All Forum Posts by: Marcus Auerbach

Marcus Auerbach has started 166 posts and replied 4835 times.

Post: RPA-CON 2025: Wisconsin's Largest Real Estate Investor Convention and Expo

Post: RPA-CON 2025: Wisconsin's Largest Real Estate Investor Convention and Expo

- Investor and Real Estate Agent

- Milwaukee - Mequon, WI

- Posts 4,953

- Votes 7,156

Post: RPA-CON 2025: Wisconsin's Largest Real Estate Investor Convention and Expo

- Investor and Real Estate Agent

- Milwaukee - Mequon, WI

- Posts 4,953

- Votes 7,156

Here is a quick video about RPA-CON 2025 in Milwaukee next Friday Oct 17th!

I have 5 free tickets for the first 5 people who comment below!

See you there!

Post: Pros & Cons of Listing Property End of Year

- Investor and Real Estate Agent

- Milwaukee - Mequon, WI

- Posts 4,953

- Votes 7,156

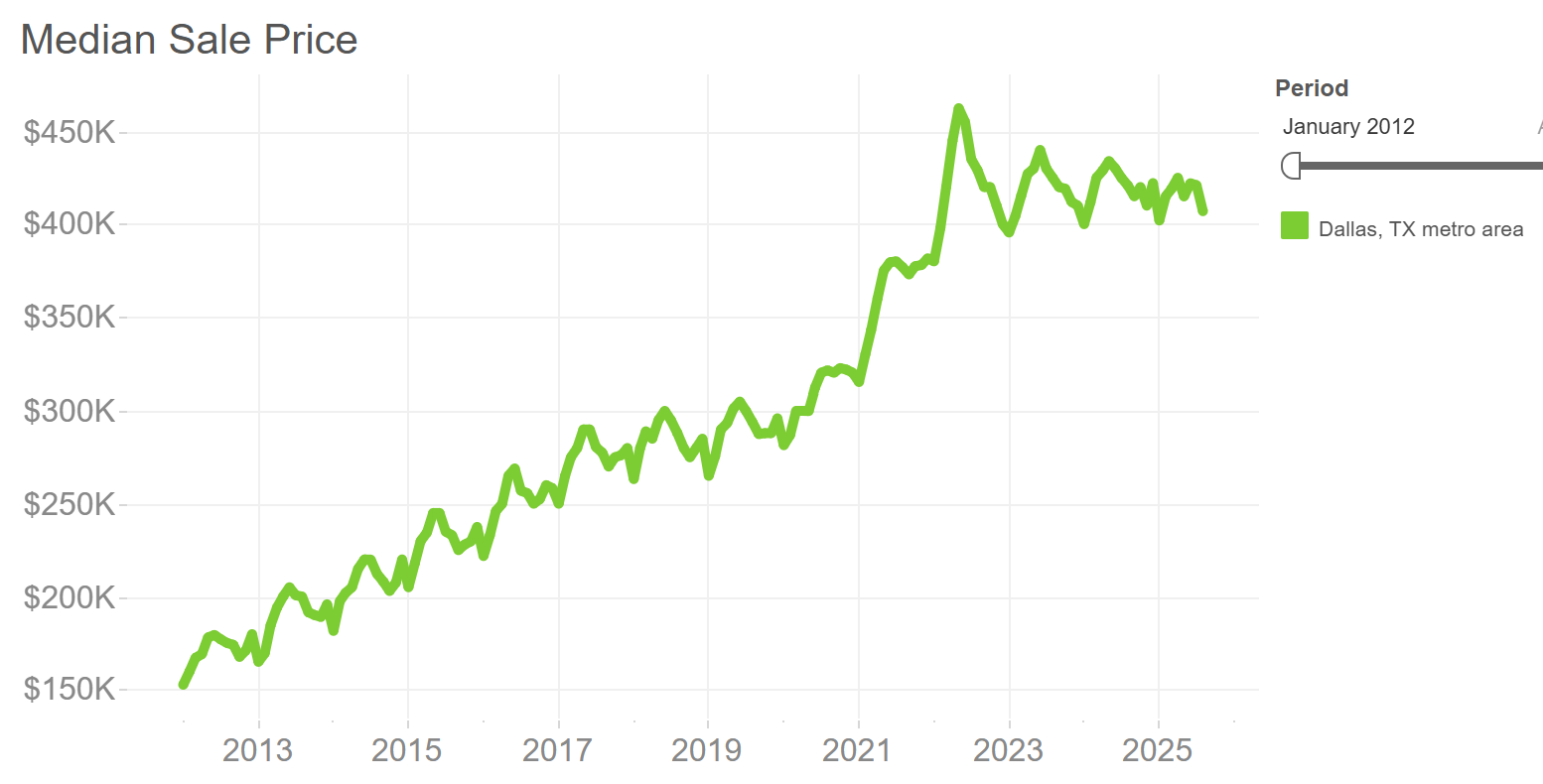

The holiday season is definitely the worst time to sell a house.

Just look It always takes a little longer, so you'll probably wrap up a month later anyway and the beginning of January is already so much better, because people make plans to buy a house "next year" and "after the holiday"- you can see it in the data: guess when the lows happen every year.

Nice price consolidation BTW..

Post: We Almost closed on an $18M Deal — here's why we walked away.

- Investor and Real Estate Agent

- Milwaukee - Mequon, WI

- Posts 4,953

- Votes 7,156

I don't get it either.

Roof condition is something that my brain checks automatically while I get out of the car the first time I see a building. And while it's not always easy to tell from the ground if a roof is on it's 2nd third or last third of its life - the difference between brand new and totally shot is normally pretty obvious.

And the cost of the roof should have been more than offset by the interest rates getting lower of the last 6 months.

There must be more to that story..

Post: prospective tenant would like to make 2 pages of changes to the lease

- Investor and Real Estate Agent

- Milwaukee - Mequon, WI

- Posts 4,953

- Votes 7,156

Leases have to be state law-compliant, so I should not comment on the specifics. But I am getting the impression you are using a home made lease (could be from an attorney, equally bad). A good lease is a pre-printed form, widely circulated and tested in court thousands of time and occasionally revised. I am sure something like this exsists in NYS and no - you don't want to make ANY modifications to a court tested lease.

We have case law in Wisconsin where landlords had to pay 6 digit numbers because their lease included what Wi law defines as 10 deadly sins - and they are not super straight forward, so even attorneys' leases got caught.

Post: Which agent is at fault?

- Investor and Real Estate Agent

- Milwaukee - Mequon, WI

- Posts 4,953

- Votes 7,156

Not a great look for either agent, you can blame them, but that is inconsequential. I assume you got a pre-approval letter with the offer. Did the lender approve the buyer without a home sale contingency or did everyone overlook that?

Before you CAMR the deal, is the buyers listing under contract and if so when wil they close? In that case your shorter path to success is to stick with them.

Post: Investing in duplexes and fourplexes, worth it?

- Investor and Real Estate Agent

- Milwaukee - Mequon, WI

- Posts 4,953

- Votes 7,156

There is a BIG difference between duplexes and fourplexes. The argument of "more units under one roof" is really shallow. Both will generally cashflow better than single-family homes, but that comes with additional management efforts, so you are working for the cash flow.

In my market (Milwaukee) I would choose a typical duplex over a Fourplex every time. Duplexes are ubiquitous here, also in good, desirable neighborhoods and tend to generate higher rents per unit. Fourplexes are typically built in clusters and are generally more often in the category "affordable housing". Duplexes typically have larger units and more bedrooms compared to quads. This is important because rent/unit is a function of both square footage and bedroom count.

Financial considerations:

The ratio of rent to the cost of ownership per unit is significantly better with duplxes. In a fourplex you share 1 roof (albeit it's larger), but still have 1 kitchen, 1 bathroom, 1 water heater etc to maintain - and they all cost the same to repair or replace, regardless if your rent is $800 or $1600 per unit. Bedroom and living space sqft is cheap to maintain, but that is what brings in more rent. The only cost synergy you have is maybe the roof, but that's once every 30 years and it's is also larger on a fourplex, so the argument is weak at best.

Tenant management:

The other issues are social dynamics. Single-family homes are the most stable, because they are self-contained. In a duplex, you have 2 tenants that share common space, so there is 1 social interaction between them. In a fourplex, every tenant has 3 other tenants to get along with, so that's 6 social interactions - and a lot more opportunity for drama. This gets amplified if you are renting to a lower-income demographic.

Personally, we invest in single-family homes, because when I started 17 years ago and had a corporate job with a lot of international travel they were the easiest to manage for me. A similar considertion applies for OOS investors, SF's are the closest thing to passive you ca get. Cash flow tends to be lower, but equity works a little better.

We have 66,000 duplexes in Milwaukee, more than any other city in the US (yes, including Chicago), yet there are typically very few on the market. They make excellent house hacks to get started and most people don't sell them when they move, because they already know how to rent out one unit, so might as well just rent the second.

This is why they are not easy to buy; in most cases, the owner has lost interest years ago before they hit the market and there is quite a bit of deferred maintenance, outdated leases, rent below market etc to fix for the new owner.

Post: RPA-CON 2025: Wisconsin's Largest Real Estate Investor Convention and Expo

- Investor and Real Estate Agent

- Milwaukee - Mequon, WI

- Posts 4,953

- Votes 7,156

Take advantage of the early bird ticket discount!

Details: RPA-CON.com

See you there!

# Milwaukee, Wisconsin, Madison, Green Bay, Fox Valley, Appleton, Chicago, Illinois

Post: Tenant From Hell - HELP

- Investor and Real Estate Agent

- Milwaukee - Mequon, WI

- Posts 4,953

- Votes 7,156

This is only going to get worse, get an eviction attorney and follow through no matter what. This relationship is broken beyond repair.

On the bright side: you have to deal with a situation like this sooner or later, it's part of the biz. The good news is that you get to do this early and it will make you a better landlord. We have all had a few tough ones, they teach you a lot!

Post: Help shape the next chapter of BiggerPockets (and earn $50)!

- Investor and Real Estate Agent

- Milwaukee - Mequon, WI

- Posts 4,953

- Votes 7,156

@Rene Hosman I understand that $50 are well well-intended, but what we try to contribute here is not for a few bucks. You are getting this reaction because it feels a little like the old "hey I'll buy you Starbucks or a steak dinner if you let me pick your brain for an hour and tell me everything you have learned over half a life-time of investing.."