Updated 3 months ago on . Most recent reply

When an ARM Isn’t What It Seems: $21,000 Surprise in My 10/30-Year Interest-Only Loan

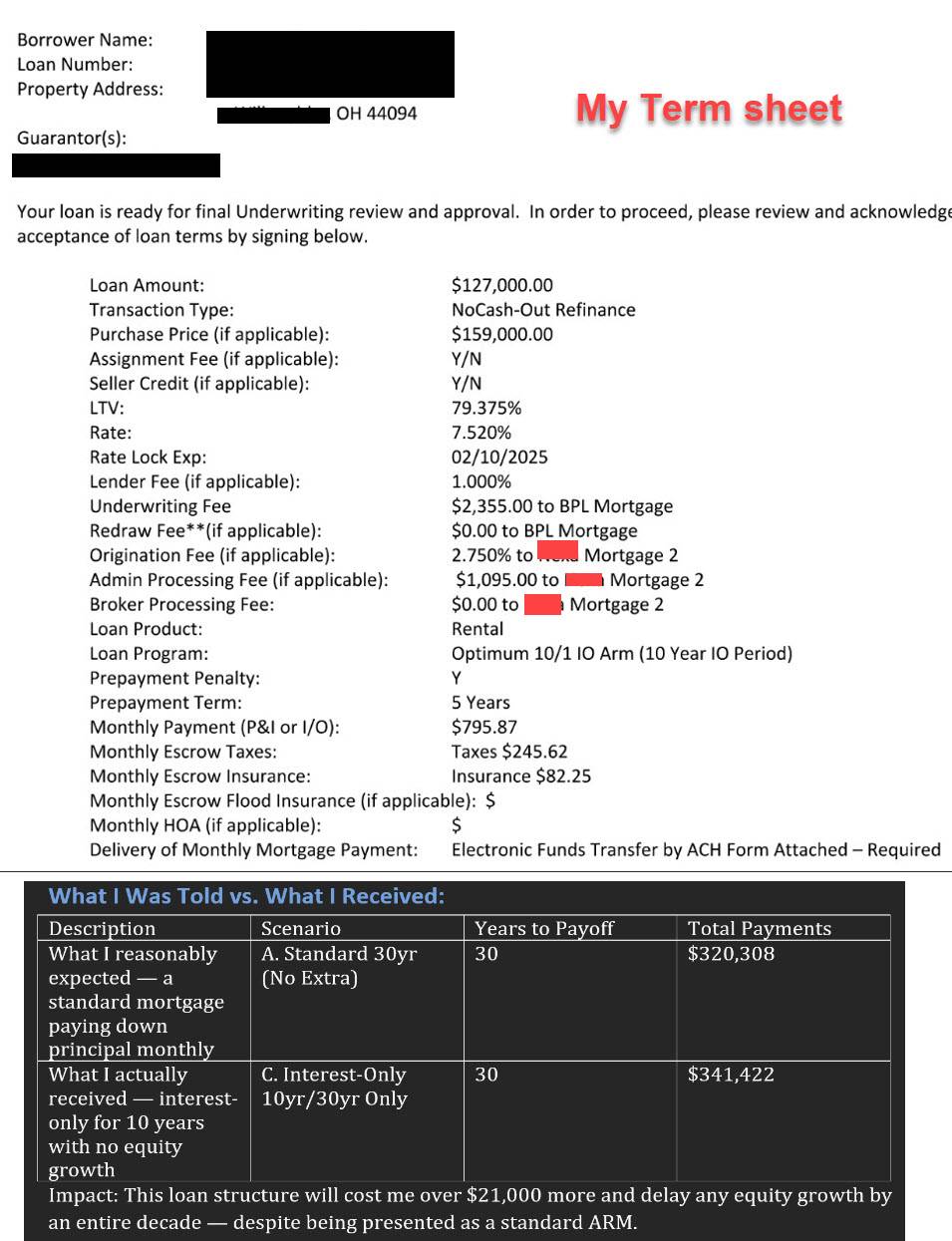

I recently discovered that the "10/30-year ARM" I enthusiastically signed was actually a 10-year interest-only loan—nothing I paid went toward principal for a full decade. After five months of $795/mo payments, my balance remains untouched, and I now face $21,000 in excess interest compared to a standard 30-year mortgage. The Term Sheet I signed never mentioned this IO feature in plain English, and my broker’s assurances were limited to “10-year ARM” jargon.

I’m seeking insights on:

-

Disclosure best practices: How can lenders ensure borrowers truly understand ARM vs. interest-only?

-

Remedies and recourse: What steps can a borrower take when industry terms are buried in fine print? I am looking for advice here.

-

Your experience and advice would be invaluable—both to correct my situation and to help raise the bar for transparency in ARM lending.

See the agreed upon Term sheet below.

Please share what I can do. Thanks Andrew

Most Popular Reply

- Lender

- Charleston, SC

- 974

- Votes |

- 1,152

- Posts

- Lender

- Charleston, SC

This is no one's fault but your own. You failed to obtain clarity, you failed to read the term sheet, and you failed to double check the math and figures. The term sheet clearly shows this is an interest only program.

If you were buying a house for $200k and then got told to wire $400k to the closing attorney, would you blindly do so? Or would you question that? Youre paying less than $800/month on a loan of $127,000. This alone shouldve set off some alarms that something was off.

People like you are the reason we have out of control, excessive regulation and increased deadweight compliance costs that just make lending more expensive for everyone. Rather than accepting accountability for your own underperformance, your reaction is to come here and start preaching about how lenders should have to do more to protect idiots from themselves, which implies more regulation. How about a law that says would-be investors have to get licensed and pass a test before buying investment properties or getting investment loans. Then they would be prepared to read term sheets and do basic investment calculations and would prevent them from doing something they dont understand.

The reality is that all you have to do is take your loan terms and plug them into one of the million-plus online loan amortization calculators to tell you how much extra to pay towards principal each month in addition to the interest only payment. Then, magically, your loan will payoff in exactly 30 years in the fashion you expect with the amount of total interest you expect. Spoiler alert - your monthly payment will increase, and the total monthly payment will be exactly the same amount as if you had gotten an equal-payment, 30yr amortizing loan with a rate of 7.5% and a loan amount of $127,000.

People like you are why we have all of the RESPA/TRID/Dodd Frank garbage in the first place.

It also wouldnt surprise me if this is some clickbait spam post. The corpus of the post is clearly AI.

- Patrick Roberts