$2,464,000

Investment Summary

- Monthly Cash Flow

- -$10,075

- Cap Rate

- 0.8%

- Cash-on-Cash Return

- -21.3%

- Debt Coverage Ratio

- 0.14

- Internal Rate of Return (5 years)

- -16.6%

Cash Flow

Net Operating Income (NOI) minus mortgage payments.

Calculation:

NOI - Mortgage Payments

Cap Rate (Market Value)

Capitalization Rate is a rate of return that compares the yearly Net Operating Income (NOI) to the market value.

Calculation:

NOI / Market Value

Cash-on-Cash Return (CoC)

Annual Cash Flow / Cash Invested

Calculation:

Annual cash flow divided by initial cash invested.

Debt Coverage Ratio (DCR)

Net Operating Income (NOI) divided by total debt payments.

Calculation:

NOI / Total Debt Payments

Internal Rate of Return (IRR)

A metric for assessing profitability over time. IRR is the discount rate at which the net present value (NPV) of all future cash flows (positive and negative) from an investment equals zero — including both periodic cash flow (such as rent) and a projected sale at the end of the holding period. It represents the expected annualized return, accounting for income, expenses, and the recovery of capital through a future sale.

Property Description

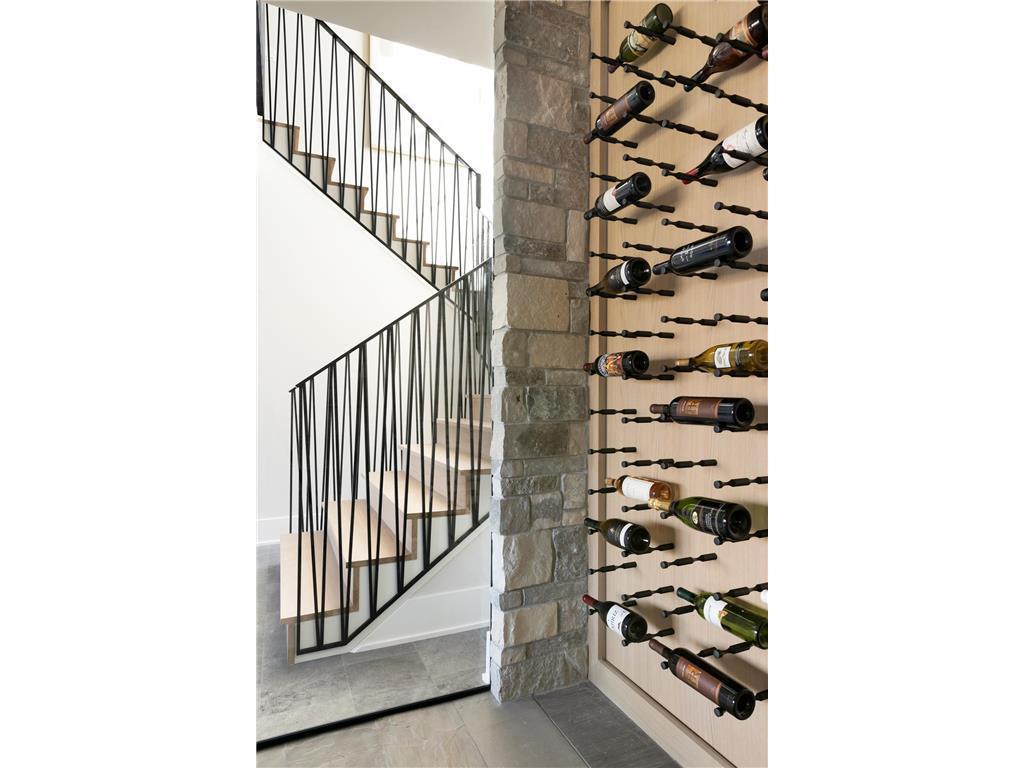

Modern Design. Storied Setting. Exceptional Access. A David Charlez–Designed Residence, built by Swanson Homes. In a secluded Minnetonka neighborhood, cradled by woodland, wetland, and a serene pond, a distinctive design–build opportunity awaits. This expansive 1.33-acre property—enhanced by more than $40,000 in professional design work, secured city approvals, and a CUP/variance for an accessory dwelling unit—includes a complete David Charlez concept plan, envisioned across all three levels to deliver approximately 4,098 finished square feet of modern Midwestern living, with flexibility to personalize selections. Architecture & Builder Pedigree: David Charlez Designs, an award-winning architectural studio, is known for contextual architecture that embraces each site’s topography, views, and natural features. Swanson Homes, a boutique luxury builder with over 50 years of Twin Cities experience, is celebrated for design-forward execution, indoor–outdoor integration, and exceptional client collaboration. Together, they deliver a one-of-a-kind design–build experience marrying vision with craftsmanship. Main Level: Anchored by a dramatic great room with statement fireplace and floor-to-ceiling glass, the main level flows into the chef’s kitchen—complete with 9’ center island, custom cabinetry, and premium appliances. The adjoining dining space opens to a covered deck overlooking the pond. A private guest/in-law suite features its own living area and kitchenette. The mud room, powder bath, and portico entry balance practicality with elegance. A full-length deck—part covered, part open—extends from the great room and connects to the lower-level patio via a sculptural spiral staircase. Upper Level: The owner’s suite is a retreat—spa-inspired bath with dual bathrooms, oversized walk-in closets, and a shared glass shower—opening to a private sky-deck. One additional bedroom shares this level, along with an art loft perfect for creative work, study, or reading. The remaining space, originally envisioned as an open art loft, offers flexible potential as a landing for any purpose. Walkout Lower Level (Finished): Designed for connection and recreation, the lower level offers a spacious family room, wet bar, media zone, fitness area, guest bedroom, and 3/4 bath—all with walkout access to the patio and wooded yard. Design Intent & Finish Direction: Every sightline is intentional—floating staircase, seamless indoor–outdoor transitions, and curated materiality: warm woods, matte black fixtures, and soft stone tones. The result is a home that feels effortless—because it was designed to be. Variance & ADU Approval: Comes with a recorded front yard setback variance and a Conditional Use Permit for a 610 sq ft accessory dwelling unit—approved by the City of Minnetonka and ready to build. The variance allows a site plan that fits the lot’s wooded setting, pond views, and walkout-friendly topography; the ADU enables a self-contained guest house, in-law suite, or studio. The Setting: Privacy and proximity, in rare balance. Minutes to Ridgedale Center, Whole Foods, Trader Joe’s, and future Southwest LRT access—yet worlds away in feel. Downtown Minneapolis is just 10 minutes via I-394. Served by Hopkins Schools and within reach of top private campuses—Breck, Blake, Benilde-St. Margaret’s, Providence Academy, and more. At 1.33 acres, it’s unusually expansive for this close to downtown—offering rare elbow room without sacrificing convenience. Lake Minnetonka Lifestyle: Just to the west, Minnesota’s most celebrated lake calls. Wayzata’s Panoway, dockside dining, the Dakota Rail Trail, and year-round events are within easy reach—while your wooded haven remains a private retreat. Permit-ready, fully customizable, and crafted by one of Minnesota’s most respected architect–builder teams—this is where legacy begins. Interior photos are of a similar Swanson Homes build and are shown for inspiration; final design, features, and finishes may vary.

Build Your Team

Quickly find investor-friendly professionals who can help you succeed in real estate investing at any stage of the investing journey.

Agents

Match with investor-friendly agents who can help you find, analyze, and close your next deal

Lenders

Get the best funding…find investor-friendly lenders who specialize in your deal strategy

Property Managers

Transition to passive investing. Find a trusted property management partnership that lasts.

Tax Pros & Accountants

Taxes and financial reporting made easy—find experts to create tax savings strategies, file taxes, and more

Location

Property Details

Parking

- Description: Attached Garage, Concrete, Garage Door Opener

- Garage Spaces: 2

- Spaces Total: 0

Bedroom Information

- # of Bedrooms: 5

Bathroom Information

- # of Baths (Full): 3

- # of Baths (Partial): 1

- # of Baths (Total): 7.0

Interior Features

- # of Rooms: 14

- # of Stories: 2

- Basement: Yes

Exterior Features

- Exterior Walls Materials: Stucco

- Roof Type: Hip

Land Information

- Land Use: Residential

- Land Use Subtype: Single Family Residential

Lot Information

- Parcel ID: 0211722440036

- Lot Size: 57499 sqft

Property Information

- Property Type: Single Family Residence

- Style: (SF) Single Family

- Year Built: 2026

Tax Information

- Annual Tax: $4,162

Utilities

- Water & Sewer: Public

- Heating: Forced Air

- Cooling: Central Air

Location

- County: Hennepin

Listing Details

Investment Summary

- Monthly Cash Flow

- -$10,075

- Cap Rate

- 0.8%

- Cash-on-Cash Return

- -21.3%

- Debt Coverage Ratio

- 0.14

- Internal Rate of Return (5 years)

- -16.6%

Cash Flow

Net Operating Income (NOI) minus mortgage payments.

Calculation:

NOI - Mortgage Payments

Cap Rate (Market Value)

Capitalization Rate is a rate of return that compares the yearly Net Operating Income (NOI) to the market value.

Calculation:

NOI / Market Value

Cash-on-Cash Return (CoC)

Annual Cash Flow / Cash Invested

Calculation:

Annual cash flow divided by initial cash invested.

Debt Coverage Ratio (DCR)

Net Operating Income (NOI) divided by total debt payments.

Calculation:

NOI / Total Debt Payments

Internal Rate of Return (IRR)

A metric for assessing profitability over time. IRR is the discount rate at which the net present value (NPV) of all future cash flows (positive and negative) from an investment equals zero — including both periodic cash flow (such as rent) and a projected sale at the end of the holding period. It represents the expected annualized return, accounting for income, expenses, and the recovery of capital through a future sale.

Purchase Details

Purchase PriceThe price paid for the property. Purchase price:

| $2,464,000 |

|---|---|

Amount FinancedThe amount of the purchase financed through a loan. Amount financed:

| -$1,971,200 |

Down paymentThe initial payment made towards the purchase. Down payment:

| $492,800 |

Closing CostsFees and expenses associated with purchasing a property, typically ranging from 2% to 5% of the home’s purchase price, paid at the end of a home purchase to cover services like lending, title transfer, and taxes. Closing costs:

| $73,920 |

Rehab CostsCosts incurred to repair or improve the property, including: roof, flooring, exterior siding, kitchen, exterior paint, bathrooms, etc. Rehab costs:

| $0 |

Initial Cash InvestedThe total initial cash invested in the property. Calculation:Down payment + Buying costs + Rehab costs Initial cash invested:

| $566,720 |

Square Feet (SQFT)The total square footage of the property. Square feet:

| 4,092 |

Cost Per Square FootCost per square foot of the property. Calculation:Purchase Price / Square Feet Cost per square foot:

| $602 |

Monthly Rent Per Square FootMonthly rent divided by the number of square feet. This ratio helps investors compare rental income efficiency across properties, markets, and unit sizes Calculation:Monthly Rent / Square Feet Monthly rent per square foot:

| $0.68 |

Financing Details

Loan AmountThe total sum of money borrowed from a lender to finance a property purchase. Calculation:Purchase Price - Down Payment

Loan amount:

| $1,971,200 |

|---|---|

Loan to Value Ratio (LTV)Loan amount divided by the market value of the property. Calculation:Loan Amount / Market Value

Loan to value ratio:

| 80.0% |

Loan TypeThe type of loan (e.g., fixed, adjustable).

Loan type:

| Amortizing |

TermThe loan repayment period in years.

Term:

| 30 years |

Interest RateThe percentage a lender charges on the borrowed amount of a loan, determining the cost of borrowing money.

Interest rate:

| 5.875% |

Principal & Interest (PI)The principal is the portion of the loan payment that reduces the loan balance. The interest is the lender's charge for borrowing money. Calculation:(P * r * (1 + r) ** n) / ((1 + r) ** n - 1) Where:

P = Loan amount (principal)

Principal & interest:

| $11,660 |

Property TaxesAnnual taxes levied by local governments on real estate properties. These taxes fund public services like schools, roads, and emergency services.

Property tax:

| $347 |

InsuranceThe costs for insurance coverage to protect against financial losses due to risks like fire, natural disasters, theft, liability, or tenant-related damages. Calculation:Assumes 7% of gross rental income, unless insurance rates are specified.

Insurance:

| $196 |

Private Mortgage Insurance (PMI)A fee that borrowers pay when they take out a conventional loan with a loan-to-value (LTV) ratio above 80%.

Private mortgage insurance (PMI):

| $0 |

Monthly PaymentThe fixed amount a borrower pays each month to repay a loan. It typically includes principal and interest (P&I) and may also cover property taxes, insurance, HOA fees, and PMI if escrowed. Monthly payment:

| $12,203 |

Operating Income

| % Rent | Monthly | Yearly | |

|---|---|---|---|

Gross RentThe total rental income received from tenants before deducting any expenses. Includes base rent, late fees, pet fees, parking fees, and other recurring charges.

Gross rent:

| $2,800 | $33,600 | |

Vacancy LossExpected loss of rent due to vacancies.

Vacancy loss:

(6%)

| 6% | -$168 | -$2,016 |

Operating IncomeGross rental income minus vacancy loss. Calculation:Gross rent - Vacancy loss

Operating income:

| $2,632 | $31,584 |

Operating Expenses

| % Rent | Monthly | Yearly | |

|---|---|---|---|

Property TaxesAnnual taxes levied by local governments on real estate properties. These taxes fund public services like schools, roads, and emergency services. | 12% | -$347 | -$4,162 |

InsuranceThe costs for insurance coverage to protect against financial losses due to risks like fire, natural disasters, theft, liability, or tenant-related damages. Calculation:Assumes 7% of gross rental income, unless insurance rates are specified. | 7% | -$196 | -$2,352 |

Property ManagementThe costs associated with hiring a property manager to handle the day-to-day operations of a rental property. Includes management fees, leasing fes, eviction fees, etc. Calculation:Assumes 8% of gross rental income. | 8% | -$224 | -$2,688 |

Repairs & MaintenanceOngoing costs for routine upkeep and minor fixes needed to keep a property in good working condition. Calculation:Assumes 5% of gross rental income. Varies by property age and condition. | 5% | -$140 | -$1,680 |

Capital ExpensesLarge, infrequent costs for major improvements or replacements, like a new roof, HVAC system, or appliances. Calculation:Assumes 5% of gross rental income. Varies by property age. | 5% | -$140 | -$1,680 |

HOA FeesRegular dues paid to a Homeowners Association for community maintenance, amenities, and management. Similar fees include: Condo Association Fees, Co-op Maintenance Fees, etc. | n/a | n/a | n/a |

Operating ExpensesRecurring costs required to maintain and manage a rental property, including property taxes, insurance, maintenance, repairs, utilities (if paid by the owner), property management fees, and other day-to-day expenses. Calculation:Insurance + Property Taxes + Property Management + Repairs & Maintenance + Capital Expenditures + HOA Fees | 37% | -$1,047 | -$12,562 |

Cash Flow

| Monthly | Yearly | |

|---|---|---|

Net Operating Income (NOI)The income generated from a property after deducting all operating expenses but before deducting mortgage payments, taxes, and capital expenditures. Calculation:Gross Operating Income - Operating Expenses

Net operating income:

| $1,585 | $19,020 |

Mortgage PaymentThe fixed amount a borrower pays each month to repay a loan. It typically includes principal and interest (P&I) and may also cover property taxes, insurance, HOA fees, and PMI if escrowed. | -$11,660 | -$139,920 |

Cash FlowNet Operating Income (NOI) minus mortgage payments. Calculation:NOI - Mortgage Payments | -$10,075 | -$120,900 |