Updated 9 months ago on .

- Lender

- Fort Worth, TX

- 6,506

- Votes |

- 8,192

- Posts

Labor Market Calls 911

- Lender

- Fort Worth, TX

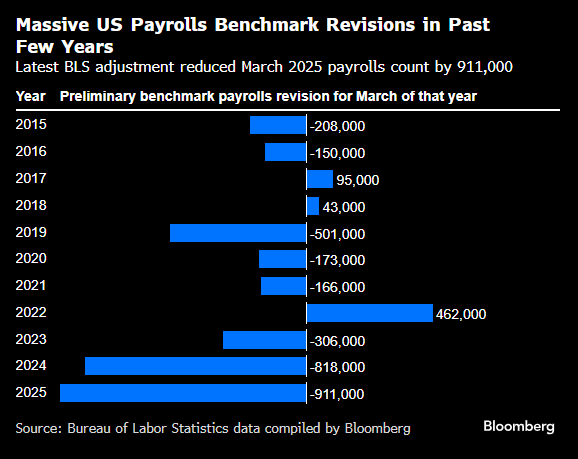

This morning’s BLS revisions delivered a shock to markets, revealing a massive 911,000 downward adjustment to payroll growth through March. The scale of the revision highlights a significantly weaker labor market than previously understood and has immediate implications for monetary policy.

The 10-year Treasury yield briefly touched 4.03%, testing major resistance at 4.00%. It has since edged slightly higher to 4.06% as markets digest the implications of the BLS data. The yield curve remains steep, with short-term yields falling on rate cut expectations, while longer-term yields are sticky due to inflation and fiscal concerns.

Gold surged to a record high of $3,650/oz, up over $3,700 year-to-date. The rally is driven by expectations of Fed rate cuts, falling real yields, and global demand for safe-haven assets amid trade and fiscal instability.

Slower employment growth and the BLS revisions solidify the case for a September rate cut. Markets are now pricing in a near-certain 25bps cut at the upcoming FOMC meeting. The Fed is likely to interpret the labor market deterioration as a signal to begin a string of cuts, barring an extremely low CPI print on Thursday.

Forecasting bond performance remains challenging amid persistent macro uncertainty, unresolved tariff impacts, and key inflation data still to come. Investors are increasingly favoring the front end of the curve and high-quality credit, as longer-duration Treasuries may struggle in this environment. Mortgage pricing, therefore, isn’t on a one-way path lower—since Friday’s payroll-induced bond rally, we’ve seen broad repricing of both risk and duration across the industry.

Servicing valuations have dropped meaningfully, as portfolio managers brace for a potential wave of payoffs driven by refinancing activity. Credit spreads, particularly in non-agency sectors like Jumbo and NQM, are widening as investors reassess the implications of a weakening labor market. Mortgages are currently down 3 ticks on the day. With rates testing the lower end of the recent trading range (4.0% on the 10-year) and origination supply picking up, the market faces stiff resistance to rally further from here without a jolt from softer inflation.