All Forum Posts by: Andrew Zee

Andrew Zee has started 1 posts and replied 6 times.

Post: When an ARM Isn’t What It Seems: $21,000 Surprise in My 10/30-Year Interest-Only Loan

Post: When an ARM Isn’t What It Seems: $21,000 Surprise in My 10/30-Year Interest-Only Loan

- Posts 6

- Votes 0

@Russell Brazil yup going to schedule an extra payments to get this thing paid off in 20 to 25 years or earlier....

IO = interest only ---YUK Not aware of IO in a term sheet. Now I know...

Thanks

Post: When an ARM Isn’t What It Seems: $21,000 Surprise in My 10/30-Year Interest-Only Loan

- Posts 6

- Votes 0

@Patrick Roberts thanks for the explanation this helps.

Post: When an ARM Isn’t What It Seems: $21,000 Surprise in My 10/30-Year Interest-Only Loan

- Posts 6

- Votes 0

@Brandon Croucier Thanks for your response

Post: When an ARM Isn’t What It Seems: $21,000 Surprise in My 10/30-Year Interest-Only Loan

- Posts 6

- Votes 0

Patrick, thanks for weighing in, but your take feels like you’re blaming me for breaking your window.

-

The Term Sheet never said “interest-only.” It said "ARM."

-

My actual payment is $1,145/month (interest + escrow). That’s the number I budgeted.

-

I’ve run the numbers: if I add $900/year toward principal, I’ll pay this off in 25 years, exactly as expected for a 30-year loan with that extra.

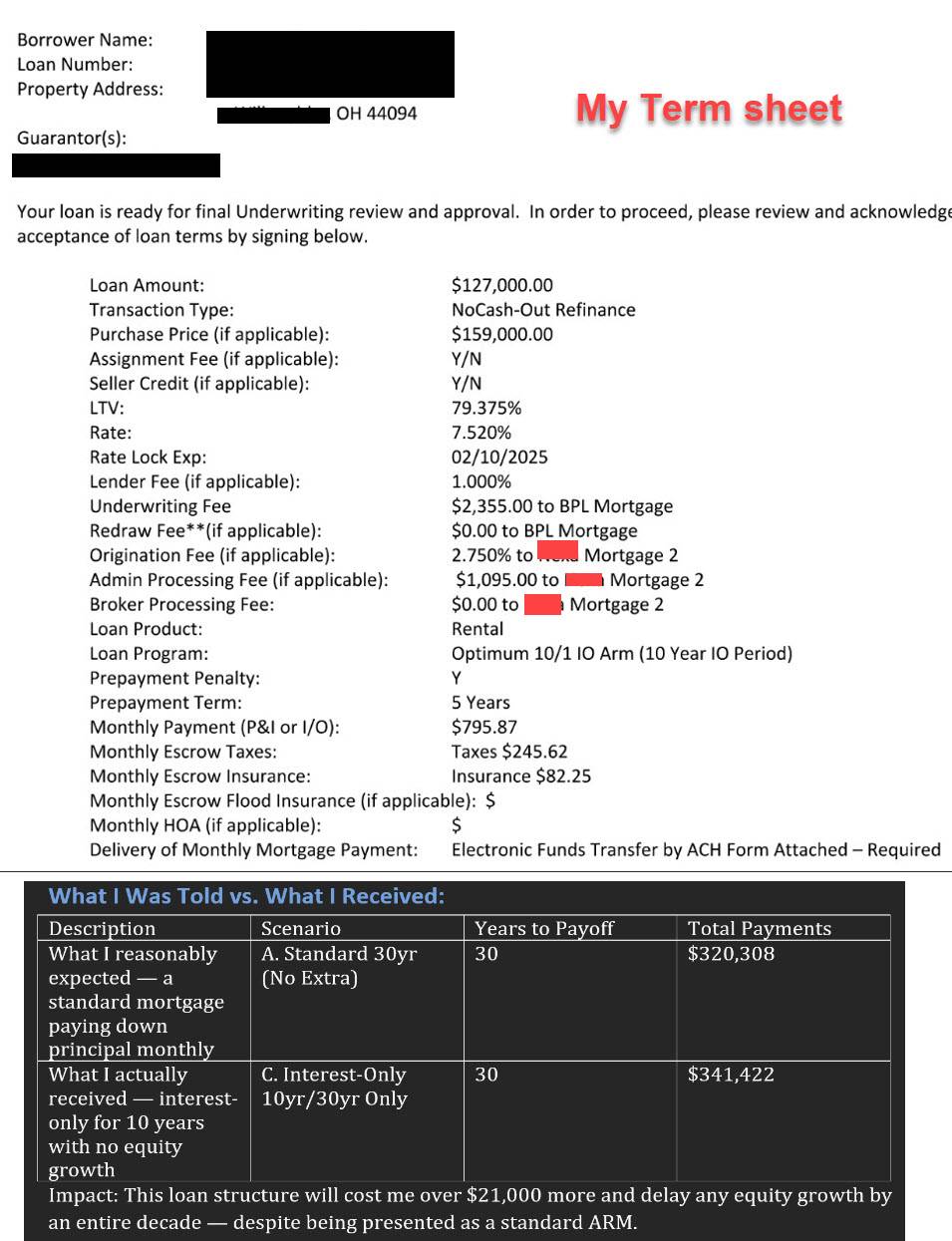

The core issue is the lender didn’t disclose the IO feature on the Term Sheet. I’m looking for practical advice on how to resolve this—whether it’s pushing the lender to amend the structure or negotiating a modification—so I can get the loan I thought I was signing. Any thoughts?

Post: When an ARM Isn’t What It Seems: $21,000 Surprise in My 10/30-Year Interest-Only Loan

- Posts 6

- Votes 0

I recently discovered that the "10/30-year ARM" I enthusiastically signed was actually a 10-year interest-only loan—nothing I paid went toward principal for a full decade. After five months of $795/mo payments, my balance remains untouched, and I now face $21,000 in excess interest compared to a standard 30-year mortgage. The Term Sheet I signed never mentioned this IO feature in plain English, and my broker’s assurances were limited to “10-year ARM” jargon.

I’m seeking insights on:

-

Disclosure best practices: How can lenders ensure borrowers truly understand ARM vs. interest-only?

-

Remedies and recourse: What steps can a borrower take when industry terms are buried in fine print? I am looking for advice here.

-

Your experience and advice would be invaluable—both to correct my situation and to help raise the bar for transparency in ARM lending.

See the agreed upon Term sheet below.

Please share what I can do. Thanks Andrew

Post: Water bill went up super high

- Posts 6

- Votes 0

I have a 4 unit. I am replacing all 4 toilets. My Property manager wanted to change the internals. With new units I will save water and remove the larger older tanks.

Installing Power Flush by Glacier Bay from Home Depot at $139 each, They have less chance of getting clogged.