Friday, 9/5/25: Interest Rates are Moving....Why?

I’ve been a banking executive, real estate investor, and lender for nearly 35 years now and I know how hard it is to get good info on the markets. That’s why I enjoy logging on to BP. There are a lot of perspectives and a lot of good people just trying to learn. That being said, today we’re seeing a ton of volatility in the interest rate markets and I thought I would tailor a post to help newer, “non-econ” people to understand what’s happening and what direction rates are heading (and why).

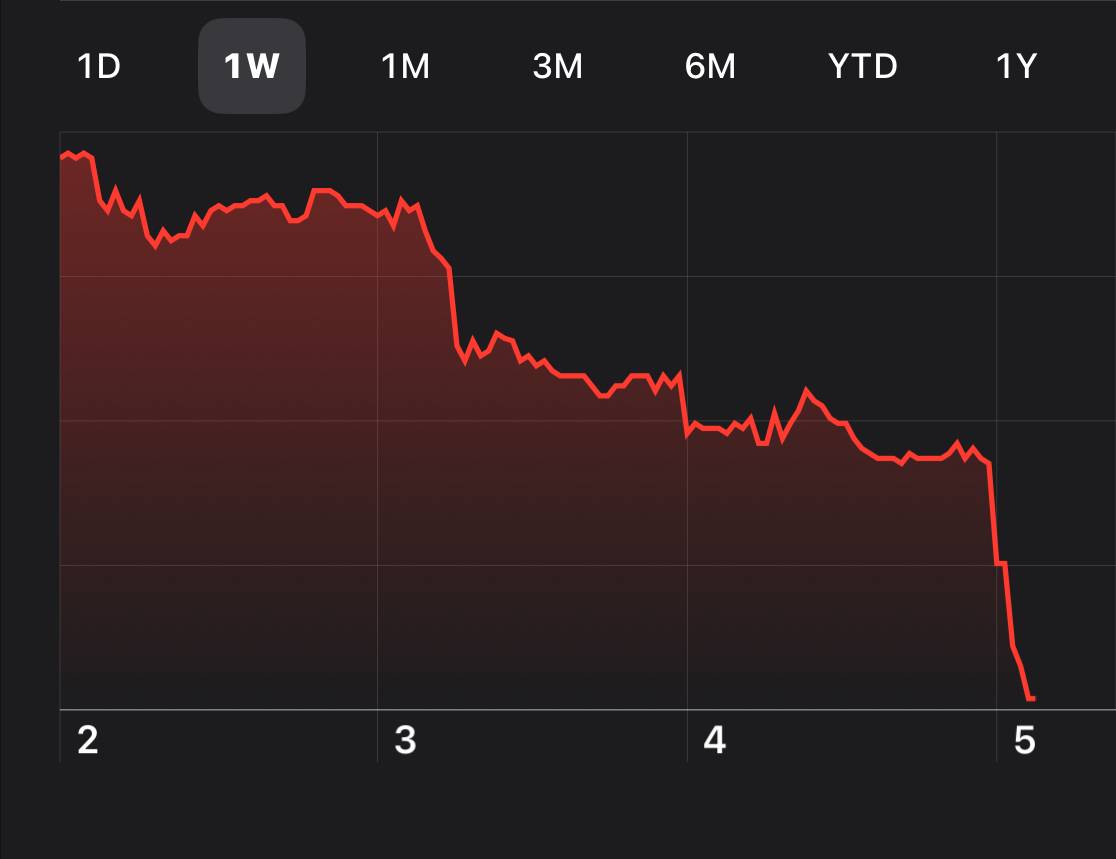

I know I’ve posted about Long-Term Mortgage Rates and the Federal Funds Rate not being directly tied, but this morning’s economic report will impact both. The attached chart is the 10-Year Treasury and you need to watch it closely (“TNX” on your smart phone’s stock ticker). Long-Term Mortgage Rates WILL move in lock-step with the 10-Year Treasury. As you can see, its cratering. Jobs data came in 22,000 lower than expected with losses in most sectors including 19,000 in manufacturing alone. Unemployment is up and I think you’ll see inflation tick up next month as well. Watch that index closely. It’s going to be a volatile day and it will remain so into next week at least, but this indicator tells us that rates ARE coming down.

Now, let’s switch gears to the Federal Reserve. This is not a political statement, but a statement of fact. Chairman Powell and President Trump are not on each other’s Christmas Card list. I suspect the Fed has wanted to lower rates, but they’ve held off as to not look like they are bending to the President’s will. With this data, however, this gives them the political cover to lower rates by 25 bps with an outside shot at a 50 bps drop. This will impact commercial loans, car loans, and equity lines (HELOCs).

I do hope this helps you and your customers. I’m always happy to “talk shop” is anyone wants to chat.

Doug