don’t think it can be answered by looking at cash flow alone. I would look at a few things:

- Has rent growth outpaced inflation over the last 5 to 7 years?

- Has appreciation been strong enough to justify keeping the equity in the property?

- Are taxes, insurance, maintenance, and vacancy costs eating up too much of the income?

- Is the property in a landlord-friendly market, or are local regulations starting to create more risk?

- If you sold or exchanged, could you move the equity into something that performs better?

The part that gets overlooked, in my opinion, is net rent, not gross rent.

A property can look good based on rent alone, but if insurance, property taxes, vacancy, turnover, or maintenance are too high, the actual income may not support the investment thesis anymore.

For example, if one market has much higher insurance and property taxes than another, that property has to generate more rent just to produce the same net result. Otherwise, the investor may be taking on more risk without getting paid for it.

Same issue with vacancy. A property with a tenant who stays five years is very different from a property that turns every year, even if the monthly rent looks similar.

My rough decision framework is:

- Hold if the property is still producing reliable income, rents are growing faster than inflation, and the market still supports the long-term goal.

- Refinance if the property is strong, but trapped equity can be used to buy another good property without weakening the original investment.

- 1031 exchange if the property has appreciated, but the income, tenant quality, operating costs, or market outlook no longer justify keeping it.

- Sell if the property no longer fits the goal and there is no better exchange opportunity, or if the investor needs to simplify.

Curious how others think about this.

- Eric Fernwood

- [email protected]

- 702-358-8884

Most Popular Reply

Another thing is your age, and family situation. I am now over 70, my kids do not want to engage in rental income, so I am slowly trans-ing to DST income. As tenants move I fix them up, sell them, and tax defer into usually 3 to 5 DSTs. It maximizes what I get for the properties, and provides the same or more net income. Using multiple DST give me comfort that if one goes bad, the rest should carry me through.

Down side to the DST is when they close it in a few years. Its either a rinse, repeat or take the 721 UPRIET option. Since the basis in each DST is much less than the original property I can also decide to take the tax hit (on the much smaller piece).