All Forum Posts by: Brittany Minocchi

Brittany Minocchi has started 9 posts and replied 960 times.

Post: New RE investor in canton

Post: New RE investor in canton

- Lender

- Massillon, OH

- Posts 996

- Votes 479

Hey Yiftach -

I'm local to the area and could give you a few names of agents that work with investors. If you need any direction with financing, I can assist with that as well. Feel free to connect!

Post: Financing options for a BRRRR + STR?

- Lender

- Massillon, OH

- Posts 996

- Votes 479

Quote from @Yvonne Wang:

Quote from @Brittany Minocchi:

Quote from @Sebastian Bennett:

@Brittany Minocchi Just to be clear the 12 month seasoning you mention is a Barrett Financial underwriting requirement, correct?

@Yvonne Wang Use this website to cross check for zoning and whether the permitting is in place.

http://atlas.phila.gov It's a good website with accurate reporting. I recently learned even the MLS can be slow to update and doesn't necessarily reflect the most up to date zoning.

No - it is a requirement for ALL conventional loans backed by Freddie/Fannie regardless of which lender you obtain the loan through.

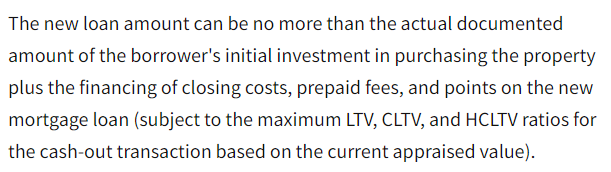

@Brittany Minocchi thanks for the clarification. I read the Fannie seller guide and it says that a cash out refinance has a 12-month seasoning requirement if it is paying off an existing first mortgage: "If an existing first mortgage is being paid off through the transaction, it must be at least 12 months old at the time of refinance, as measured by the note date of the existing loan to the note date of the new loan." But I interpreted this seasoning requirement to not apply if there's no first mortgage on the property (initial purchase was all cash). https://selling-guide.fanniemae.com/sel/b2-1.3-03/cash-out-r... But you are saying even if there's no mortgage on the property / it was bought with cash initially any cash out refinance using Fannie/Freddie loans still require a 12 month seasoning period? Do you mind pointing me to where this requirement is in the selling guide?

You are correct that the 12 month period applies if there is currently a mortgage on the property. However, if you are refinancing a property purchased with cash within 6 months of purchase, this is considered delayed financing. A cash out refinance and delayed financing are not exactly the same thing. While there isn't necessarily a 12 month seasoning requirement to refinance in this instance, your loan amount will be limited to the original purchase price + closing costs/fees/points if you refinance before the 12 month seasoning period has passed. So to clarify, the 12 month seasoning applies if you want to use the appraised value of the property. If you only want to pull your initial investment, then this would work. Most people who are completing rehab want to pull based on the value they have added to the property. See below for a snippet from the Selling Guide.

Post: New Investor Looking for Advice

- Lender

- Massillon, OH

- Posts 996

- Votes 479

Hey Alison -

You don't typically need proof of income for a fix and flip loan, they are more asset-based. However, depending on the property, you may have trouble getting financing as a beginner and may need to bring someone else in on the deal with you. As others have mentioned, it may make more sense to start with a house hack or at least a turn-key rental instead of a flip.

Post: New investor from Ohio

- Lender

- Massillon, OH

- Posts 996

- Votes 479

Whats up Bryson!

I'm also in Ohio. I've worked with many folks who choose to house-hack as their first step into the investing world, and that's what I'd suggest to you. Buy a duplex, live in one side, rent out the other, and use that rent to cover a chunk of your mortgage. When you're ready, you can move into a new place and rent out the unit you were living in. Doing it this way allows you to ease your way in and costs you less up front - down payment for an owner-occupied property is much lower than an investment property, you may qualify for down payment assistance and can even use funds as a gift from a family member if that's an option.

Post: Want to use primary residence to start my investment journey

- Lender

- Massillon, OH

- Posts 996

- Votes 479

Lots of people use the equity in their homes to buy an investment property. You're putting the roof over your head on the line if anything falls through, so of course there is some risk with that option. I typically advice a cash out refi over a HELOC if you have an immediate use for the funds since HELOCs have variable interest rates, but you also want to take your current interest rate into consideration. Happy to connect, feel free to reach out.

Post: Advice and guidance

- Lender

- Massillon, OH

- Posts 996

- Votes 479

Hey Michael -

Not all lenders have the same requirements when it comes to DTI, some have what's called an overlay. This is a requirement a lender places on top of what Fannie/Freddit/HUD etc require. Did any of them tell you what they're calculating for your DTI currently? Have they pulled credit? Happy to discuss if you'd like to connect.

Post: What are lenders you know of that do cash-out refinances on 100k rental properties?

- Lender

- Massillon, OH

- Posts 996

- Votes 479

Hey Jose -

This is definitely doable. If you've owned it for at least a year, you can go the conventional route or something like a DSCR loan. Depends on whether you can qualify by supplying docs like W2s, paystubs, etc. and if you want to close in your name or an LLC. Feel free to reach out, I'd be happy discuss these options.

Post: Need Advice on Financing a new purchase

- Lender

- Massillon, OH

- Posts 996

- Votes 479

As far as the pricing goes, this isn't terrible. I priced your scenario out as a DSCR loan at 75% LTV with excellent credit and am very close to what you posted, slightly cheaper cost in points. Keep in mind that these are with 1 year prepayment penalties. I typically recommend 3 years to keep pricing more favorable but also not lock yourself in longer than necessary. The penalty will trigger upon sale OR refinance. Some lenders call DSCR loans (or other nonQM programs) conventional loans, but the fact that you have a prepayment penalty tells me it's not a Fannie/Freddie conventional loan - they don't allow them. If you can qualify by supplying W2s, paystubs, etc. your rate and/or cost in points may be lower and you will not have a prepayment penalty.

How much to put down depends on how much cash you will have in reserves and what your cash flow preference/tolerance is. With this being your first investment, you want to make sure you have enough held back to cover anything that pops up. We don't know when or if rates will drop any time soon, so it may be worth exploring the 2 and 3 year prepayment penalty options and compare the pricing there. It will lower your rate and help you cash flow a bit more, and if rates do come down after that period is up, then you can look at refinancing.

Post: Loans and llcs

- Lender

- Massillon, OH

- Posts 996

- Votes 479

Hey Reyna -

It sounds like you're planning to occupy a unit in order to qualify for 3% down, correct? If so, you'd need to go with conventional financing and unfortunately are unable to close in an LLC with that type of loan. This goes for FHA, USDA and VA as well. You can close in an LLC with a DSCR loan, but DSCR would not be an option if you plan to occupy since it's a business purpose loan - you'd have to rent out both units.

Post: Email template for Out of State Mortgage Lender

- Lender

- Massillon, OH

- Posts 996

- Votes 479

If you're looking to use conventional financing, whoever you work with will need to be licensed in the state you're buying in. If you use a DSCR loan like some others have mentioned, licensing works differently since that's a business purpose loan. Those of us (loan officers) that do DSCRs are very familiar with working with people from all over (and outside of) the US. No need for an e-mail template :) I hope that helps, feel free to reach out if you have any questions.