Updated about 1 month ago on . Most recent reply

- Investor

- Zero Down Specialist

- 1,034

- Votes |

- 1,833

- Posts

Buying Using Subject To vs Using A Bank - How Do They Compare - Actual Deal

- Investor

- Zero Down Specialist

For starters, you run out of money using a bank to finance and you pay huge fees for the "privilege" of using their money. You can avoid all of that by knowing how. This can be done in CA, FL, AZ, TX you name it, ANYWHERE. It varies a little bit in each location, but it's a great advantage to serious investors. You can rent out the property, you can "fix and flip", you can STR, all with or without a LLC.

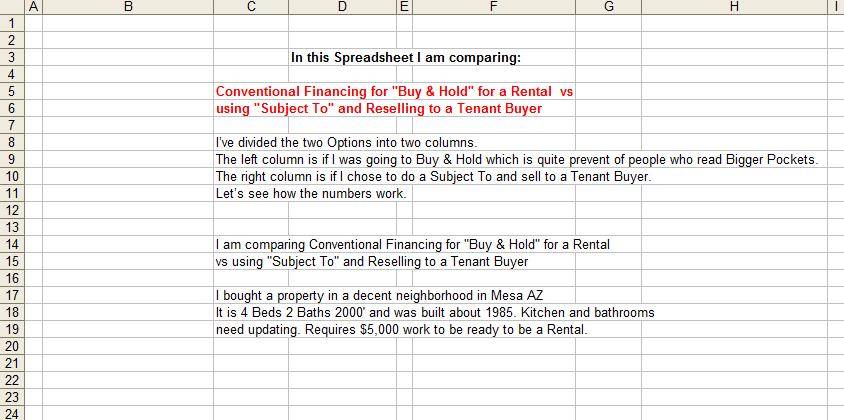

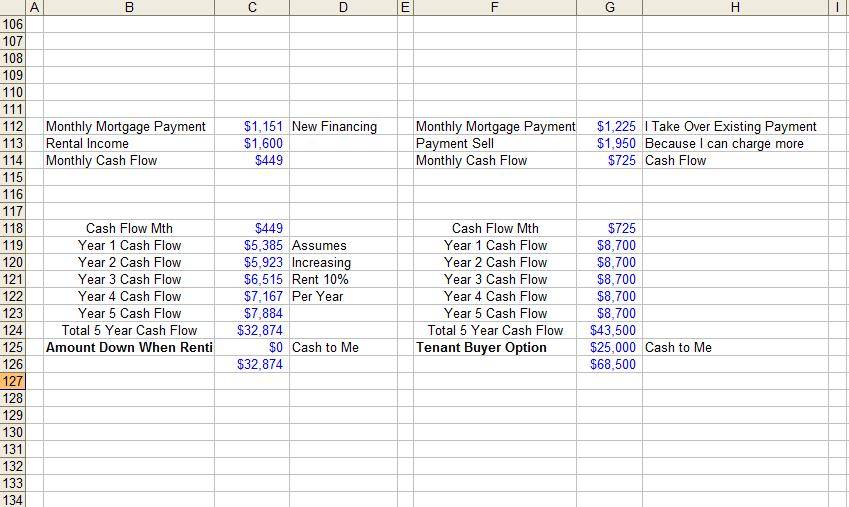

I was asked by a couple of people to compare doing a Buy & Hold Rental using conventional financing and buying Subject To with selling to a Tenant Buyer and what that would look like.

This is an actual deal I recently did. I bought a 4 Bed 2 Bath 2000' property in a decent neighborhood in Mesa AZ that was built about 1985.

In this Spreadsheet I am comparing:

OPTION: 1 Conventional Financing for "Buy & Hold" for a Rental vs ---- OPTION: 2 using "Subject To" and Reselling to a Tenant Buyer

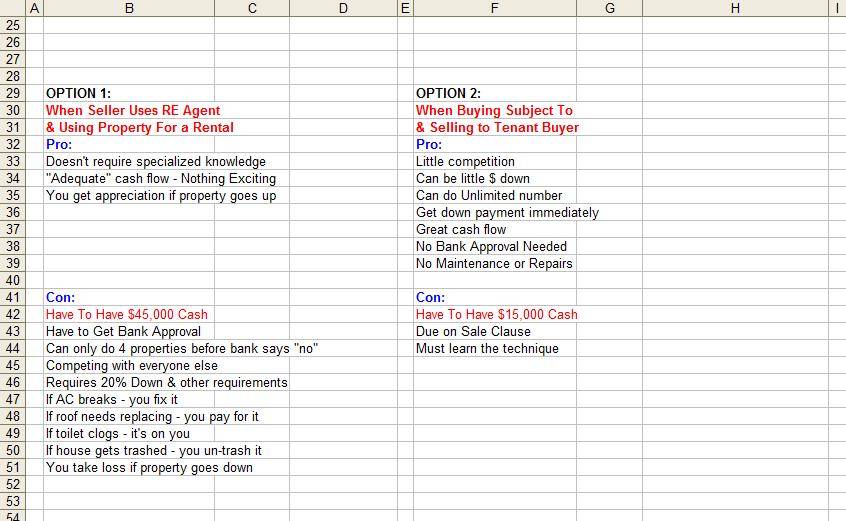

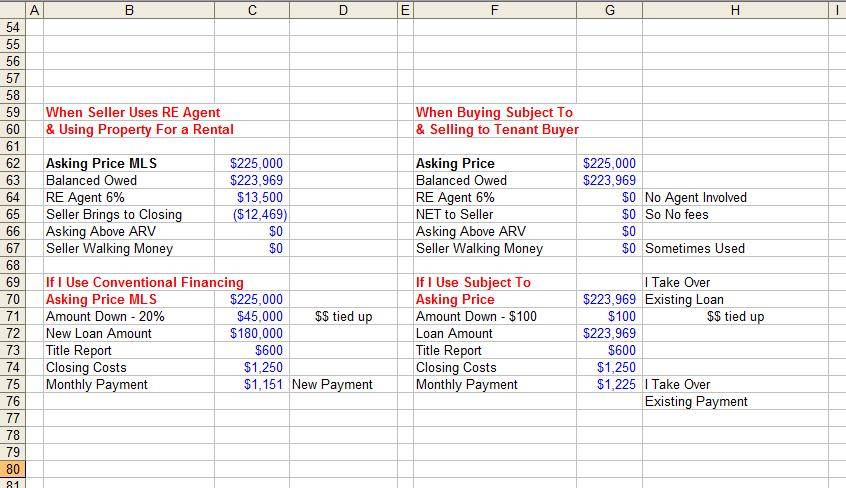

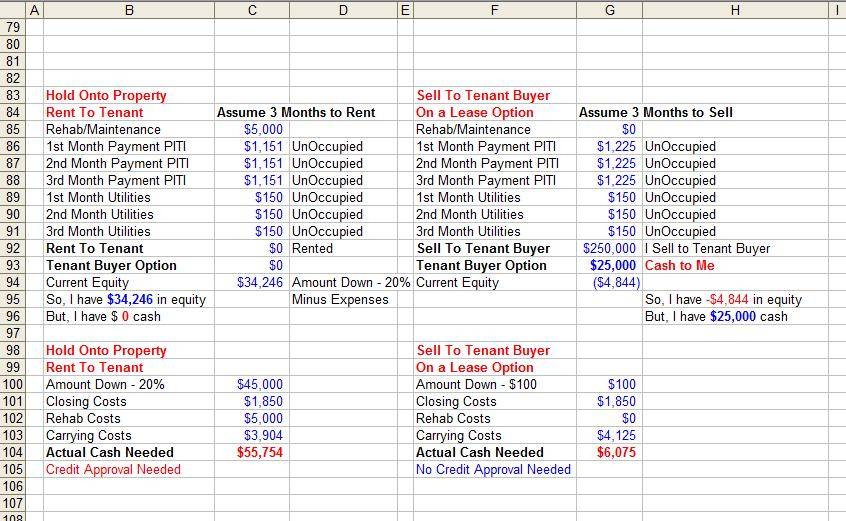

OPTION: 1 As a Rental, the Kitchen and Bathrooms needed updating requiring about $5,000 of work in order to be ready to be a Rental. From the Renter I would get first month’s, last month’s and deposit. I would have to have a loan from a bank with 20% down or about $45,000 to qualify.

OPTION: 2 Selling it to a Tenant Buyer requires no rehabbing on my part.

The Tenant Buyer will do (or not) the rehab to their liking. From the Tenant Buyer I get an Option Payment of $25,000 and a rent payment when they take possession. There is no deposit. Here I simply take over the existing loan and payment & need about $15,000 “Cash on Hand” to cover expenses & reserves etc. I can sell the property for more because he doesn’t have to qualify at a bank and will pay a slight premium.

Let’s see how the numbers work.

Click On Each Section To Enlarge

Most Popular Reply

We're lucky here in Canada that we had virtually no fallout from the GFC. We're getting a long overdue price correction now but it wasn't caused by the insane lending policies that caused the credit crisis, just good old fashioned irrational exuberance and interest rates getting pushed down too low during the pandemic. I haven't heard of any weird legislative stuff relating to financing here except for a temporary moratorium on foreign buyers and possibly putting limits on how many single family homes private equity firms can buy.