Don't Make This Costly Mistake On An Over-funded Policy

Don’t Make Lump Sum Premium Payments!

Introduction

I don’t mean to sound hyperbolic, but this is the number one mistake I see people make when they pull the trigger on an over-funded policy. As much as you’d like to get your money into the policy and working as rapidly as possible, large Lump Sum premiums destroy the efficiency of your policy. That is not the way to get your money into a policy efficiently.

The bottom line is this: a large, up-front premium drives up the death benefit and internal costs of a policy. If your goal is maximum cash value accumulation, this is counter-productive. Unfortunately, I usually hear about it after the fact when it's too late to fix it. I generally find this when I’m reviewing an in-force policy from someone who has asked me to take a look at their policy to make sure that it was designed right. Once the policy has been issued, and the free look period has elapsed, it is too late to make any changes.

The only winner will be the Life Insurance agent who sold you the policy. The agent’s compensation is based on the Death Benefit of the policy. And the large up-front premium proportionately increased the death benefit of the policy. And unfortunately, that large premium also increased all of the costs of the policy.

Agent’s who do this KNOWING that the client’s goal is cash value accumulation are either ignorant of how life insurance works under the hood or are unethical and simply accommodate your wishes without informing you of the consequences. I have to talk people out of doing this all the time.(1) It is a very common request.

A Little Life Insurance 101

Why is a lump sum premium a bad idea? Simple: the death benefit is a function of the first year premium. And in a policy that is designed for maximum cash value, we are solving for the smallest death benefit that will still meet the definition of Life Insurance based on the premium paid--the first year.

Life Insurance is very scalable. In other words, If you double the premium, you’ll also double the death benefit, cash value, and costs. If a premium of $1,000 per month results in a policy with a $500,000 death benefit, you can expect that a policy with a $2,000 per month premium will have a $1,000,000 death benefit.

The internal costs are also scalable. The fees taken from the $2,000 per month policy will be roughly 2 times the fees of the policy with a $1,000 premium.(2)

There are generally four types of expenses in a policy.(3)

Premium Charges - These are charges that are assessed on every dollar of Premium that is paid into a policy. It is a percentage of the premium. They are typically collected in order to pay the premium tax that insurance companies must pay to the state governments.

Variable Policy Charges - These charges are related to the death benefit. The higher the death benefit, the higher the charge. These are typically collected during the surrender charge period of the policy. If a policy has a 10-year Surrender charge period, the charges are collected every year for 10 years. If the policy has a 15-year surrender charge period, the charges are collected every year for 15 years. This charge remains constant even if the death benefit is reduced during the surrender charge period.

Fixed Policy Charges - This is typically a very small fixed charge assessed on every policy large or small. It does not vary based on the amount of death benefit.

Cost of Insurance - This charge covers the gap between the death benefit and the cash value: The Net Amount at Risk. It is used to pay the expected claims.(4)

Analysis

It is the Variable Policy Charge and the Cost of Insurance that will eat up the cash value in a policy that is funded with a large lump sum premium paid in the first year.

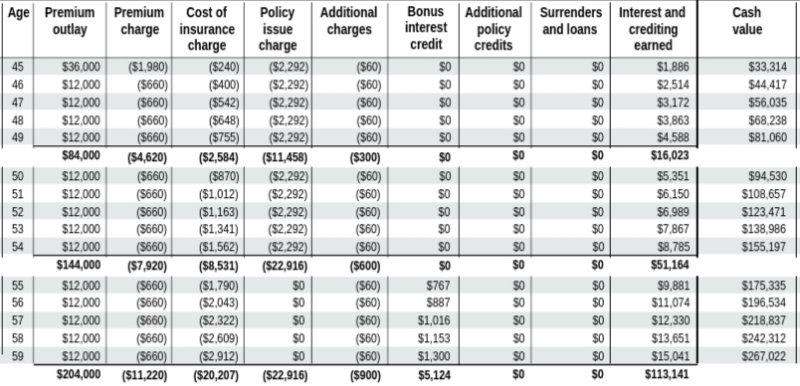

This is a breakdown of the costs in a properly-designed, maximum cash value policy with a $12,000 annual premium…(5)

This illustration extract shows the premium, charges, and cash value for the first 15 years of the policy with the client paying $12,000 per year of annual premium. If you do the math, the premium charge works out to be 5.5% of the premium and is assessed every year that a premium is paid. The Policy Issue Charge is the Variable charge tied to the amount of death benefit. As you can see, this charge is $854/year and is assessed for only the first 10 years of the policy.

The death benefit on this policy is not shown in the table. It is $291,080 at issue and is increasing i.e. the total death benefit is the amount of cash value plus the face amount of the policy at issue. The death benefit will switch to level and be reduced to minimum Non-MEC after 20 years when the client reaches retirement age. Making this change minimizes the policy expenses when the client is done paying premium into the policy. The idea that a policy will lapse due to rising cost of insurance is a myth. The cost of insurance will only be about 0.25% of the cash value because the net amount at risk is so small.

The “Cost of Insurance” is the cost of that fixed increment of $291,080 of death benefit protection. You can see that the cost increases each year as the insured ages. The future reduction is not shown here.

The column labeled “additional charges” is the fixed policy charge of $60 per year.

Note the ending cash value balance of $257,429 at the end of the 15th year: $257,429

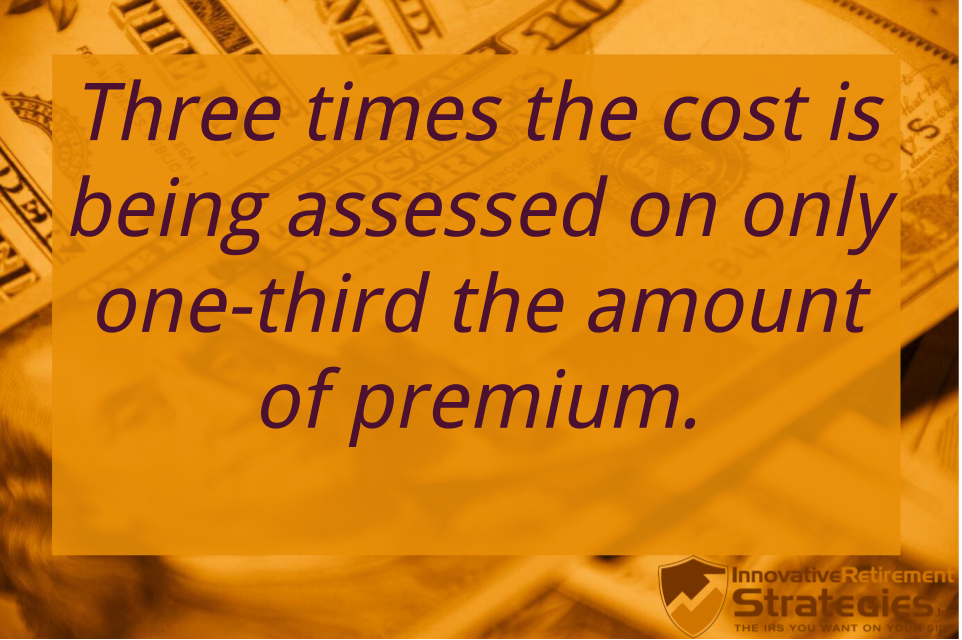

Now let’s say that this client has $24,000 sitting in the bank and they’d like to add that money to the policy too. The agent happily re-runs the illustration showing the additional premium of $24,000 in the first year of the policy. The client thinks they are building up their cash value bank. The agent happily runs the illustration because they are looking at a commission that is 3 times higher now.

What?

The Agent’s commission will be 3 times higher. Here is the illustration showing the charges for the new policy design…

The death benefit of this policy design is $846,198. That is nearly 3 times wh

at the death benefit was in the previous illustration ($291,080). As a result of the change in death benefit, the agent gets a commission that is nearly 3 times as large. But the client now has a policy with internal costs that are 3 times higher yet the premium after the first year reverts back to the original $12,000 per year!

The Premium Charge is scalable. Luckily it goes down with the reduction in premium after the first year. The Fixed Policy Charge remains unchanged as well. But unfortunately, both the Policy Issue Charge and the Cost of Insurance Charge have nearly tripled while the premium has dropped to only $12,000 per year. Three times the cost is being assessed on ⅓ the amount of premium!

The higher charges consume more of the premium dollars that go into the policy leaving less to go toward the cash value. Look at the ending cash value. It is only $9,593 higher than in the previous illustration.

Let that sink in.

A lump sum of $24,000, paid in the first year of the policy, resulted in only $9,543 more cash value at the end of the 15th year. The client lost money.

And unfortunately I see this ALL THE TIME. The clients have no idea. They don’t understand the cost structure of the policy. More premium should mean more cash value, right? The problem is agents who also don’t understand the cost structure of the policy. Or worse, they understand the cost structure of the policy and still do it.

So what should this client do?

The additional premium should be spread out over a few years. Since the first year premium is the driver for the death benefit, we want to keep the first year premium to a minimum. I have found that the sweet spot is 5 years. A shorter funding period leaves too high of a death benefit and costs that consume the cash. Any longer and you are taking too long to put your money to work. The premium should be spread out over 5 years with a reduction in the death benefit to help drive out costs after the premium changes back to the lower amount.

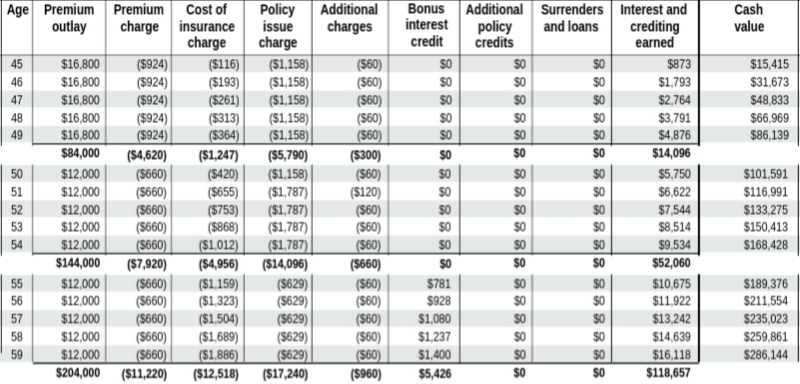

The following illustration shows an additional $4,800 tacked onto the original $12,000 per year for the first five years...

This policy design has a $408,494 death benefit at issue. This is substantially lower than in the previous illustration. In addition, I am reducing the death benefit to the minimum Non-MEC limit at the end of the 6th policy year and again after 20 years when the client will be 65 years old and doesn’t want to continue paying premiums.

The reduction in the death benefit after year 6 does not help with the Policy Issue Charge. It is what it is. But the Cost of Insurance charge will be reduced because the death benefit is lower. The change is barely noticeable when you look closely at the table.

But, look at the cash value at the end of the 15th year now: $286,144. This is a significant improvement over both previous illustrations.

But what does the client do with the remaining cash not being paid into the policy?

Anything they want. They can keep it where it is or place it into a Premium Deposit account managed by the Insurance Company. The insurance companies will pay interest on the money held to pay future premiums. It’s not a super-high interest rate, but it is still considerably higher than bank CDs and money market rates.

Conclusion

I hope that the analysis and the explanation that I’ve provided in this paper will help save people from making a very costly mistake. While the idea of adding a lump sum premium to a policy would seem to make sense, the reality is that the only one making any more money is the agent writing the policy.

Any additional money should be spread out over 5 years with policy changes to reduce the death benefit and keep the policy’s internal costs down.

Footnotes:

(1) It is important to point out that the primary reason to buy life insurance should be the death benefit protection. Cash accumulation is a side-benefit but should be a secondary consideration.

(2) I state “Roughly” because there are some fixed policy charges that are assessed on every policy regardless of the amount of premium. The smaller the premium, the larger these fees are as a percentage of the premium paid.

(3) The terms used are terms related specifically to Universal Life policies. But for all practical purposes, a Universal Life policy is nothing but an unbundled Whole Life. They are mechanically the same under the hood. A UL simply makes explicit that which is buried in the black box of a Whole Life.

(4) If you need a primer on the mechanics of a life insurance policy, download and read the Life Insurance 101 paper from http://innovativeretirementstrategies.com/life-insurance-101/

(5) Assumes a Universal Life 6% interest crediting rate and NO EARLY CASH VALUE RIDER. I’m using a UL because the costs are made explicit on the illustration. Whole Life costs would be nearly identical except for company to company differences. WL illustrations don’t show these costs.

Comments