All Forum Posts by: Devin Peterson

Devin Peterson has started 121 posts and replied 1703 times.

Post: Looking for a Fix & Flip Mentor in Connecticut (CT)

Post: Looking for a Fix & Flip Mentor in Connecticut (CT)

- Lender

- Sarasota, FL

- Posts 1,830

- Votes 623

Karan,

Local investor and broker here in CT - happy to connect you with the right person. Let's chat!

Post: Refinancing Your Rental

- Lender

- Sarasota, FL

- Posts 1,830

- Votes 623

Quote from @Jeanette Land:

Hello everyone, I'm inquiring the refinancing part of the BRRRR method. What happens to your cash flow when you refinance the property you fixed up and take the cash out?

Your cash flow should increase! If you have a high-interest-only loan you should be able to cash flow MORE. The lender will not close a loan for you with a higher DSCR than 1.00 which means, no cash flow. I reccommend connecting with an experienced loan broker who can price out a few differnt loan options for you

Post: Any reliable loan broker here?

- Lender

- Sarasota, FL

- Posts 1,830

- Votes 623

Quote from @Steve Dorian:

I am looking to partner with a reliable loan broker long term

What is your loan scenario? Can you elaborate a bit on what you are looking for?

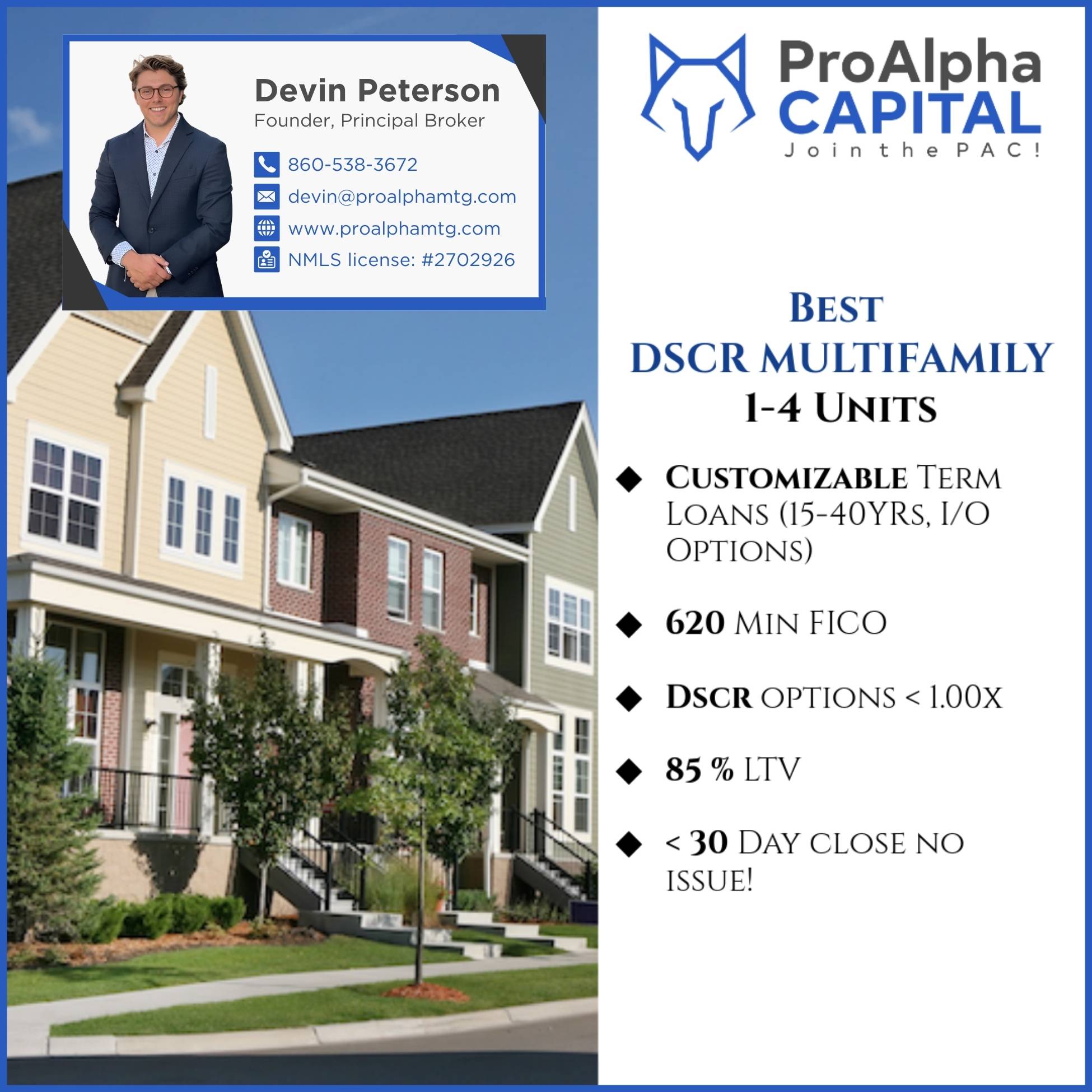

Post: Best DSCR Multifamily Loans - 1-4 Units - ProAlpha Capital

- Lender

- Sarasota, FL

- Posts 1,830

- Votes 623

Get the absolute best RATES and SERVICE that you will find in the DSCR space!

#🥇 in product analysis - Don't just settle for "chocolate" or "vanilla" There is a reason Ben & Jerry's Ice Cream has over 100 different flavors. Let us find the absolute best DSCR fit for your needs!

#🥇in client relationship management - Don’t get stuck in the masses. Work 1:1 directly with your broker from pre-approval to closing day! No fuss!

#🥇 in risk analysis and Pro-forma education - Other DSCR lenders will just show you the rates and fees. We take pride in the deals we work on. That means, personalized underwriting services for investors who want additional opinions.

🚀 Trust the #🥇 broker in the DSCR space to close even the toughest of deals!

✅ Customizable loan terms

✅ No Income Required

✅ No Employment Verification

✅ No W2s or Tax Returns

✅ Close in your LLC

✅ Non-credit reporting option

✅ DSCR < 1.00 is OKAY

✅ All 50 States

👉 Check out our website:

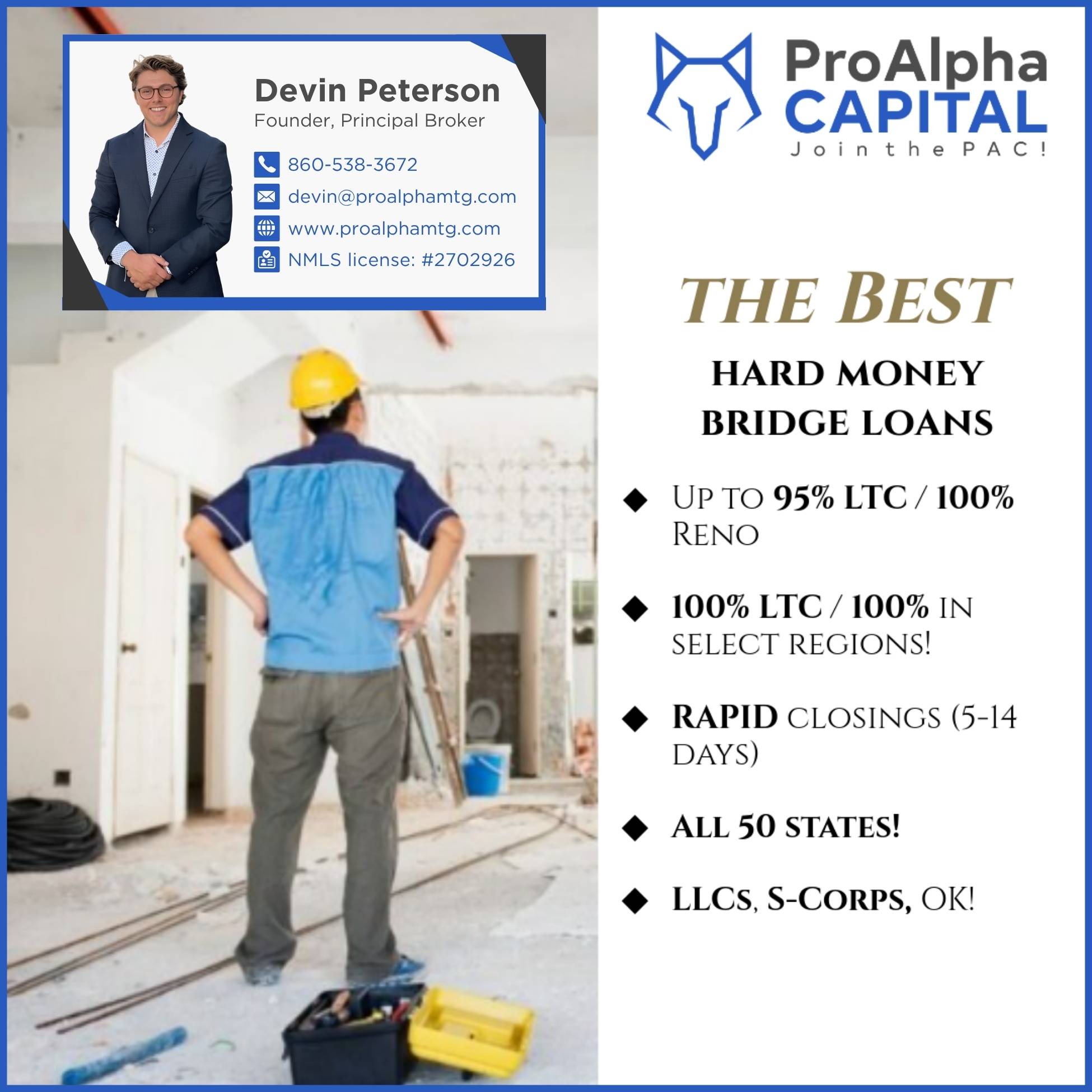

Post: Best Hard Money Bridge Loans - ProAlpha Capital

- Lender

- Sarasota, FL

- Posts 1,830

- Votes 623

Deals happen FAST! Trust a broker with 60+ years of combined experience to get in the win column!

🚀 WIN your next “Bridge” / “Fix to Flip” / “Fix to Rent” loan with ease.

✅ We allow first-time bridge investors!

✅ Get up to 95 LTC and 100 LTC in select states!

✅ Close quick! Super lite doc bridge loans allow for SPEED!

✅ Unbelievably EASY draw process!

👉 Check out our website:

Post: Best Hard Money Bridge Loans - ProAlpha Capital

- Lender

- Sarasota, FL

- Posts 1,830

- Votes 623

Deals happen FAST! Trust a broker with 60+ years of combined experience to get in the win column!

🚀 WIN your next “Bridge” / “Fix to Flip” / “Fix to Rent” loan with ease.

✅ We allow first-time bridge investors!

✅ Get up to 95 LTC and 100 LTC in select states!

✅ Close quick! Super lite doc bridge loans allow for SPEED!

✅ Unbelievably EASY draw process!

👉 Check out our website:

👉 Schedule a FREE consultation:

https://calendly.com/devinpeterson

Post: Best Investor/ DSCR Specialty Broker - 1-4 & 5-25+ Units - ProAlpha Capital

- Lender

- Sarasota, FL

- Posts 1,830

- Votes 623

Mortgage shopping can be a tall task - let us handle the heavy lifting!

✅ Tailored mortgage broker services for all your investment needs!

✅ We say YES when others say NO!

✅ FREE Pro-Forma Modeling Assistance with EVERY locked loan!

👉 Check out our website:

Post: Best Commercial Broker - 25-200+ Units - ProAlpha Capital

- Lender

- Sarasota, FL

- Posts 1,830

- Votes 623

Work with investment-focused brokers who KNOW real estate investing!

🚀 We go beyond the traditional DSCR lender's maximum unit capacity!

✅ 1000+ commercial lending partners

✅ Flexible Lending Terms

✅ Debt Funds, Private Capital, Mezzanine Deb

✅ All 50 States

👉 Check out our website:

👉 Schedule a FREE consultation:

Post: Looking for a possible 40 year dscr loan in RI

- Lender

- Sarasota, FL

- Posts 1,830

- Votes 623

Quote from @Justin Chan:

Please contact me if you are capable of processing a 40 yr dscr loan in the state of RI. Thank you.

Every reliable DSCR lender has this option - what are you looking for specifically?

Post: Renovation loan for triplex

- Lender

- Sarasota, FL

- Posts 1,830

- Votes 623

Quote from @Nana Sefa:

I a looking for any lender that has a product that can finance a renovation loan for a triplex. Looking for a product that can finance both the purchase and the renovation costs. Happy to discuss various down payment options. Any recommendations? Thank you.