$699,900

Investment Summary

- Monthly Cash Flow

- -$1,755

- Cap Rate

- 2.7%

- Cash-on-Cash Return

- -13.1%

- Debt Coverage Ratio

- 0.47

- Internal Rate of Return (5 years)

- -8.7%

Cash Flow

Net Operating Income (NOI) minus mortgage payments.

Calculation:

NOI - Mortgage Payments

Cap Rate (Market Value)

Capitalization Rate is a rate of return that compares the yearly Net Operating Income (NOI) to the market value.

Calculation:

NOI / Market Value

Cash-on-Cash Return (CoC)

Annual Cash Flow / Cash Invested

Calculation:

Annual cash flow divided by initial cash invested.

Debt Coverage Ratio (DCR)

Net Operating Income (NOI) divided by total debt payments.

Calculation:

NOI / Total Debt Payments

Internal Rate of Return (IRR)

A metric for assessing profitability over time. IRR is the discount rate at which the net present value (NPV) of all future cash flows (positive and negative) from an investment equals zero — including both periodic cash flow (such as rent) and a projected sale at the end of the holding period. It represents the expected annualized return, accounting for income, expenses, and the recovery of capital through a future sale.

Property Description

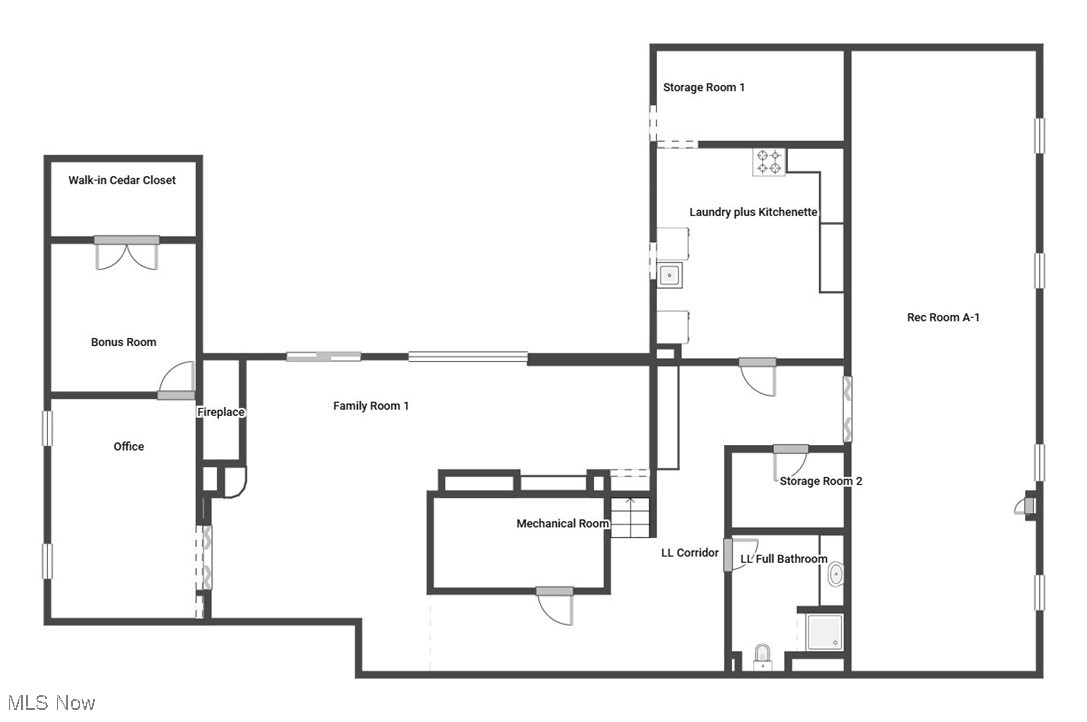

Welcome to 8001 Robin Lane—an exceptional 4-bed, 4.5-bath home nestled on 1.31 acres in Brecksville. Offering 3,538 sq ft above grade plus 3,231 sq ft of finished walk-out lower-level space, this property blends modern luxury with natural serenity. The remodeled kitchen (2018) features quartz countertops, custom cabinetry with built-in step stools, a Wolf gas range, stainless steel appliances, and a widened picture window above a one-touch faucet. The sunroom opens to a stamped concrete patio with a louvered Pergola X roof and brick/sandstone steps—perfect for entertaining or relaxing in the park-like fenced backyard with 15+ mature trees (canopy) & a stone border. The primary suite includes a spa-like bath (2019) with soaking tub, zero-entry shower, floating double vanity with under-mount lighting, and a custom California Closets walk-in. Hardwood floors, four fireplaces, Pella windows with internal blinds, and abundant storage add comfort throughout. The expansive lower level, which could be used for an in-law or teen suite, includes a massive rec room, office, bonus room with a huge cedar closet, full bath, 2 storage rooms, and a secondary kitchen/laundry space with gas range, pantry, and fridge area—plus access to the lower patio from the family room. The attached 3-car garage includes a foldable ramp for wheelchair accessibility. NEW major upgrades include a 7-zone boiler (December 2023), central A/C (2024), hot water tank (2024), and half bath toilet (2025). Additional features: glass block windows, newer ceiling fans, illuminated closets, a brick outbuilding with electricity, and a storage shed. Ideally located on a very quiet street located just minutes from downtown Brecksville, Valor Acres, Metroparks, and the Cuyahoga Valley National Park—this move-in-ready home offers luxury, comfort, and a truly special setting. Don’t miss the interactive 3D virtual tour which includes the interior & the yard. Don't delay... schedule your tour today!

Build Your Team

Quickly find investor-friendly professionals who can help you succeed in real estate investing at any stage of the investing journey.

Agents

Match with investor-friendly agents who can help you find, analyze, and close your next deal

Lenders

Get the best funding…find investor-friendly lenders who specialize in your deal strategy

Property Managers

Transition to passive investing. Find a trusted property management partnership that lasts.

Tax Pros & Accountants

Taxes and financial reporting made easy—find experts to create tax savings strategies, file taxes, and more

Location

Property Details

Parking

- Description: Attached, DirectAccess, Garage, GarageDoorOpener

- Details: Attached, Driveway, Garage, Garage Door Opener, Inside Entrance, Outside, Garage Faces Side

- Garage Spaces: 3

- Spaces Total: 0

Bedroom Information

- # of Bedrooms: 4

Bathroom Information

- # of Baths (Full): 4

- # of Baths (Partial): 1

- # of Baths (Total): 5.0

Interior Features

- # of Rooms: 8

- # of Stories: 1

- Basement: Yes

- Basement Description: Exterior Entry, Full, Finished, Walk-Out Access

- Fireplace: Yes

Exterior Features

- Exterior Walls Materials: Brick

- Roof Type: Hip

- Roof Material: Asphalt, Fiberglass

- Pool Community: Yes

Land Information

- Land Use: Residential

- Land Use Subtype: Single Family Residential

Lot Information

- Parcel ID: 60203064

- Lot Size: 0 sqft

Property Information

- Property Type: Single Family Residence

- Style: Ranch

- Year Built: 1970

Tax Information

- Annual Tax: $10,293

Utilities

- Water & Sewer: Public

- Heating: Hot Water, Steam, Zoned

- Cooling: Ceiling Fan(s), Central Air

Location

- County: Cuyahoga

Listing Details

Investment Summary

- Monthly Cash Flow

- -$1,755

- Cap Rate

- 2.7%

- Cash-on-Cash Return

- -13.1%

- Debt Coverage Ratio

- 0.47

- Internal Rate of Return (5 years)

- -8.7%

Cash Flow

Net Operating Income (NOI) minus mortgage payments.

Calculation:

NOI - Mortgage Payments

Cap Rate (Market Value)

Capitalization Rate is a rate of return that compares the yearly Net Operating Income (NOI) to the market value.

Calculation:

NOI / Market Value

Cash-on-Cash Return (CoC)

Annual Cash Flow / Cash Invested

Calculation:

Annual cash flow divided by initial cash invested.

Debt Coverage Ratio (DCR)

Net Operating Income (NOI) divided by total debt payments.

Calculation:

NOI / Total Debt Payments

Internal Rate of Return (IRR)

A metric for assessing profitability over time. IRR is the discount rate at which the net present value (NPV) of all future cash flows (positive and negative) from an investment equals zero — including both periodic cash flow (such as rent) and a projected sale at the end of the holding period. It represents the expected annualized return, accounting for income, expenses, and the recovery of capital through a future sale.

Purchase Details

Purchase PriceThe price paid for the property. Purchase price:

| $699,900 |

|---|---|

Amount FinancedThe amount of the purchase financed through a loan. Amount financed:

| -$559,920 |

Down paymentThe initial payment made towards the purchase. Down payment:

| $139,980 |

Closing CostsFees and expenses associated with purchasing a property, typically ranging from 2% to 5% of the home’s purchase price, paid at the end of a home purchase to cover services like lending, title transfer, and taxes. Closing costs:

| $20,997 |

Rehab CostsCosts incurred to repair or improve the property, including: roof, flooring, exterior siding, kitchen, exterior paint, bathrooms, etc. Rehab costs:

| $0 |

Initial Cash InvestedThe total initial cash invested in the property. Calculation:Down payment + Buying costs + Rehab costs Initial cash invested:

| $160,977 |

Square Feet (SQFT)The total square footage of the property. Square feet:

| 6,769 |

Cost Per Square FootCost per square foot of the property. Calculation:Purchase Price / Square Feet Cost per square foot:

| $103 |

Monthly Rent Per Square FootMonthly rent divided by the number of square feet. This ratio helps investors compare rental income efficiency across properties, markets, and unit sizes Calculation:Monthly Rent / Square Feet Monthly rent per square foot:

| $0.52 |

Financing Details

Loan AmountThe total sum of money borrowed from a lender to finance a property purchase. Calculation:Purchase Price - Down Payment

Loan amount:

| $559,920 |

|---|---|

Loan to Value Ratio (LTV)Loan amount divided by the market value of the property. Calculation:Loan Amount / Market Value

Loan to value ratio:

| 80.0% |

Loan TypeThe type of loan (e.g., fixed, adjustable).

Loan type:

| Amortizing |

TermThe loan repayment period in years.

Term:

| 30 years |

Interest RateThe percentage a lender charges on the borrowed amount of a loan, determining the cost of borrowing money.

Interest rate:

| 5.875% |

Principal & Interest (PI)The principal is the portion of the loan payment that reduces the loan balance. The interest is the lender's charge for borrowing money. Calculation:(P * r * (1 + r) ** n) / ((1 + r) ** n - 1) Where:

P = Loan amount (principal)

Principal & interest:

| $3,312 |

Property TaxesAnnual taxes levied by local governments on real estate properties. These taxes fund public services like schools, roads, and emergency services.

Property tax:

| $858 |

InsuranceThe costs for insurance coverage to protect against financial losses due to risks like fire, natural disasters, theft, liability, or tenant-related damages. Calculation:Assumes 7% of gross rental income, unless insurance rates are specified.

Insurance:

| $245 |

Private Mortgage Insurance (PMI)A fee that borrowers pay when they take out a conventional loan with a loan-to-value (LTV) ratio above 80%.

Private mortgage insurance (PMI):

| $0 |

Monthly PaymentThe fixed amount a borrower pays each month to repay a loan. It typically includes principal and interest (P&I) and may also cover property taxes, insurance, HOA fees, and PMI if escrowed. Monthly payment:

| $4,415 |

Operating Income

| % Rent | Monthly | Yearly | |

|---|---|---|---|

Gross RentThe total rental income received from tenants before deducting any expenses. Includes base rent, late fees, pet fees, parking fees, and other recurring charges.

Gross rent:

| $3,500 | $42,000 | |

Vacancy LossExpected loss of rent due to vacancies.

Vacancy loss:

(6%)

| 6% | -$210 | -$2,520 |

Operating IncomeGross rental income minus vacancy loss. Calculation:Gross rent - Vacancy loss

Operating income:

| $3,290 | $39,480 |

Operating Expenses

| % Rent | Monthly | Yearly | |

|---|---|---|---|

Property TaxesAnnual taxes levied by local governments on real estate properties. These taxes fund public services like schools, roads, and emergency services. | 25% | -$858 | -$10,294 |

InsuranceThe costs for insurance coverage to protect against financial losses due to risks like fire, natural disasters, theft, liability, or tenant-related damages. Calculation:Assumes 7% of gross rental income, unless insurance rates are specified. | 7% | -$245 | -$2,940 |

Property ManagementThe costs associated with hiring a property manager to handle the day-to-day operations of a rental property. Includes management fees, leasing fes, eviction fees, etc. Calculation:Assumes 8% of gross rental income. | 8% | -$280 | -$3,360 |

Repairs & MaintenanceOngoing costs for routine upkeep and minor fixes needed to keep a property in good working condition. Calculation:Assumes 5% of gross rental income. Varies by property age and condition. | 5% | -$175 | -$2,100 |

Capital ExpensesLarge, infrequent costs for major improvements or replacements, like a new roof, HVAC system, or appliances. Calculation:Assumes 5% of gross rental income. Varies by property age. | 5% | -$175 | -$2,100 |

HOA FeesRegular dues paid to a Homeowners Association for community maintenance, amenities, and management. Similar fees include: Condo Association Fees, Co-op Maintenance Fees, etc. | n/a | n/a | n/a |

Operating ExpensesRecurring costs required to maintain and manage a rental property, including property taxes, insurance, maintenance, repairs, utilities (if paid by the owner), property management fees, and other day-to-day expenses. Calculation:Insurance + Property Taxes + Property Management + Repairs & Maintenance + Capital Expenditures + HOA Fees | 50% | -$1,733 | -$20,794 |

Cash Flow

| Monthly | Yearly | |

|---|---|---|

Net Operating Income (NOI)The income generated from a property after deducting all operating expenses but before deducting mortgage payments, taxes, and capital expenditures. Calculation:Gross Operating Income - Operating Expenses

Net operating income:

| $1,557 | $18,684 |

Mortgage PaymentThe fixed amount a borrower pays each month to repay a loan. It typically includes principal and interest (P&I) and may also cover property taxes, insurance, HOA fees, and PMI if escrowed. | -$3,312 | -$39,744 |

Cash FlowNet Operating Income (NOI) minus mortgage payments. Calculation:NOI - Mortgage Payments | -$1,755 | -$21,060 |