Newbies! Here's How to Account for All Costs Of a Flip

You’ve found a great deal, you feel it’s going to work, but how you go about figuring out the potential net profits on a flip? You simply take your purchase price, add your rehab budget, and subtract those two inputs from your selling price, right? Follow that simple formula and you’ll be left saying where “where did all that profit go?”

There are plenty of posts/articles providing general rules, but there is not a lot of detailed information on how to accurately account for these “other costs” in a flip. Accounting for these costs was was initially a hindrance for me, so I’d like to share a detailed breakdown of how I now account for all costs to help anyone who is currently in that position.

Below is a breakdown of my analysis after the property passed my original sniff test.

***I am more than happy to share this spreadsheet with anyone who requests it, but I encourage you to understand the logic of the spreadsheet as my assumptions may not be relevant to your market/strategy..***

SET COSTS

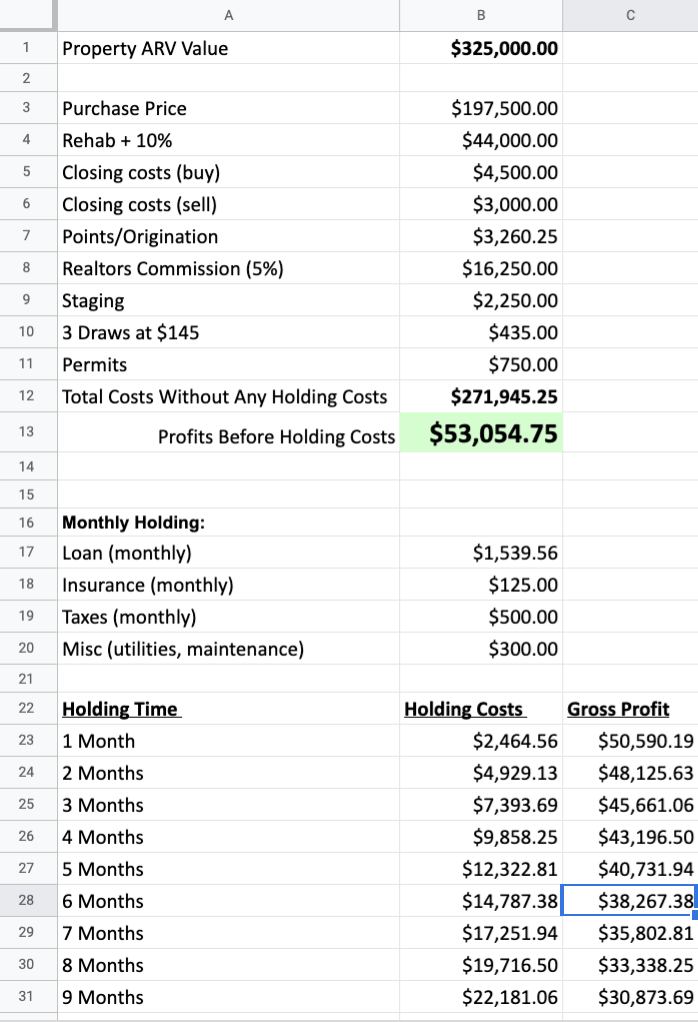

Let’s start with some easy inputs that before the inclusion of holding costs :

Property ARV (B1). Always take the conservative estimate as your data point. If the expected ARV is a range between 150-160k, use 150k. You can’t do calculations with wishful thinking in mind.

In my example our ARV is 325-335k so I input 325k

Rehab Costs (B3). I take my rehab costs and add a 10% contingency. Even if my contractor is usually dead-on, things happen. We all know things come up when doing construction and these risk don’t cease to exist just because you ignore them in your calculations.

In my example, rehab was 40k which I marked-up to 44k.

Closing Costs (B5 and B6). I don’t want to prescribe exact numbers to use, as it varies by area and loan size, but rather ensure you are accounting for these. Talk to investors in your area to get a better feel for this. In IL I’m going to be paying for title insurance, attorney fees, city transfer tax, county transfer tax...etc. In addition, I pay lender fees on the front end, application fee, appraisal costs, servicing fee...etc.

My numbers are based off of past closings. Note that I keep origination separate (next cell) so I can have it automatically adjust with the loan size

Points/Origination (B7). If you’re using a hard money loan, you probably know what you’ll pay in points. I’m currently at 1.5 points so I set up that cell to automatically calculate the origination. My lender gives me 90% of purchase and 90% of rehab so I use the following calculation to arrive at the appropriate points: =(B3+B4)*0.9*0.015.

This formula takes 90% of rehab+purchase and multiplies by 1.5%. You can adjust as needed. Note that I sometimes you private money that does not require me to pay points, but I advise to always account for it in the numbers. Always overshoot.

Realtors’ Commissions (B8). Real basic, there is no fee on the acquisition but you need to account for both realtors when selling the finished product. 5-6% is standard, 6% being a baseline, and anything lower usually negotiated for doing repeat business. Cell B8 simply takes the ARV number and multiplies it by 5%: =B1*0.05

Staging (B9). This is market specific, but my opinion is that if you are in a nicer area, this makes all the difference in the world and is worth every penny. Not saying it’s right/wrong for you, just articulating that you need to put 2-3k aside if you plan to have the property professionally staged.

Draws (B10). If you have a hard money lender, they will have a third-party inspect the property every time you request a draw to ensure the work is actually complete. We tend to do 2-3 draws a project.

Permits (B11). Get a general understanding of permits in your area. Other investors can tell you typical costs and you will then be able to estimate which permit(s) you’ll need based on your scope of work. Note that some larger projects that require architectural drawings can come with a five-figure expense.

I’ve now accounted for all my costs not affected by the length of my holding period. Cell B12 adds up my fixed costs (=SUM(B3:B11)) and Cell B13 subtracts that number from my ARV (=B1-B12). So if you had one magical day where you closed on the property, performed the rehab and sold the property all within 24 hrs, this number would be your profits :).

HOLDING COSTS

Monthly Loan (B17). This will vary, but I always assume I’m financing 90% of the deal. I take the purchase price and rehab budget from the set cost, multiply by .90 (90% LTV) and then multiply by the rate (8.5%) and divide by 12. That formula can be expressed as: =0.9*(B3+B4)*0.085/12. Set the formula once so you never have to do the calculation again.

Insurance (B18). 12 month insurance policy divided by 12.

Unlike your personal home or a rental, you’ll most likely have a policy that includes a line item for the Construction Builders Risk Renovation, which covers the construction amount. Note that from a cashflow perspective, your lender may require you to pay the 12 months upfront, but you will be refunded the difference when you sell (If you only have the policy open for 6 months, you’ll be refunded the other 6 months after your sale of the property).

Taxes (B19). Like the insurance take the annual taxes and divide by 12.

So you understand how taxes can your cashflow/money out of pocket: if you are 3 months into a tax cycle when you buy the property, you’ll receive that 3 month proration from the original seller. Let’s say you turn around and sell 4 months after that, the new buyer will receive a 7 month proration (4 months you owe plus the original 3 credited to you). It’s also important to know when taxes are due so you can make the appropriate payments.

Utilities B20. Get a baseline idea of what water, electric and heat will run you and also include items like landscaping and snow removal if necessary.

PUT IT ALL TOGETHER

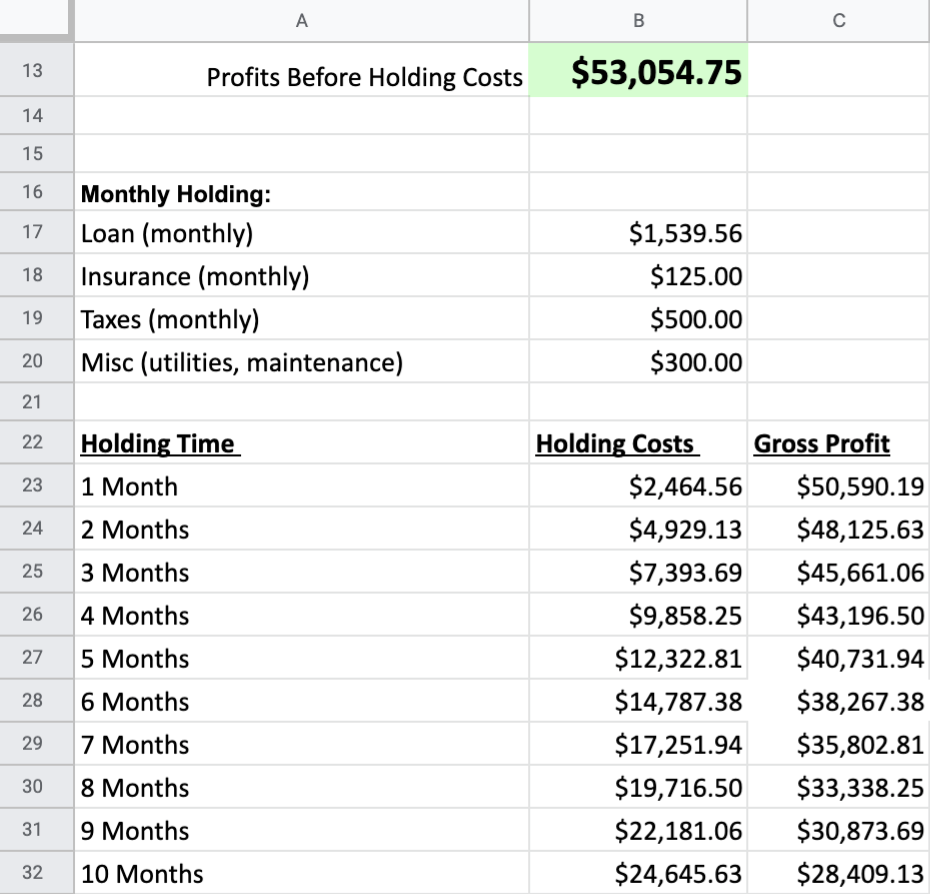

Now that you have the rough monthly costs, you create a simple chart to account for these costs during the length of your hold. This can be seen in cells A22-C32:

A Column: For Cells A22-A32 just write the same content you see above

B Column: For Cell B23 you are adding up the holding costs in B17-B20: =SUM(B17:B20). Cell B24 is then B23*2 as it will be 2 months of holding costs. Cell B25 is =B23*3, Cell B24 is =B23*4 and so on for Column B.

C Column: In this Column you are subtracting the holding costs from B13, which as a reminder is the profit number before we incorporate holding costs. Cell C23 is =B13-B23. Cell C24 is =B13-B24, Cell C25 is =B13-B25 and so on.

Now all costs are accounted for (well, we have not quantified emotional costs :)) and you can see where you land before paying capital gains. Putting it all together it looks like this:

As you can see, a 6 month hold from day of purchase to date of sale, will net north of 38k. When estimating your holding costs, remember it’s not just your rehab period, but time on the market and then time under contract until you actually close. Also, this 38k does not account for the short-term capital gains tax you will pay.

Feel free to create one that fits your needs, but I wanted to provide a baseline to help newbies understand the true cost of a flip.

Anything I missed? Questions? Does anyone have a similar method? Let me know, more than happy to chat!

Comments (3)

Right, and that's the best part! I never enjoy just taking someone elses work and copying it. I love the challenge of implementing this in my own way and tailoring towards BRRRR's. The foundation is still there which will help me a lot.

David Ross II, over 5 years ago

Wow this is great! I'm 21 and just landed a six-figure job. I'm looking to get started with the BRRRR strategy to build equity fast. I'm definitely going to implement this spreadsheet when I analyze deals! I may even go more conservative and take an additional 5% out of the gross profits. Thanks for sharing!

David Ross II, over 5 years ago

Hi @David Ross II - congrats on getting started. Note that you can borrow concepts from this to calculate your hold during a BRRRR, but this is geared towards flips.

For example, your BRRRR won't have realtor commissions, will have to account for long-term financing...etc. Most importantly, this does not account for any calculations of your long-term buy-n-hold period after you secure a tenant which is probably a critical piece of your BRRRR calculation.

Tom Shallcross, over 5 years ago