Personal Finance

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

Updated 14 days ago on . Most recent reply

- Tax Strategist, Financial Planner and Real Estate Investor

- Atlanta, GA

- 917

- Votes |

- 2,400

- Posts

💰 Are You Really Middle Class? Here's What the Data Says 💰

💰 Are You Really Middle Class? Here's What the Data Says 💰

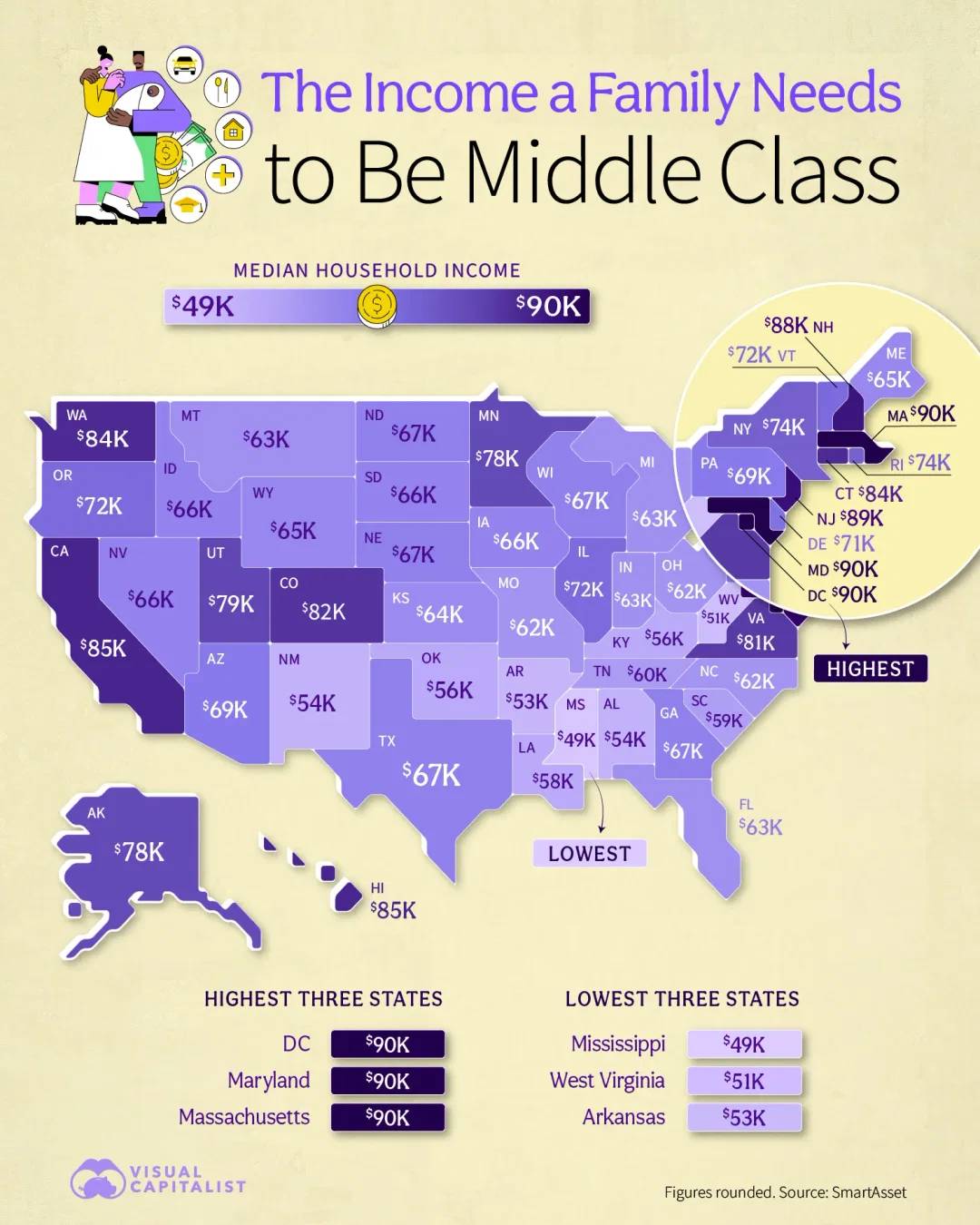

What it takes to be middle class in America varies wildly by state. According to SmartAsset, a family needs anywhere from $49K in Mississippi to $90K in D.C., Maryland, and Massachusetts to qualify. In high-cost states like California and Hawaii, the middle-class threshold is $85K+, while states like West Virginia and Arkansas sit below $55K.

As a financial planner, I urge families to benchmark their income against their state’s cost of living. Living in a high-income state without a matching financial strategy could mean falling behind—even if you earn more than others in different parts of the country.

📊 Are you on track to reach your financial goals in your state?

- Bill Hampton

- 404-482-3170

Most Popular Reply

- Investor

- Poway, CA

Average rent for a 2 br apartment in the city of San Diego is $3017. For a 3 br apartment it is $4298 (source apartment advisor). According to census San Diego median household income (which recently passed Los Angeles and is leaving it in the dust after being far below it forever) $104,321 (source census). SFH in general rent for more than apartments for Same BR count

2 BR: $3017 * 3 * 12 =$108,612.00

3 BR: $4298 * 3 * 12 =$154,728.00

This implies the median household income cannot even afford to rent the average 2 BR apartment. They are over $50k short of being able to rent the average 3 BR apartment.

Los Angeles has lower rent, but they now have significantly lower household income (when I was a young worker, Los Angeles salaries were much higher than San Diego and it was called locally as the sunshine tax). Their numbers I would guess are about the same for affording rent.

It is not good for tenants, but the property values are so high that the rents cannot be much lower (I guarantee the property owners at high LTV are typically large negative cash flow at purchase). The only way the high rents associated with high property costs benefits the landlord is it makes for higher quality tenants and with patience the rents increase while typically the mortgage is fixed. So eventually there will be positive cash flow if no value is extracted.

Note this does not seem sustainable but 1) the rents have been high in San Diego forever. In ~1990 my now wife rented a 1 br at $650/month. It seemed crazy high as minimum wage then was $3.35/hour (vs $17.25 today). 2) I suspect the rent to value is near an all time low meaning the tenant has rarely rented more value for their rent amount than now. In that respect the tenants are getting a good value 3) MF are rent controlled. Tenants once they are in a MF unit have a cap on their rent increase. They can typically stay as long as they desire with constrained rent increases.

housing in San Diego is expensive whether it is to purchase or to rent. However, it is currently noticeably initially much cheaper to rent than to purchase. Apparently we are still paying the sunshine tax but now Los Angeles is also paying a similar sunshine tax.

Southern ca is expensive. Fortunately, there are also opportunities for those with vision, willing to take appropriate risks, and work smart and hard. The average person is unable to meet all these criteria. They therefore struggle to afford to live in southern CA.

I once long ago risked virtually every somewhat liquid dollar (so not my home, 401k, job, or family) on an investment. First year cash flow was over 65% of my investment. I had the vision and took the gamble. It paid off big time and I still am getting cash flow of near 10% of our initial investment amount (in inflation adjusted dollars it is much less than 10% but we already achieved crazy returns on that investment). By the way, I told some people my rationale on the investment. Not one wanted to invest. After the opportunity had gone to a normal type opportunity (so a few years later) one of those people asked if I thought it was still a good investment. I told him that the cost was 4x what it was when I purchased (my $300k investment was worth ~$1.2m and had paid us around $600k in 3 years) and that other opportunities could probably out perform it. He was eager to invest in the opportunity only after it had produced crazy returns but by then it was priced appropriately for its expected return. That is most people. Unwilling to take calculated risks. It is why many people on BP will never buy an investment property. What is worse a bad investment or no investment? I can make a case for either. What is better a mediocre investment or no investment? I lean toward the mediocre investment. My definition of a good investment at purchase is not solely based on return. It is based on the risk adjusted return which includes best and worse case scenarios. If there is only 10% chance at a killer return (50%+) but the worse case scenario is I lose 5%, even if the worse case will happen 25% of the time, that is a good risk adjusted return.

Good luck