All Forum Posts by: Luka Milicevic

Luka Milicevic has started 50 posts and replied 2564 times.

Post: Need help Analyzing a duplex

Post: Need help Analyzing a duplex

- Real Estate Agent

- Nashville, TN

- Posts 2,658

- Votes 2,195

Quote from @Chris Fatur:

Buying my third property in Sacramento where I invest, I'm purchasing a duplex and kinda just got lucky with my first two deals, what's the most important numbers to pay attention to when Analyzing a deal, my main thing i need is a general percentage for expense aside from mortgage and property management... vacancy and maintenance ect. Thanks for the help! Also is there anyone out there that thinks Sacramento is a good or bad market ?

Hey Chris,

The most important numbers in a deal - if you ask 10 people on this forum that question you will get 11 different answers. It's very personal and situation dependent.

If you're looking to live off your RE income today then cash flow is the most important number. If you're looking to build equity then purchase price vs appraised value. If you're looking for highest ROI then lowest down payment might be the most important number!

It just really depends!

Sacramento is in California and everything in California is bad. Invest out of state where you can actually have control over your property and not live under the crushing weight of red tape.

Post: Possible STR potential

- Real Estate Agent

- Nashville, TN

- Posts 2,658

- Votes 2,195

Quote from @Ajay Singh:

Hey everyone, I’ve been thinking about setting up a unique Airbnb in a more secluded spot and possibly renovating a property to make it stand out. I’m still in the early planning stage and trying to learn as much as I can.

If anyone here has experience with short-term rentals, knows of mentors or people who’ve done something similar, or has advice on how to make an Airbnb really stand out for nature lovers, I’d love to connect. Also open to tips on how to figure out if a location is a good fit and how to run the numbers properly. Im a canadain looking to invest in whistler , washington state, or nashville Tennessee.Thanks!

These are some of the highest ROI STRs that you can get. You will be best served on the outskirts of Nashville as city limits will have more restrictions on this sort of project and also less of the vibe you're trying to achieve.

I'm in the Middle TN area reach out if you have questions.

Post: Leasing & AirBnB

- Real Estate Agent

- Nashville, TN

- Posts 2,658

- Votes 2,195

Quote from @Elio J. DiTrento:

A friend of mine came across this property called "The Burnham" in Nashville TN.

it seems like you Lease it and they let you air bnb it.

Looks like they take. 25% fee.

Seems to be a pretty busy place and a lot of people stay there.

Does anyone know about this place or places like this?

STR arbitrage.

Depends what you make of it, depends what they charge on the rent.

Post: subdividing and flipping with investor help?

- Real Estate Agent

- Nashville, TN

- Posts 2,658

- Votes 2,195

Quote from @Jason Braddock:

I have been trying to figure out what to do in my current situation to get the most return on my current house if I decide to sell it. In my neighborhood the lots are decent sized and developers have started coming in and tearing down older homes and subdividing into 2 properties then building 2-3 story "tall and skinnies." My current house that was built in the 1950's in current condition would get around $575k; if we put some money into rehabbing the house we could get around 700k; but these tall and skinnies are selling for 1.2M to 1.5M each meaning potentially $2-3M in revenue. So my question is this: would approaching a developer be an option for a better selling outcome? With a HELOC and savings I potentially have around $300k to access for funds going into a deal.

Your best option is to reach out to me, partner on the project, we build both units and we sell. That's the highest outcome for you.

Or....you decide to keep one house when they are done as a primary, STR the other side using Nashville's HPR STR allowance

Or....you keep one house and just sell the other making your base in the other house super low.

So many exit strategies on an R lot

Post: Anyone here in Canada? Investing in US Multifamily Real Estate

- Real Estate Agent

- Nashville, TN

- Posts 2,658

- Votes 2,195

Quote from @Adam Chung:

My partner and I run 5 Airbnbs in Dallas and 1 in Nashville. We’re now diving into research on which U.S. markets are best for an AirbnbRRR strategy. Since you’re also a Canadian looking at U.S. investing, I’d love to connect!

Well, what has your research come up with? What markets are best?

Post: Southwest Airlines starts serving the Smokies in Spring 2026

- Real Estate Agent

- Nashville, TN

- Posts 2,658

- Votes 2,195

Quote from @Jay Hinrichs:

Hey now....some of us are big on SW! I honestly stopped looking at other airlines. SW was just by far and wide the best experience I have had on an airline and the most cost effective. No assigned seat never bothered me.

Post: Independent Land Scouts Wanted – $1,500–$2,450 Per Parcel (Middle TN)

- Real Estate Agent

- Nashville, TN

- Posts 2,658

- Votes 2,195

A bunch on the MLS right now that meet these criteria

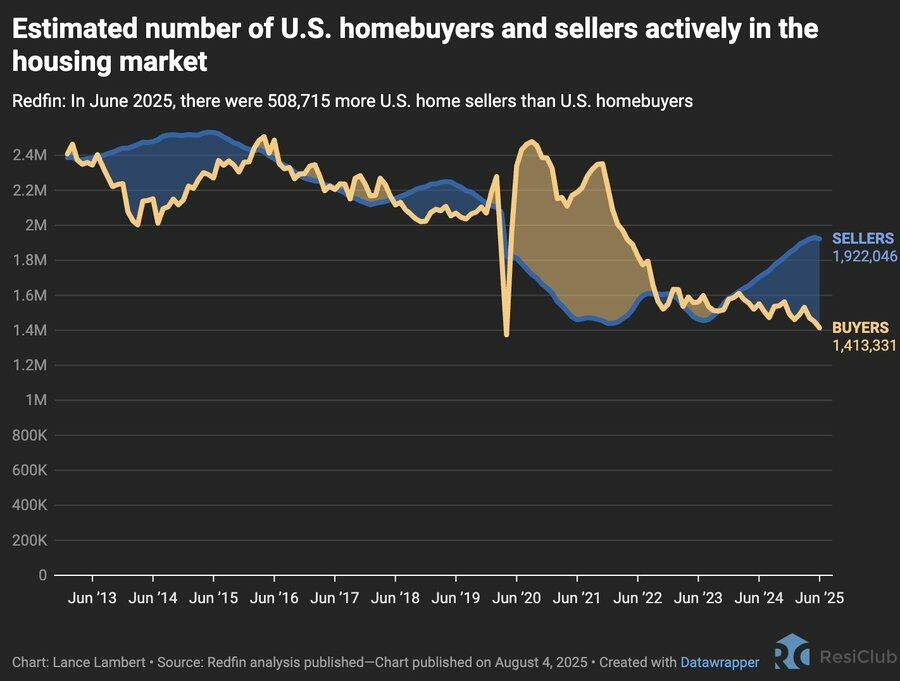

Post: Home-Sellers Outnumber Home-Buyers By The Most In Over A Decade - Is It Good or Bad?

- Real Estate Agent

- Nashville, TN

- Posts 2,658

- Votes 2,195

Quote from @Ken M.:

Why aren't you out there buying a house? I just bought 3 below list. It can be done!

************************************************************************

Home-Sellers Outnumber Home-Buyers By The Most In Over A Decade by Tyler DurdenLance Lambert, co-founder and editor of ResiClub, posted on X, highlighting an ongoing and record-breaking trend in the housing market: sellers now outnumber buyers by the widest margin since Redfin data began well over a decade ago. The growing number of sellers is especially evident in the U.S. Southwest and U.S. Southeast, particularly in Texas and Florida, where the balance of power has shifted in favor of buyers.

There are an estimated 1.92 million home sellers in the U.S. housing market and about 1.41 million homebuyers. In other words, there are 508,715 more home sellers than buyers, a massive mismatch not seen at any other point in Redfin data going back to 2013.

https://www.zerohedge.com/markets/home-sellers-outnumber-hom...

Much of the supply is materializing in Sun Belt metro areas, such as Austin, Dallas, Tampa, and Nashville. Inversely, Northeast and Midwest metros like Chicago, Hartford, and Boston have seen tight supplies.

It can very much be felt in the market. Gosh it feels good to have options again!

Post: Fix and flip projects

- Real Estate Agent

- Nashville, TN

- Posts 2,658

- Votes 2,195

Quote from @Crystal Redmon:

Hello, my name is Crystal Redmon. I am just starting out on the fix and flip what anybody like to give me any information that would help me along the way would be greatly appreciated. Thank you.

What kind of info are you looking for? How big of a reno is this going to be?

Post: Off-market and on-market real estate opportunities

- Real Estate Agent

- Nashville, TN

- Posts 2,658

- Votes 2,195

Quote from @Colton Friday:

Hi BP Community! I am an agent in Nashville, TN. I have got some potentially exciting off-market and on-market deals that might interest investors.

I'll reach out as I want to be on your list