$749,000

Investment Summary

We noticed that property taxes are missing—this is a standard expense and should be considered in your estimate.

- Monthly Cash Flow

- -$853

- Cap Rate

- 4.3%

- Cash-on-Cash Return

- -5.9%

- Debt Coverage Ratio

- 0.76

- Internal Rate of Return (5 years)

- -1.8%

Cash Flow

Net Operating Income (NOI) minus mortgage payments.

Calculation:

NOI - Mortgage Payments

Cap Rate (Market Value)

Capitalization Rate is a rate of return that compares the yearly Net Operating Income (NOI) to the market value.

Calculation:

NOI / Market Value

Cash-on-Cash Return (CoC)

Annual Cash Flow / Cash Invested

Calculation:

Annual cash flow divided by initial cash invested.

Debt Coverage Ratio (DCR)

Net Operating Income (NOI) divided by total debt payments.

Calculation:

NOI / Total Debt Payments

Internal Rate of Return (IRR)

A metric for assessing profitability over time. IRR is the discount rate at which the net present value (NPV) of all future cash flows (positive and negative) from an investment equals zero — including both periodic cash flow (such as rent) and a projected sale at the end of the holding period. It represents the expected annualized return, accounting for income, expenses, and the recovery of capital through a future sale.

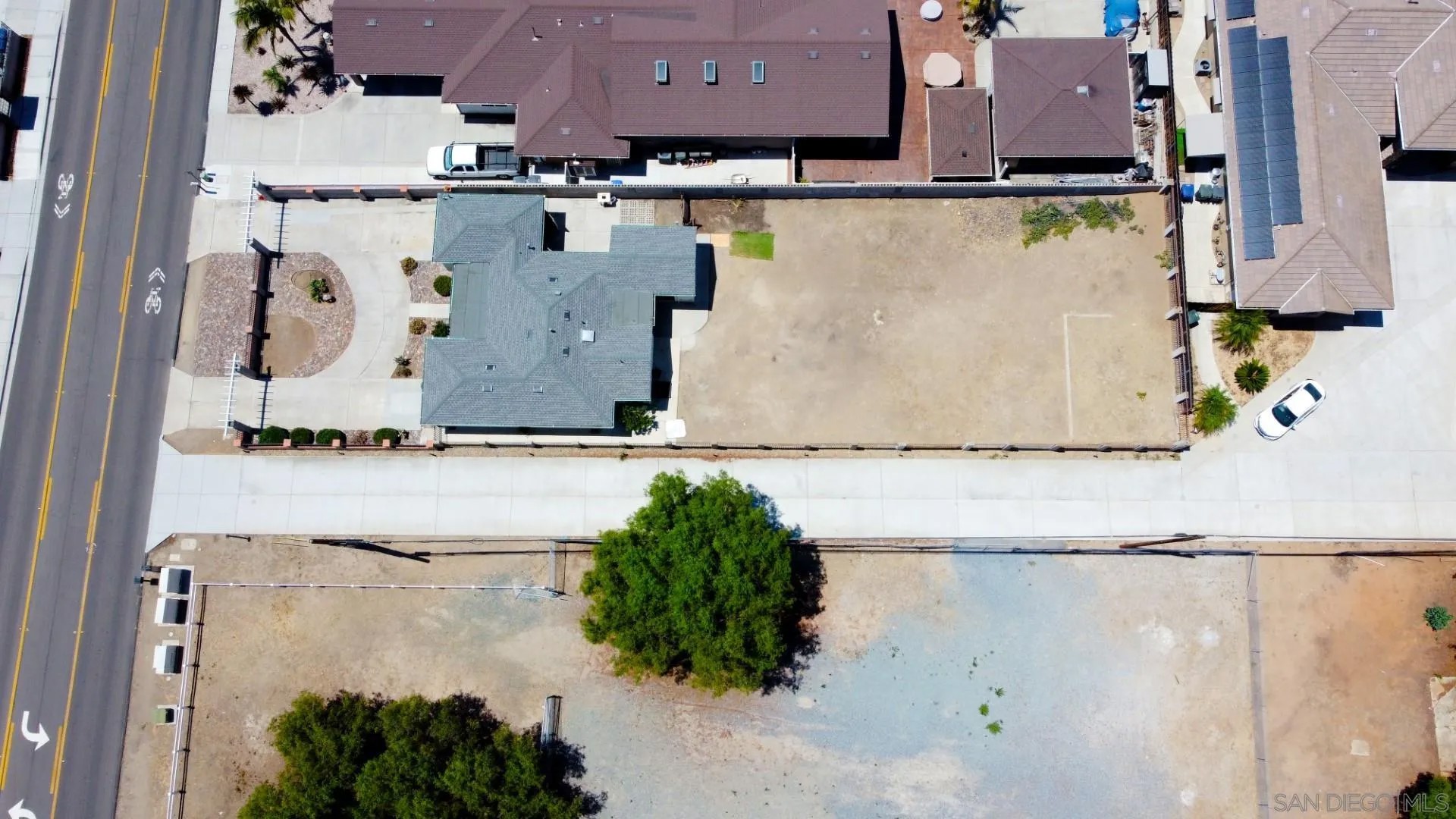

Property Description

A rare Bonita opportunity to build significant equity awaits with this family home on a sprawling, park-like lot—the largest and most promising parcel available in its price range. The vast, usable land is a blank canvas, offering limitless potential for a high-income ADU, a private pool oasis, and your dream backyard. The home itself is a structurally sound foundation with unique, convenient features like a pass-through garage, awaiting your personal touches to add immense and immediate value. Nestled in a premier family community, enjoy a short, safe walk to the highly-regarded elementary school, with the vast greenbelts of Rohr Park, local golf courses, and the trails of Sweetwater Reservoir just minutes away. Your investment is strategically secured by the proximity to the multi-billion dollar Chula Vista Bayfront redevelopment, a landmark project set to boost the entire region's value. This is a unique opportunity to acquire a legacy property offering an unmatched combination of land, lifestyle, and financial upside. Disclaimer: The following information is provided for informational purposes only and is based on documents provided by the seller. This summary is intended to be a helpful overview and is not a guarantee of development potential. All buyers and their agents are strongly advised to conduct their own independent investigations and due diligence with the appropriate city, county, and state agencies to verify all information, including but not limited to zoning, permits, fees, and building regulations. Do not rely solely on the statements presented here. Summary of Development Potential for 5361 Central Ave, Bonita, CA 91902 Based on the provided documents, here is a breakdown of the property's zoning and potential for additional units. Property Zoning Information The property is located in an unincorporated community of San Diego County. Zone: RS (Residential Single). Building Type: C - Allows for one single detached dwelling unit per lot. Minimum Lot Size: 10,000 sq. ft.. Maximum Height: G - 35 feet or 2 stories. Setbacks: The "H" designation requires specific setbacks: Front: 50 feet (measured from the centerline). Side: 10 feet. Rear: 25 feet. Option 1: Accessory Dwelling Unit (ADU) Development Under standard ADU regulations, the property could potentially accommodate a total of three units on the lot. This would include the existing main home plus two additional units. (1) Junior Accessory Dwelling Unit (JADU): This involves converting a portion of the existing primary house into a separate unit. A garage conversion for a JADU has a maximum size of 500 sq. ft.. (1) Accessory Dwelling Unit (ADU): This can be either attached to the main home or built as a separate, detached structure. Detached ADU: A new, standalone structure. The maximum allowed size is 1,200 sq. ft.. Attached ADU: An addition that shares at least one wall with the primary house. The maximum size is up to 50% of the existing home's square footage. Conversion ADU: An existing garage or other permitted accessory structure can be converted into an ADU. The County of San Diego offers several pre-approved ADU building plans ranging from 600 to 1,200 sq. ft.. Option 2: Senate Bill 9 (SB9) Development The property meets the criteria for California Senate Bill 9 (SB9), which may allow for more extensive development. Eligibility: The parcel is located within an Urban Area and a single-family zone , and it does not intersect a Very High Fire Hazard Severity Zone. Maximum Units: SB9 projects are limited to a maximum of four units on the property. Unit Combination: This could include two primary units, one ADU, and one JADU, as long as the total does not exceed four units on the lot. Potential Building Permit Fees The County of San Diego has a fee schedule for building construction permits (effective 07/01/2025). For an Accessory Dwelling Unit, the estimated fees would be: Guest House/Accessory Dwelling Unit: Plan Review Fee: $1,865 + $0.394 per sq. ft.. Permit Fee: $1,596 + $0.537 per sq. ft.. Accessory Dwelling Unit for OTC Review: Plan Review Fee: $1,084 + $0.304 per sq. ft.. Permit Fee: $1,596 + $0.537 per sq. ft.. Important Considerations Septic System: If the property is on a septic system, it may be subject to additional requirements for development.

Build Your Team

Quickly find investor-friendly professionals who can help you succeed in real estate investing at any stage of the investing journey.

Agents

Match with investor-friendly agents who can help you find, analyze, and close your next deal

Lenders

Get the best funding…find investor-friendly lenders who specialize in your deal strategy

Property Managers

Transition to passive investing. Find a trusted property management partnership that lasts.

Tax Pros & Accountants

Taxes and financial reporting made easy—find experts to create tax savings strategies, file taxes, and more

Location

Property Details

Parking

- Description: Garage

- Details: Attached, Garage, Garage Door Opener

- Garage Spaces: 1

- Spaces Total: 5

Bedroom Information

- # of Bedrooms: 3

Bathroom Information

- # of Baths (Full): 2

- # of Baths (Total): 2.0

Interior Features

- # of Stories: 1

Exterior Features

- Roof Material: Composition

Land Information

- Land Use: Residential

- Land Use Subtype: Single Family Residential

Lot Information

- Parcel ID: 5901600800

- Lot Size: 0 sqft

Property Information

- Property Type: Single Family Residence

- Style: Craftsman

- Year Built: 1954

Tax Information

- Annual Tax: $0

Utilities

- Water & Sewer: Public

- Heating: Natural Gas

Location

- County: San Diego

Listing Details

Investment Summary

We noticed that property taxes are missing—this is a standard expense and should be considered in your estimate.

- Monthly Cash Flow

- -$853

- Cap Rate

- 4.3%

- Cash-on-Cash Return

- -5.9%

- Debt Coverage Ratio

- 0.76

- Internal Rate of Return (5 years)

- -1.8%

Cash Flow

Net Operating Income (NOI) minus mortgage payments.

Calculation:

NOI - Mortgage Payments

Cap Rate (Market Value)

Capitalization Rate is a rate of return that compares the yearly Net Operating Income (NOI) to the market value.

Calculation:

NOI / Market Value

Cash-on-Cash Return (CoC)

Annual Cash Flow / Cash Invested

Calculation:

Annual cash flow divided by initial cash invested.

Debt Coverage Ratio (DCR)

Net Operating Income (NOI) divided by total debt payments.

Calculation:

NOI / Total Debt Payments

Internal Rate of Return (IRR)

A metric for assessing profitability over time. IRR is the discount rate at which the net present value (NPV) of all future cash flows (positive and negative) from an investment equals zero — including both periodic cash flow (such as rent) and a projected sale at the end of the holding period. It represents the expected annualized return, accounting for income, expenses, and the recovery of capital through a future sale.

Purchase Details

Purchase PriceThe price paid for the property. Purchase price:

| $749,000 |

|---|---|

Amount FinancedThe amount of the purchase financed through a loan. Amount financed:

| -$599,200 |

Down paymentThe initial payment made towards the purchase. Down payment:

| $149,800 |

Closing CostsFees and expenses associated with purchasing a property, typically ranging from 2% to 5% of the home’s purchase price, paid at the end of a home purchase to cover services like lending, title transfer, and taxes. Closing costs:

| $22,470 |

Rehab CostsCosts incurred to repair or improve the property, including: roof, flooring, exterior siding, kitchen, exterior paint, bathrooms, etc. Rehab costs:

| $0 |

Initial Cash InvestedThe total initial cash invested in the property. Calculation:Down payment + Buying costs + Rehab costs Initial cash invested:

| $172,270 |

Square Feet (SQFT)The total square footage of the property. Square feet:

| 1,304 |

Cost Per Square FootCost per square foot of the property. Calculation:Purchase Price / Square Feet Cost per square foot:

| $574 |

Monthly Rent Per Square FootMonthly rent divided by the number of square feet. This ratio helps investors compare rental income efficiency across properties, markets, and unit sizes Calculation:Monthly Rent / Square Feet Monthly rent per square foot:

| $2.99 |

Financing Details

Loan AmountThe total sum of money borrowed from a lender to finance a property purchase. Calculation:Purchase Price - Down Payment

Loan amount:

| $599,200 |

|---|---|

Loan to Value Ratio (LTV)Loan amount divided by the market value of the property. Calculation:Loan Amount / Market Value

Loan to value ratio:

| 80.0% |

Loan TypeThe type of loan (e.g., fixed, adjustable).

Loan type:

| Amortizing |

TermThe loan repayment period in years.

Term:

| 30 years |

Interest RateThe percentage a lender charges on the borrowed amount of a loan, determining the cost of borrowing money.

Interest rate:

| 5.875% |

Principal & Interest (PI)The principal is the portion of the loan payment that reduces the loan balance. The interest is the lender's charge for borrowing money. Calculation:(P * r * (1 + r) ** n) / ((1 + r) ** n - 1) Where:

P = Loan amount (principal)

Principal & interest:

| $3,544 |

Property TaxesAnnual taxes levied by local governments on real estate properties. These taxes fund public services like schools, roads, and emergency services.

Property tax:

| $0 |

InsuranceThe costs for insurance coverage to protect against financial losses due to risks like fire, natural disasters, theft, liability, or tenant-related damages. Calculation:Assumes 7% of gross rental income, unless insurance rates are specified.

Insurance:

| $273 |

Private Mortgage Insurance (PMI)A fee that borrowers pay when they take out a conventional loan with a loan-to-value (LTV) ratio above 80%.

Private mortgage insurance (PMI):

| $0 |

Monthly PaymentThe fixed amount a borrower pays each month to repay a loan. It typically includes principal and interest (P&I) and may also cover property taxes, insurance, HOA fees, and PMI if escrowed. Monthly payment:

| $3,817 |

Operating Income

| % Rent | Monthly | Yearly | |

|---|---|---|---|

Gross RentThe total rental income received from tenants before deducting any expenses. Includes base rent, late fees, pet fees, parking fees, and other recurring charges.

Gross rent:

| $3,900 | $46,800 | |

Vacancy LossExpected loss of rent due to vacancies.

Vacancy loss:

(6%)

| 6% | -$234 | -$2,808 |

Operating IncomeGross rental income minus vacancy loss. Calculation:Gross rent - Vacancy loss

Operating income:

| $3,666 | $43,992 |

Operating Expenses

| % Rent | Monthly | Yearly | |

|---|---|---|---|

Property TaxesAnnual taxes levied by local governments on real estate properties. These taxes fund public services like schools, roads, and emergency services.

We noticed that property taxes are missing—these are standard expenses and should be considered in your estimate. | n/a | n/a | n/a |

InsuranceThe costs for insurance coverage to protect against financial losses due to risks like fire, natural disasters, theft, liability, or tenant-related damages. Calculation:Assumes 7% of gross rental income, unless insurance rates are specified. | 7% | -$273 | -$3,276 |

Property ManagementThe costs associated with hiring a property manager to handle the day-to-day operations of a rental property. Includes management fees, leasing fes, eviction fees, etc. Calculation:Assumes 8% of gross rental income. | 8% | -$312 | -$3,744 |

Repairs & MaintenanceOngoing costs for routine upkeep and minor fixes needed to keep a property in good working condition. Calculation:Assumes 5% of gross rental income. Varies by property age and condition. | 5% | -$195 | -$2,340 |

Capital ExpensesLarge, infrequent costs for major improvements or replacements, like a new roof, HVAC system, or appliances. Calculation:Assumes 5% of gross rental income. Varies by property age. | 5% | -$195 | -$2,340 |

HOA FeesRegular dues paid to a Homeowners Association for community maintenance, amenities, and management. Similar fees include: Condo Association Fees, Co-op Maintenance Fees, etc. | n/a | n/a | n/a |

Operating ExpensesRecurring costs required to maintain and manage a rental property, including property taxes, insurance, maintenance, repairs, utilities (if paid by the owner), property management fees, and other day-to-day expenses. Calculation:Insurance + Property Taxes + Property Management + Repairs & Maintenance + Capital Expenditures + HOA Fees | 25% | -$975 | -$11,700 |

Cash Flow

| Monthly | Yearly | |

|---|---|---|

Net Operating Income (NOI)The income generated from a property after deducting all operating expenses but before deducting mortgage payments, taxes, and capital expenditures. Calculation:Gross Operating Income - Operating Expenses

Net operating income:

| $2,691 | $32,292 |

Mortgage PaymentThe fixed amount a borrower pays each month to repay a loan. It typically includes principal and interest (P&I) and may also cover property taxes, insurance, HOA fees, and PMI if escrowed. | -$3,544 | -$42,528 |

Cash FlowNet Operating Income (NOI) minus mortgage payments. Calculation:NOI - Mortgage Payments | -$853 | -$10,236 |