All Forum Posts by: Andrew Postell

Andrew Postell has started 95 posts and replied 7700 times.

Post: Part investment and primary question in regards to a lender

Post: Part investment and primary question in regards to a lender

- Lender

- Fort Worth, TX

- Posts 8,037

- Votes 6,401

Quote from @Ruth Schrader-Grace:

Quote from @Andrew Postell:

@Ruth Schrader-Grace there are loans that will not hold your departing residence against your "debt to income" ratio. Meaning, you can buy another primary home without the other home holding you up. Not every lender has them but they do exist.

Andrew-Shy of a bridge loan there doesn't seem to be but appreciate the thought. But I will keep looking for a solution. Thank you.

@Ruth Schrader-Grace these absolutely exist. We write them. Not bridge loans. 30 year fixed loans that won't hold your primary against you. It's a different loan, so not a lot of lenders have them.

Post: How are investors structuring deals when they have great credit but limited cash?

- Lender

- Fort Worth, TX

- Posts 8,037

- Votes 6,401

@Camren Berry this is the problem and the BRRRR Method solves. That's the whole point it exists. I mean, it's also the point of "Subject To", "Loan Assumptions", "Owner Financing", etc. NONE of us have unlimited money. Even if you have $1million....your limit is just higher than mine - you still have a limit!

I started out with $4,000. I have 15 properties now. And I'm nothing. There's PLENTY of examples of people who have done much better than me. There's also more examples of people who didn't do it well. Since you are posting this in the BRRR Method forum...I'm assuming you might be interested in this technique? Maybe?

Here's some tips:

BRRRR SKILLS NEEDED

Generally speaking you will need several things to successfully complete a BRRRR:

- ARV - being able to calculate the Value on your own (meaning, without the wholesaler telling you the value) is really important.

- Repairs - You will likely need to know how to budget the repairs as well. Getting a contractor can be extremely frustrating especially if you need to make an offer without even looking at the property. How do you calculate repairs without a contractor? You may need to lean on other local real estate investors in the beginning. Or maybe even just focus on properties with a very light rehab?

- Lenders - You will need a lender on your BUY step and on your REFINANCE step. And I would HIGHLY recommend to read this article I wrote for Bigger Pockets on how to find good lenders that you can find HERE. If they are good, they should be absolutely definitive on rate, terms, costs, etc. Trust me, many lenders will tell you they can do this...but it's very rare to find. When I first started BRRRR'ing my properties lenders would tell me "That's illegal"....it's not, they just didn't know anything about it.

- Finding Properties - and this is the absolute hardest step of anything right now. So network like crazy and find some good resources. It's going to be hard...but if it were easy then anyone could do it.

Some notes on the 2 most critical steps to me:

- How to calculate After Repair Value (ARV)

- How to calculate Rehab Costs

And it's not so easy to understand. People spend HOURS of training on this subject and there are plenty of horror stories of people who purchased homes...and didn't do ANY math before they bought. So at least you are trying and you will get better at it.

So, how can you get better at estimating ARV? Treat this like college. It takes some people 4 years to get through college (and sometimes longer) so we aren't going to take just 1 class and call ourselves experts. We need to take multiple "classes" and become the SMARTEST person on this subject. Here's some ideas:

- Lean on your Lender - a good lender can show you how to estimate ARV.

- Lean on your Appraiser - ask your appraisers what they did. Maybe even ask them if there's any training they could suggest for you.

- Lean on your Title Company - Title companies will often give free training, designed for real estate agents, on this subject. Ask if they have anything coming up...if they don't, ask them to host one!

- Lean on your local Real Estate club - I don't know if you have any close to you but I lean HEAVILY on my REI clubs for this. They often will have sessions on this subject.

- Bigger Pockets? - Do they have any tools? They have an entire forum on this subject. Maybe ask this same question in there?

- YouTube? - It's got everything else, why not this?

- And ASK - What's the impact of a pool? Windows? Bathrooms? Granite vs. Laminate? Where do I get the most bang for my buck?

How can you get good at estimating your renovation costs? - This one is going to be a little harder to do. I actually had a contractor provide me with his renovation calculator. I met this contractor at a REI club...because he was teaching a class on how to calculate renovations! Get with people who are smarter than you to make you smarter too.

Again, we need to get smarter than smart on this subject. This is money. YOUR money. Get out there and get better. You can do this and maybe one day you can even be teaching one of those classes. Who knows?

Post: Rates Slide as Global and Domestic Pressures Mount

- Lender

- Fort Worth, TX

- Posts 8,037

- Votes 6,401

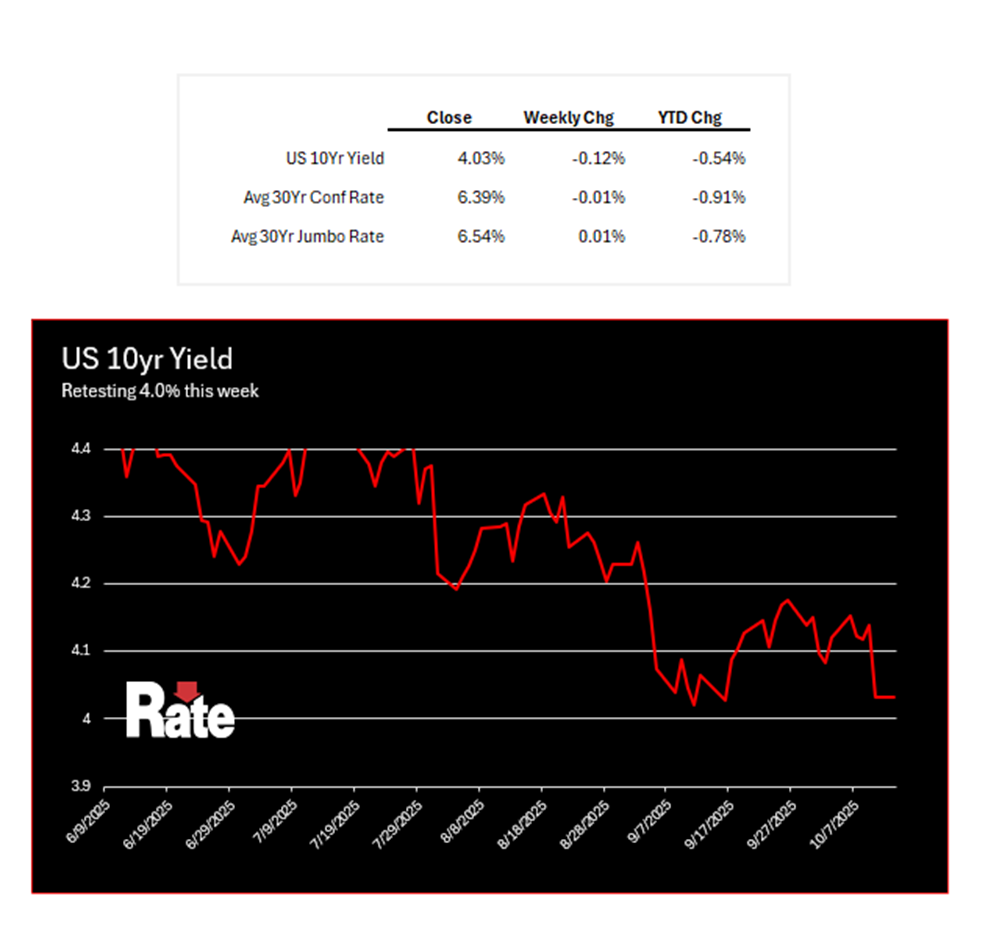

Interest rates are trending lower across the board. The average 30-year fixed mortgage rate is now approaching 6.25%, while the 10-year Treasury yield has dipped to 4.02%—a notable decline driven by a flight to safety and weakening economic signals. Market sentiment has shifted decisively toward lower rates, with investors responding to a combination of geopolitical relief and renewed global uncertainty. The Israel-Hamas ceasefire, brokered by the U.S., has helped stabilize risk sentiment, while the re-escalation of the U.S.-China trade war—marked by a 100% tariff on all Chinese imports effective November 1—has triggered a sharp selloff in equities and crypto, reinforcing demand for bonds. The S&P 500 fell 2.71% on Friday, underscoring the market’s pivot toward defensive positioning.

Fed Outlook: Easing Bias Grows as Data Goes Dark

The Federal Reserve’s October meeting (Oct. 28–29) is now shrouded in uncertainty. With the government shutdown delaying key economic reports like CPI and Nonfarm Payrolls, policymakers are operating with limited visibility. The September FOMC minutes revealed a divided committee, but the recent drop in yields and softening private-sector data have tilted expectations toward another 25 basis point cut. The federal funds target range currently sits at 4.00%–4.25%, and markets are increasingly pricing in further easing. Fed officials remain cautious, but the lack of fresh data and rising global risks are making a stronger case for preemptive action. Bond yields have responded accordingly, holding near recent lows as traders brace for dovish signals.

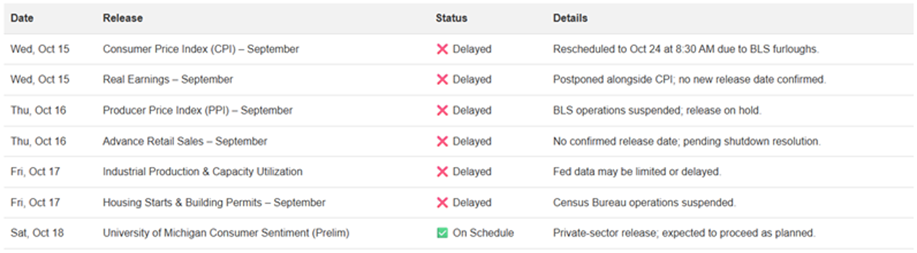

Government Shutdown: Data Drought Fuels Rate Decline

Now entering its third week, the federal government shutdown has paralyzed the release of critical economic data. The September CPI report has been postponed, and the jobs report remains unscheduled. This data blackout has left markets and the Fed flying blind, amplifying the impact of private-sector indicators like ADP's weak employment numbers. The result: a muted but persistent downward drift in rates. Agencies like the IRS and FHA are operating at reduced capacity, but core mortgage operations remain functional. With no clear end in sight, the shutdown is reinforcing the market's dovish bias and delaying any potential tightening moves from the Fed. Until the data resumes, expect rates to remain under pressure.

Key Economic Data Releases this Week:

WEEKLY INTEREST RATE SNAPSHOT (this is for primary homes, which is what the majority of retail lenders and news outlets promote/advertise

Post: Reliable Contractor for out of state Investors

- Lender

- Fort Worth, TX

- Posts 8,037

- Votes 6,401

@Maxwell Wuensch Bigger Pockets is a nationwide site. It might be more appropriate for you to say this in the guy's google reviews or post it in several Facebook REI Group pages for that market. That would give him the most exposure.

Post: What’s Your Go-To Strategy for Funding Deals Fast?

- Lender

- Fort Worth, TX

- Posts 8,037

- Votes 6,401

@Kelly Schroeder when it comes to closing quickly I always use private/hard money and the best lenders come from local lenders in the market. Ok, maybe not EVERY time...but 99% of the time, the more local the better. And I'm guessing you are referring to "off market" properties in a state of disrepair? If it's on the MLS and it's someone's primary home - that's different. But if I'm using the BRRRR Method or targeting homes that cannot be sold on the MLS - then I need "alternative" financing to execute on those properties. And yes, private money and hard money is usually the ONLY option for those types of properties - especially if they have to close in less than 7 days (which commonly happens).

So, how do you find those lenders? This is a super important question and it doesn't just apply to lenders. How do you know that a contractor is any good? An electrician? A title company? Anything? Even if they do have 20 years experience...how do you know really? And while nothing is foolproof the most consistent method of finding good vendors is relying on OTHER real estate investors that have worked with those vendors. This is why we network with other real estate investors - kind of like what you are doing here!

You do have a "lender" link at the top of Bigger Pockets here...and maybe that might lead you to some good lenders but I would still recommend networking with investors, in your market, who have used other lenders and have firsthand knowledge of how they operate. So, let's try some local real estate meetup groups. Meetup.com is a good resource for those but some of the groups will also post here on Bigger Pockets Marketplace too. Even facebook might have some good local groups for you. Some of those facebook groups have thousands of members. The priority is consistent recommendations from active investors. Oh, eventbrite too. But post locally for this. That’s the best bet.

Post: Part investment and primary question in regards to a lender

- Lender

- Fort Worth, TX

- Posts 8,037

- Votes 6,401

@Ruth Schrader-Grace there are loans that will not hold your departing residence against your "debt to income" ratio. Meaning, you can buy another primary home without the other home holding you up. Not every lender has them but they do exist.

Post: Re-finance a rental with a relative in it

- Lender

- Fort Worth, TX

- Posts 8,037

- Votes 6,401

@Spencer Cox the short answer here is that yes, you can refinance with a relative with some lenders. I can't tell which state your property is in but there is likely a lender in that state that can help. This is one of the reasons why we need multiple venders with what we do. So, let's do the local thing.

Going local is super important and it doesn't just apply to lenders. How do you know that a contractor is any good? An electrician? A title company? Anything? Even if they do have 20 years experience...how do you know really? And while nothing is foolproof the most consistent method of finding good vendors is relying on OTHER real estate investors that have worked with those vendors. This is why we network with other real estate investors - kind of like what you are doing here!

So, let's try some local real estate meetup groups. Meetup.com is a good resource for those but some of the groups will also post here on Bigger Pockets Marketplace too. Even facebook might have some good local groups for you. Some of those facebook groups have thousands of members. The priority is consistent recommendations from active investors. Oh, eventbrite too. But post locally for this. That’s the best bet.

Post: BRRRR Partner Needed – Kankakee, IL – Free & Clear Property

- Lender

- Fort Worth, TX

- Posts 8,037

- Votes 6,401

@Tawone Autman thanks for the post and welcome to Texas! Now, as a 15 year, out-of-state investor my recommendation is to ALWAYS use people who are referred to you. Keep in mind that you may never see your asset. That's an ENOURMOUS amount of trust/money to put into a stranger's hands. One wrong move, one wrong contractor, one wrong vendor…will erase your profits. Your network is the most important piece for any potential returns when you invest out of state.

So, how do you find a good reference? This is a super important question and it doesn't just apply to partners. How do you know that a contractor is any good? An electrician? A title company? Anything? Even if they do have 20 years experience...how do you know really? And while nothing is foolproof the most consistent method of finding good vendors is relying on OTHER real estate investors that have worked with those vendors. This is why we network with other real estate investors - kind of like what you are doing here!

So, let's try some local real estate meetup groups on facebook. There are several Illinois and some have THOUSANDS of members. The priority is consistent recommendations from active investors. Interview, get references, and trust no one! Just kidding about that last one...but you know what I mean. This is your money, so be diligent with it.

Thanks!

Post: Refinance Help Commercial Multi-Family

- Lender

- Fort Worth, TX

- Posts 8,037

- Votes 6,401

@Adam Danes in case someone else is searching for this I wanted to provide some additional details.

Usually, we do not BRRRR Commercial properties. Residential properties are 1-4 unit properties. Anything 5+ would be considered commercial in nature. The BRRRR Method is designed for residential properties because financing is so different in the commercial space.

When we "flip" a residential property, we can fix it, and list it immediately for sale. Mainly because our potential buyer can buy a single family home right away (there are some exceptions even to this though). A flip in the commercial space (5+ units) might be a 4 year process. This is because the financing on a multi-family unit property might need 2 years of the improved rent roll to get financing. Warehouses, gas stations, etc, in the commercial world usually have the same types of restrictions. So, doing a BRRRR Method in the 5+ unit space might take 3+ years! Because the financing might need 2 years of rent rolls.

There is some gray area in the 5-10 unit space. I do know a great DSCR lender that can go up to 60 units. That's pretty rare...but they don't lend in the entire state of Ohio! Crazy, right? Again, lending in the 5+ unit space gets really different in a hurry. So, if we do find a good property, I need to identify my exit lender before I execute.

Going Local - as mentioned above, going local is really important for our strategy. And this is a super important strategy that doesn't just apply to lenders. How do you know that a contractor is any good? An electrician? A title company? Anything? Even if they do have 20 years experience...how do you know really? And while nothing is foolproof, the most consistent method of finding good vendors is relying on OTHER real estate investors that have worked with those vendors. This is why we network with other real estate investors - kind of like what you are doing here!

So, let's try some local real estate meetup groups. Meetup.com is a good resource for those but some of the groups will also post here on Bigger Pockets Marketplace too. Even facebook might have some good local groups for you. Some of those facebook groups have thousands of members. The priority is consistent recommendations from active investors. Oh, eventbrite too. But let's get connected in these local groups, ask the question of who people are working with, and that should get you in a better direction. Oh, and while I respect how anybody markets...we need another INVESTOR to recommend someone. That's what we are looking for. So, if someone states "I can do it"....maybe they can and maybe they can't. But if another investor says, "I worked with X company and here's the person I used there" - that's what we want.

Hope all of that makes sense.

Post: 1st BRRRR Deal. Unfinished Basement.

- Lender

- Fort Worth, TX

- Posts 8,037

- Votes 6,401

@Matthew Sevilla I read the posts above but the right answer here is "What do your comps say?". So, if none of your comps have granite countertops....then adding granite countertops may not add any value at all. You know the phrase "Don't over improve a property"...this is where your comps are critically important. Yes, it is possible that some of the things listed above would help with value...but not if there aren't any comps. Hope this makes sense how I am describing it.