The All Cash Plan - Path #1 to Free & Clear Real Estate

On your path to a destination of Financial Independence, I think a simple but powerful goal of free & clear (no debt) real estate is a good idea.

Your free & clear goal might be, for example, to own 10 houses that together rent for $12,000 per month ($1,200 per house) and net $7,000 per month after expenses. In other words $84,000 per year.

Once you have set your personal free & clear goal, the next natural question is how do you get there?

In this series I will give you three general paths that may help you climb the free & clear mountain.

1. The All Cash Plan

2. The Snowball Plan

3. The “Buy 3-Sell 2” Plan

In this article I’ll explain plan #1.

The All Cash Plan

I am going to start with the most conservative plan. This plan is conservative because it involves no debt.

I am not afraid to use debt, as long as it fits my rules. I see it as a simple risk-reward trade-off. In some situations the rewards of debt clearly out weigh the risks.

But, I have also found that simple, conservative plans executed consistently and with enthusiasm will often trump more debt-filled, “intelligent” plans. I’ve also noticed that most of the rich (and happy) people I know like to keep it simple and have little debt.

So my version of a simple, conservative plan basically works like this:

1. Save enough cash to buy one income property

2. Save 100% of the rental income plus extra savings from a job.

3. Buy another income property.

4. Repeat until your goal for free & clear properties is met.

I love the story of Vince Lombardi, an NFL Hall of Fame coach. It was said that Coach Lombardi ran only two simple plays on offense - a sweep left and a sweep right.

His players would practice these two plays over, and Over, and OVER! They became sick of the endless and boring repetition.

But, you can probably guess what happened. His players executed these simple plays to perfection and won championships.

So this All Cash Plan is the equivalent of Lombardi’s sweep left and sweep right for real estate investing.

An All Cash Plan Example

To shed light on how this plan works, let me show you some real numbers using lower-priced duplexes.

In my example, first you will need to build up savings of $60,000. If you earn a lot, this could happen very fast. If you don’t earn a lot, this could take years.

Either way you will need to get good at saving lots of money.

Next you buy a duplex.

Because you own this duplex free & clear, all $7,200 of the net rent goes into your bank account. Importantly, I also assume that you can save $5,000 per year from your job or other source.

So each year you’ll accumulate $12,200 in your bank account (before taxes, although depreciation will likely shelter part of the income from taxes).

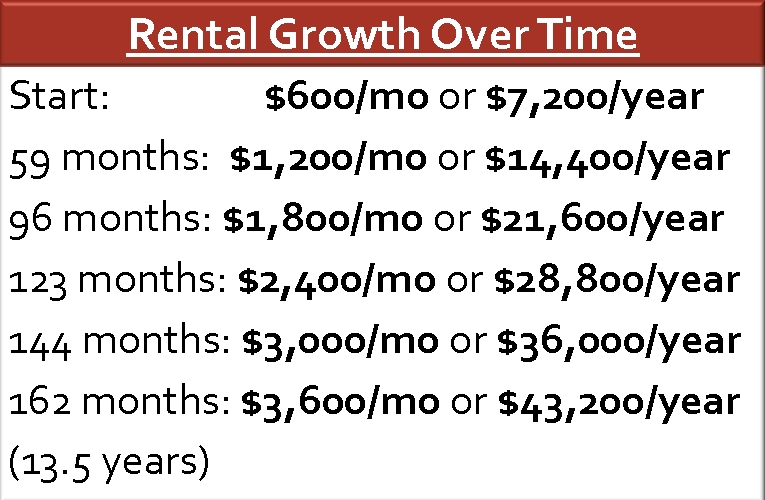

After 4 years, 11 months you’ll have another $60,000 saved. So you buy duplex #2.

After another 3 years, 1 month you’ll have another $60,000 saved. So you buy duplex #3.

This pattern keeps going on and on, and the money accumulates faster and faster over time.

If you want to see the big picture, in just 13.5 years you would own 6 duplexes (12 units) that produce over $43,000 per year in net rent, free and clear of any debt!

This chart shows how your income stream grows over time:

How many plans do you know that turn a $60,000 initial investment + $5,000 per year savings into a $43,000 per year income stream for life?

I know of very few.

And the other ones that do claim to work depend on a lot of factors outside of your control. This plan depends primarily upon three things:

1. Your ability to save money.

2. Your ability to purchase good properties

3. You ability to manage a small number of properties (or to hire a manager).

I like it when my financial destiny depends upon my efforts and not upon chance or the whims of others.

Objections

I welcome your comments, counter-arguments, or questions. But, there are a couple of primary objections that I have heard in the past when discussing this particular plan.

“I can’t find these great deals in my area”

You might object that these deals have incredible cash flow numbers and that you’ll never be able to find deals like that.

I agree these numbers are very good, but in many markets if you are persistent and if you build systems and networks to find deals, these types of deals can be found consistently.

If you are in one of the high-priced markets where numbers like these absolutely won’t work, you can go buy in other markets or you can try one of the other plans I’ll suggest in subsequent articles.

But, also remember that even if the numbers aren’t this good, the principle still works. The time-table just might take a little longer.

“I don’t have enough cash. It will take too long to get started.”

My first response is patience. If you don’t have enough cash yet, you have an earnings and savings problem, not an investing problem.

Learn to win the game of earning money and saving money first, then start focusing on investing in real estate. Get a side job, get a raise, cut your personal overhead, sell all your junk, sell your fancy car, sell your over-sized residence.

Get the picture?

Also you might consider thinking outside of the box.

Do you have that much money in an IRA or 401k? These types of accounts can be self-directed to buy real estate. I personally have worked a variation of this all cash plan in my own self-directed IRA with much success.

You may also be able to partner with someone else. If you have $30,000 and someone else has $30,000, together you can buy one property.

So if you like your real estate wealth building steady and super-safe, this might be a path up the mountain for you. There will certainly be challenges, but as you can see, the payoff in the end is worth the effort.

In my next article I’ll share Free and Clear Path #2 - The Snowball Plan.

Enthusiastically,

Comments (15)

i realize this is an old post, but here goes. i like all these strategies but they don't seem to take into account the 50% rule. Don't you have to set aside about half of your rental income for repairs and maintenance and taxes and ins. etc? And then save all the extra cashflow for payoff? or did i miss something. I'm currently in the learning stage and maybe be a little overloaded with information from listening to bigger pockets podcasts all day!

Laura Srocki, over 7 years ago

Hey Laura, it's a good question. But in my example above I did account for about 50% expenses. The gross rent was $1,200/mo and the net rent was $600/mo. So, you'd only be saving the net rent.

It's easy to get overwhelmed with info! But you're asking the right questions:)

Chad Carson, almost 7 years ago

Very simple and nice strategy! I fully support all cash investment principle. But it requires some sacrifices. we are managing to save up to 58-61% of our household salary income in order to invest in RE. now we have one condo renting out, purchased second one (new condo construction phase), after we rent it out, we'll go for the third one. And repeat this principle again and again.

Sanzhar Zikirov, about 9 years ago

Well done Sanzhar!! Keep rolling!

Chad Carson, almost 7 years ago

I love this post! I am a lot like you, meaning I would use a small amount of debt in the right deal. My wife does not like the idea. I think sometimes people are to quick to say no you need to leverage in order to get big and be succesfull. I guess it all boils down to your goals.

Michael Brown, about 10 years ago

thanks Michael! You are right - so.e people would give you the crazy look if you talked about buying with no leverage. But I tried

Chad Carson, about 10 years ago

Chad Carson, about 10 years ago

The partnership strategy resonates quite well with me and can cut the time for the investment period while building cash flow free and clear. Great post and responses.

Cheers!

Kingsley Siribour, about 11 years ago

Chad Carson, about 11 years ago

I love the idea of owning my rentals free and clear and generating cash flow. I take a slightly different strategy. I do have some debt, but I also purchase properties CHEAP -- as in < $40,000. This way they can get paid off very quickly even with mortgages.

Dawn Anastasi, about 11 years ago

Dawn, I have no problem taking on more risk with debt as long as I is done safely and with full awareness. So your plan sounds smart.

Personally, on lower priced properties as I have described in this article or like you described at <40k, I would ONLY take on debt that pays off quickly. I want it free and clear before I get too burned out:)

Chad Carson, about 11 years ago

I'm looking at all cash strategy to build my passive income. Can't wait for your next article on plan 2 and 3. Thanks for sharing

Martin Yung, about 11 years ago

thanks @Martin Yung ! Next article coming soon.

Chad Carson, about 11 years ago

Wendy, I like both of your reasons for paying cash. Your reason #2, taking it slow and easy so as not to make too many mistakes, is VERY wise in my opinion. As long as you're moving forward, you'll be compounding cash and compounding knowledge, which will grow faster and faster over time.

I have done some all cash investing (with my IRA) and debt investing (which I'll explain in my next 2 articles). So I hope my thoughts and strategies are helpful.

Thanks for commenting!

Chad Carson, about 11 years ago

Thanks for this. I thought I was the only one who would think cash was a good strategy. I was lucky to make a lump sum of cash buying a condo, living in it and fixing it up over 3 years. At the end of three years, it was almost turnkey and a buyer snapped it up. I used this profit to buy my first rental unit for cash and currently saving up to buy my second by the end of this year. Its not sexy but it has two advantages: (1) I sleep well at night. (2) because I'm not in a rush, I have time to do a lot of learning and researching and hopefully I won't make too many mistakes along the way. By property #3, I'm thinking of financing a % of the home price that I don't tie up all my own cash and still get some cash flow. So very interested to read your next articles to get more info.

Account Closed, about 11 years ago