Classifieds

Market News & Data

General Info

Real Estate Strategies

Landlording & Rental Properties

Real Estate Professionals

Financial, Tax, & Legal

Real Estate Classifieds

Reviews & Feedback

Updated 2 months ago on . Most recent reply

- Real Estate Agent

- Nashville, TN

- 148

- Votes |

- 288

- Posts

Anyone Can Own Real Estate. It just takes a little savvy, and sweat.

Welcome to the Skeptical Investor blog, right here on BP! A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

___________

Today, we’re talkin’ market updates, housing affordability, and how anyone can get started owning real estate. Conservatively. No gurus, no gimmicks. Just tried and true real estate investor strategies.

It’s a longer article today. I thought I would give a few extra nuggets this Memorial Day week. You won’t want to miss the end, on my dad’s wild real estate ride. Trust me, it’s worth it. 😉

Let’s get into it.

___________

Today’s Interest Rate: 7.02%

(☝️.10% from this time last week, 30-yr mortgage)___________

The Weekly 3 in News:- -Is it a bull market? ““All in all, I’ve remained bullish,” says economist Ed @yardeni, “I think it’s a bull market, and I think we’re heading higher over the rest of the decade.”

- -Emerging Trends in Real Estate: 2025 Top Markets lists the top 10 markets to watch. Dallas, Miami, Houston, Tampa and, of course, Nashville round out the top 5 (EmergingTrends).

- -Fun Random Fact: You prefer the smell of a potential romantic partner over another because it reflects their underlying immune system composition. In general, people select/prefer partners with immune systems more different than their own. Which makes perfect sense. Any offspring = hardier (Huberman).

___________

News headlines will be aplenty this shortened Memorial holiday week. Data releases on Core PCE inflation, pending home sales, and Federal Reserve minutes will provide signals about interest rates, housing demand, and economic growth. We will also get a double dose of consumer sentiment numbers (both Conference Board and UMich), the revised GDP growth for Q1 2025, and jobless claims.

Let’s get ready for volitilityyyyyy!

Interest Rates Popping

The Federal Reserve meets 8 times a year, the next is June 17-18. At each meeting, they make a binary decision: Cut interest rates or increase rates (yes, yes they can also just leave it alone too, smart *** :) ).

Should they cut? Inflation looks under control, and the bond market is throwing a tantrum about our escalating federal deficits, which are being exacerbated by high interest rates.

I think they should.

Will they? Here is Atlanta Fed President Austan Goolsbee on the upcoming decision,

“The bar for me is a little higher for action, in any direction, as we are waiting to get some clarity [on potential tariff effects].”

I think they won’t.

The problem. GDP data comes out after the quarter is over. And even then that number isn’t final, more lagging data needs to come in, and it is revised (like it will be this week). So Something might have already happened to slow (or grow) the economy. It’s like watching the game you recorded after the fact, and before you check you text messages.

Also, a side note: the Fed doesn’t trust the Administration. Right or wrong, they are concerned, bordering on fearful, that global trade policy is being rewritten at too rapid a pace and with too much uncertainty. However, that is precisely the intended strategy of this Administration, so the two may be at loggerheads for a while until the Fed gets comfortable with being uncomfortable. Or if the labor market breaks down.

I got distracted there…the Administration’s trade policy is not my point. It’s that the Fed has another armament in its arsenal, and it’s not being discussed much.

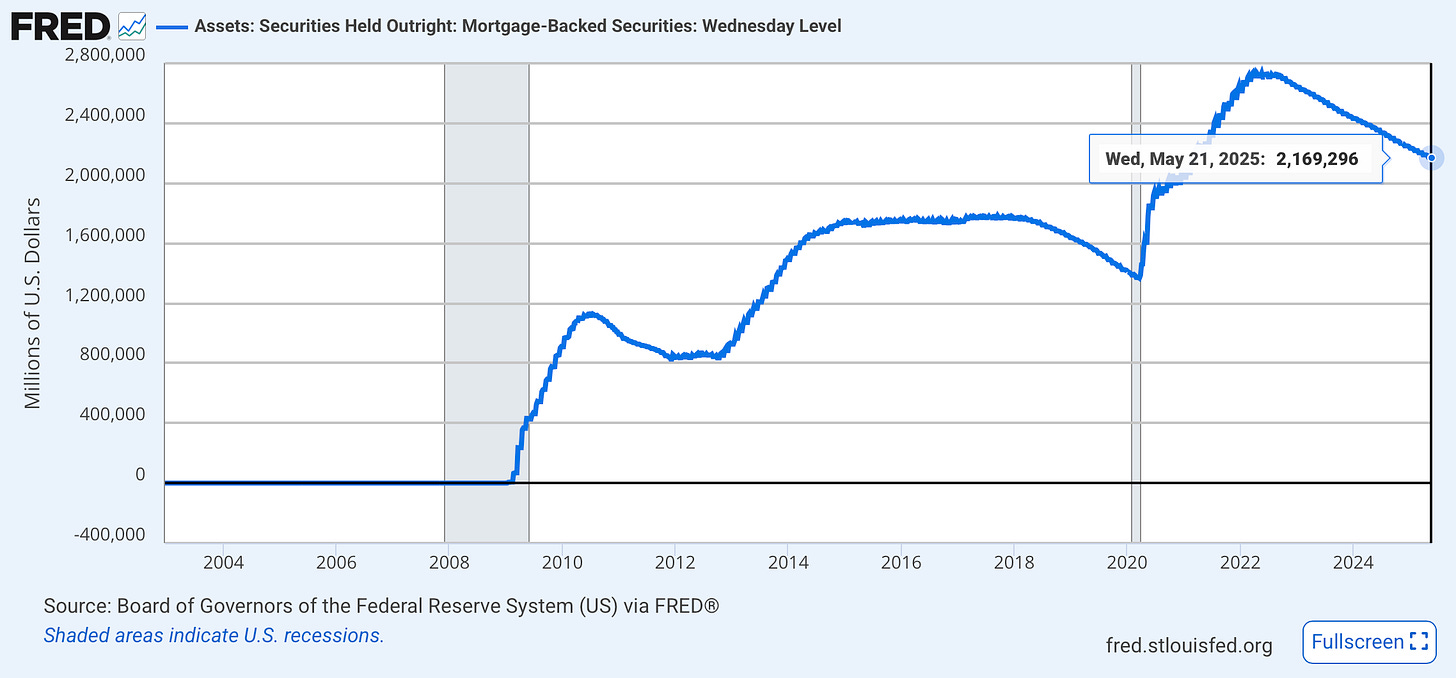

There is another way the Fed affects long-term interest rates: Quantitative Tightening/Easing. Aka printing money and buying bonds.

Interest Rate Pressure from the FedThe Fed is slowly unwinding its ownership of mortgage-backed securities (MBS) off its balance sheet, which it bought heavily in 2020, and didn’t stop even in the red-hot 2021 real estate market. This kept interest rates unnecessarily / artificially low. Fun fact, the Fed never owned MBS prior to '09, then put trillions of these assets on its balance sheet. And reupped with another trillion during COVID. As of May 22nd, the Fed still owned almost $2.17 trillion of these assets.

This extreme buying of MBS artificially kept interest rates down both in the post Great Financial Crisis and COVID eras 2020-2022, distorting the housing market.

When times were really good, that was the time to take the foot off the gas pedal. Yet, the Fed kept buying MBS. The result: inflated home prices.

As they unravel their ownership (aka Quantitative Tightening) of these holdings, removing the liquidity they injected in the market, it will put upward pressure on 10-yr Treasury and mortgage rates. This is one reason why the Fed announced at their last few meetings that they would be slowing their rate of selling MBS off their books. This process of quietly slowing their (QT) started in April.

This is another reason, in my humble opinion, the Fed should restart cutting interest rates. QT is what they should have done back in 2022, while raising rates.

The Fed should stop QT, and resume once rates are back down to normal (r*) levels.

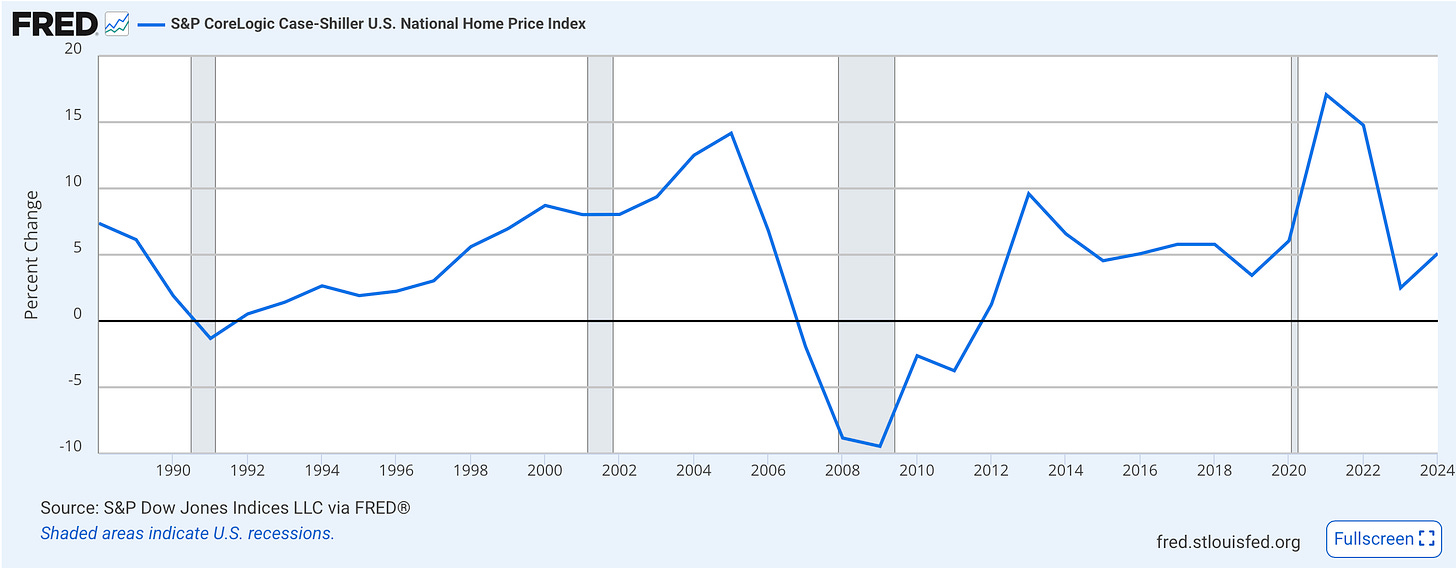

Home Prices and Affordability

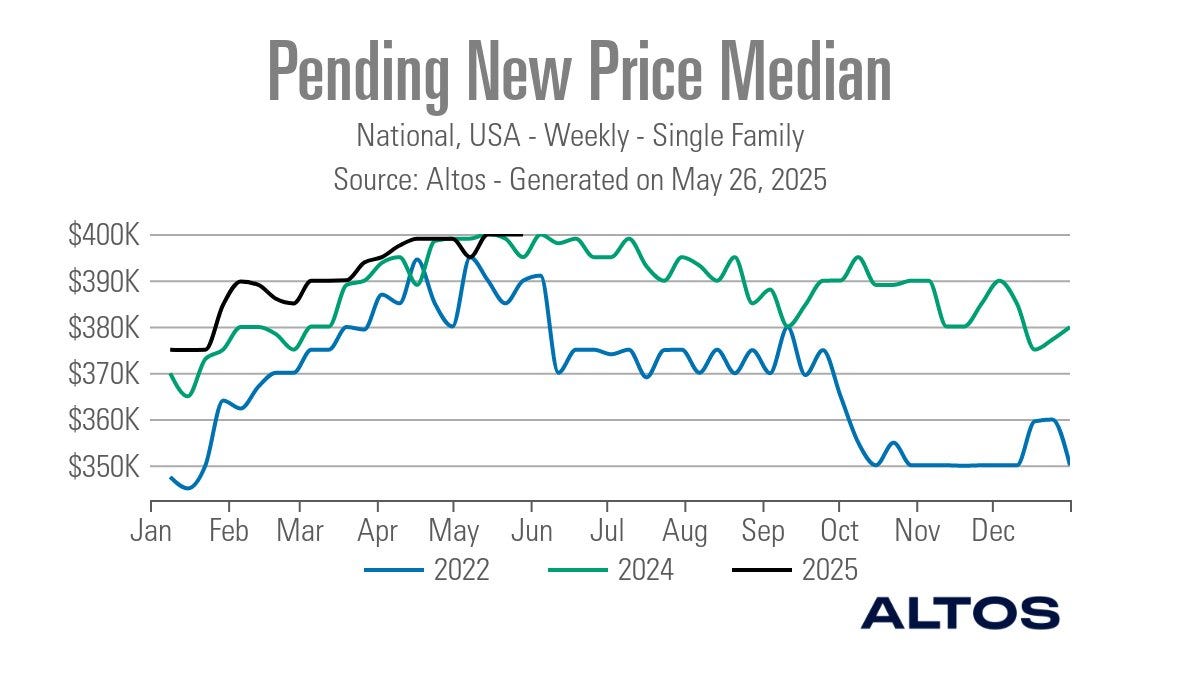

Keeping on this home price theme, we all know home prices are elevated, and will likely stay that way. Inventory is gradually improving but remains tight, with home prices expected to rise moderately in Q2, the strongest quarter of the year. Real estate is highly seasonal; homebuyers start buying in March and continue through mid-summer, driving seasonal price increases. And this year is looking no different (Altos).

Home Price Crash! ? No.

Home prices were up .8% Feb-March (latest data), up 3.4% YoY, and up 52.3% since March 2020 (ResiClub).

All the gurus out there are predicting a home price crash this year, like they do most years, but this is unlikely. Inflation may be variable, but prices are permanent. If you are waiting for prices to meaningfully decrease, it’s going to be a long wait.

But that is not to say affordability has been rectified, far from it. So, how is this affecting homebuyers?

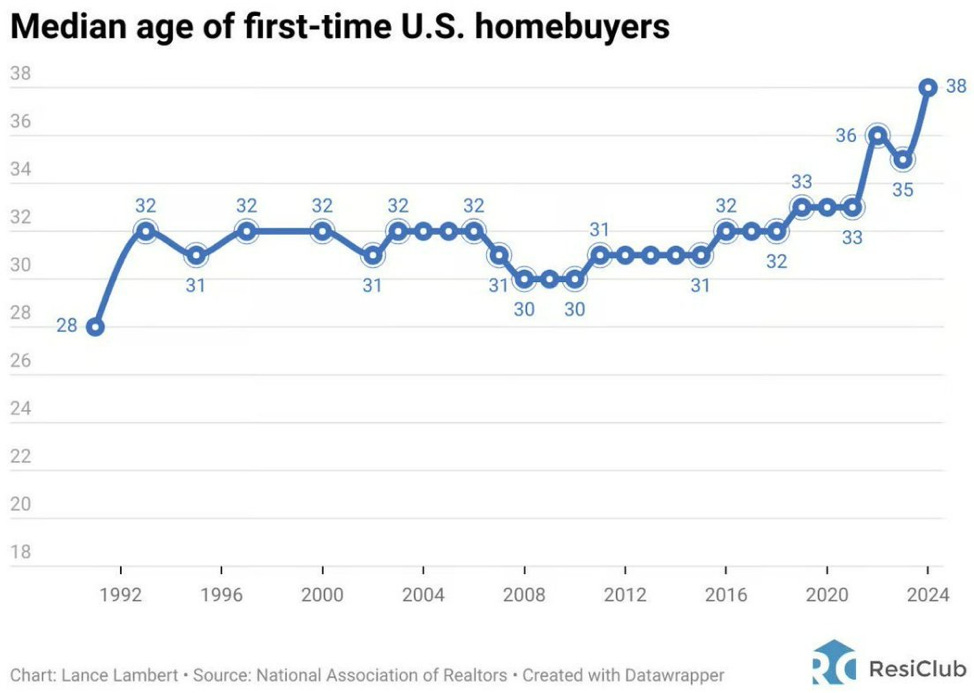

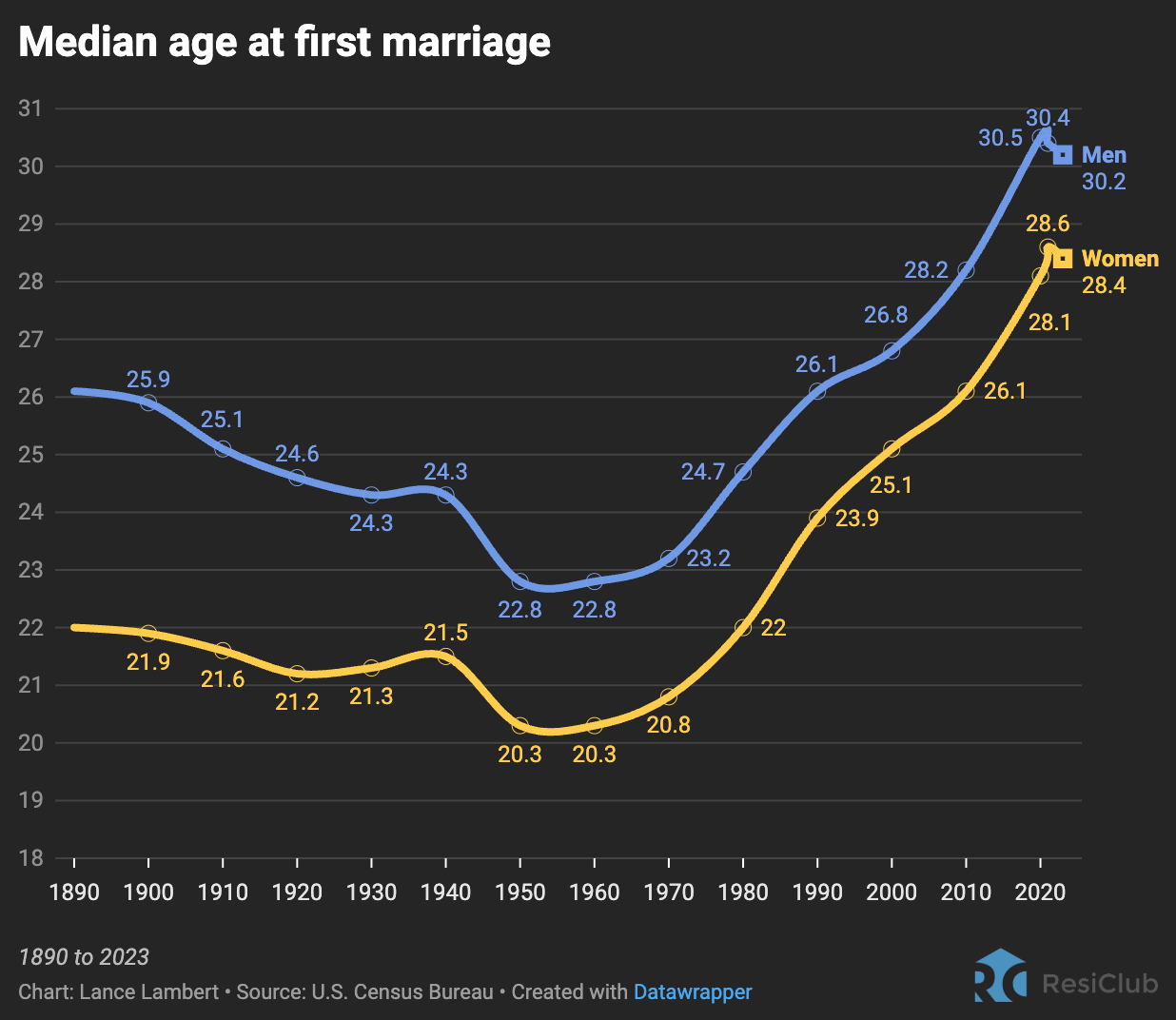

Median age of first-time homebuyer hits all-time high.In 2005, the median U.S. homeowner lived in their home for 6.5 years. Today, that number is 11.8 years (). Why? Much of this is being driven by home price affordability for first-time homebuyers. The median age of first-time homebuyers is now 38, ten years older than it was in the 90s.

And, first-time homebuying is often part of another life event, marriage, which is also happening later in life (yours truly included, sadly ResiClub).

Why is this happening and what to do about it?

Why is this happening and what to do about it?

Mortgages are expensive. So for first timers, it’s likely interest rates, which have driven up that monthly payment, even more than the overall home price, which is driving unaffordability.

To get the housing market healthy again, we need two things to happen:

- Lower interest rates. This will happen once the Fed cuts rates, and the federal government gets its fiscal house in order, driving Treasury bonds down, and thus mortgage rates.

- More homes! But….new construction is still slow vis-a-vis demand.

Sadly, this is not to be.

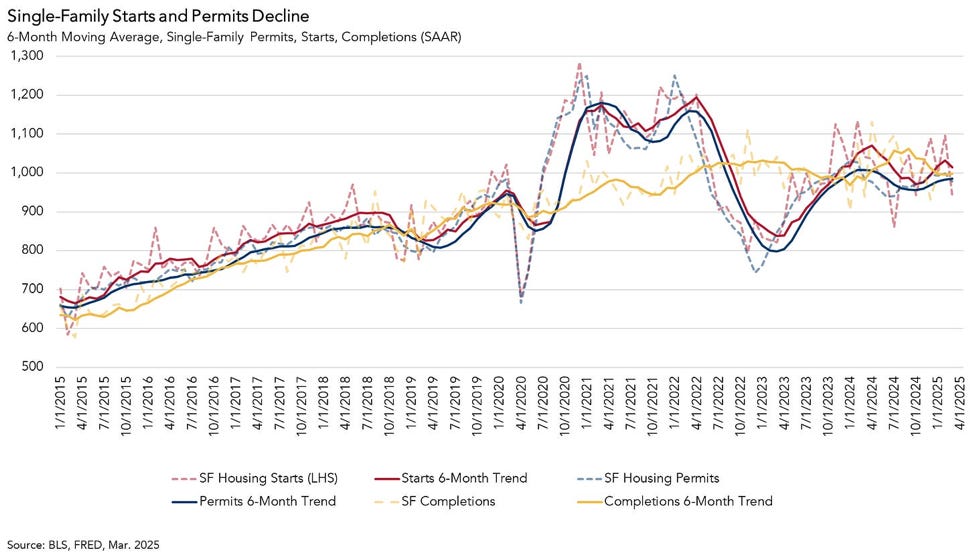

Construction of Single-family homes is slowing

New building permits dipped 2% in March, after having stagnated for months. Completions are still heightened, meaning we will likely see lower new supply coming on market in the upcoming months. (Here is a fantastic set of charts from housing analyst Odeta Kushi).

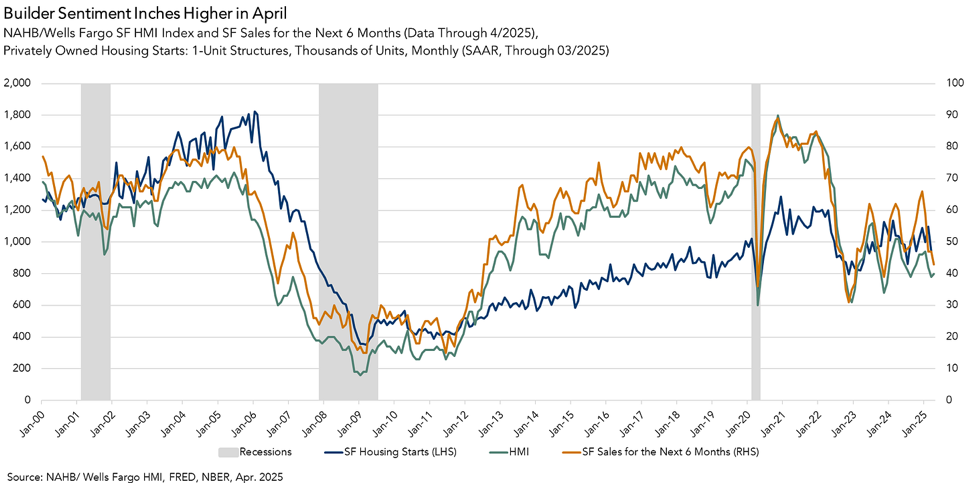

Case in point, home builder sentiment is in the pits. Well below 2019 levels.

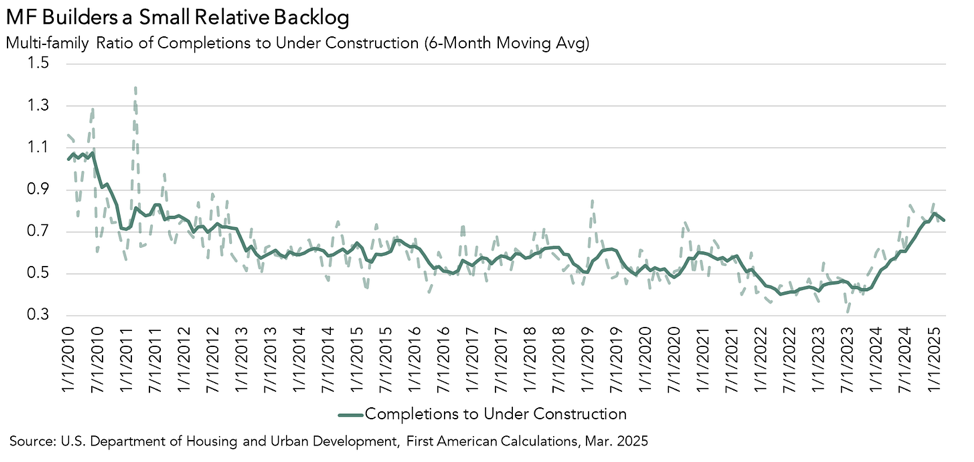

Multifamily builders now have the smallest backlog relative to completions since the tail-end of the Great Financial Crisis in 2011.

This imbalance will be the primary reason home prices, and to a larger extent rental rates, will resume their trek higher.

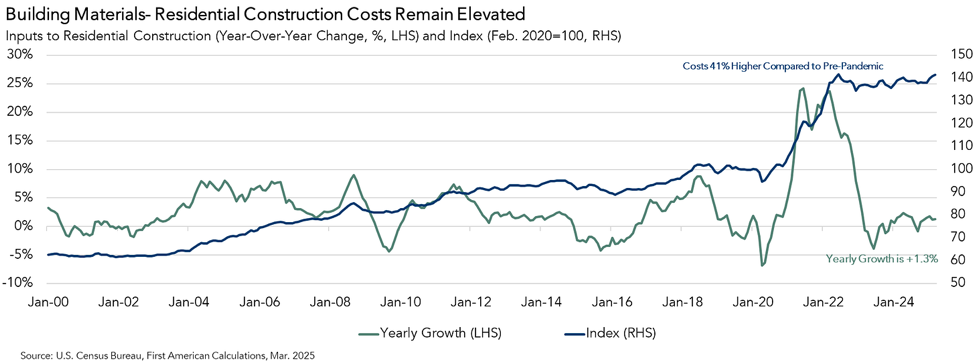

Yes home prices are ~40-50% higher than 2019 levels. But guess what led this increase? Inflation. Hell, building costs went up 40%!

This is why inflation sucks. And again, why Fed policy and government spending really matters for real estate.

So, don’t buy a house, right? I mean, it looks and feels like it’s a terrible time. I’ll just wait till interest rates come down and maybe prices will come down too? I hope.

I disagree. Hope is not a strategy.

Is it really not a good time to buy a house?

I would argue no, it’s a fantastic time to buy (but it’s a difficult time to sell one).

And further, I offer this...

Anyone can own real estate.

Anyone.

It just takes a little savvy and a bit of a typical lifestyle sacrifice.

Let me tell you how…

Owning Real Estate is within reach for Anyone.

Again, it is absolutely true that home affordability is still really really tough. 7% interest rates are pure yuck, especially when we were just teased with 3% rates and 80% of all mortgages today are below 5%.

A rate of 7% vs 3% can seem like a world apart. To put this in perspective, a $400,000 home with a 20% down payment would have a monthly payment today of ~$800 more than just a few years ago. Put another way, the same monthly payment then would buy you a $600k house, now you can only afford a $400k house.

Scheiße!

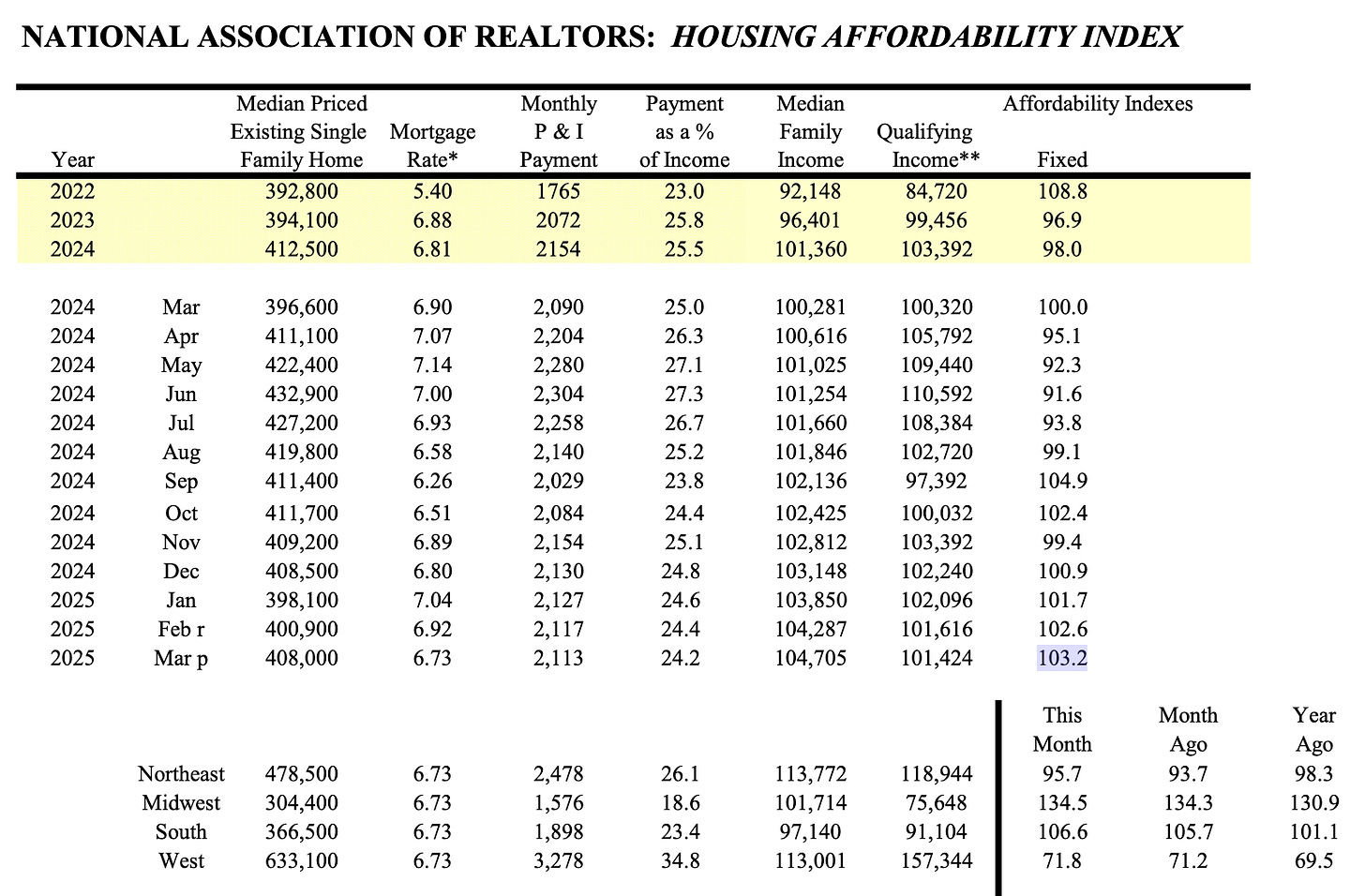

But the market is adjusting, although I would argue temporarily. In fact, according to the National Association of Realtors Housing Affordability Index has improved for 5 straight months, the highest reading since last September, back to 2022 levels.

Home affordability is hurting buyers’ ability to buy, meaning those looking to sell are having a hard time finding buyers and are being forced to lower their asking price (again this does not mean overall prices are dropping. The asking price is lower). Savvy buyers, and us investors of course, who can afford the mortgage (or have cash) are finding themselves in the driver’s seat. The avg list-to-sale price gap is staying wider, albeit better than 2023 when interest rates hit 8%.

This is called a buyer’s market. And I love it.

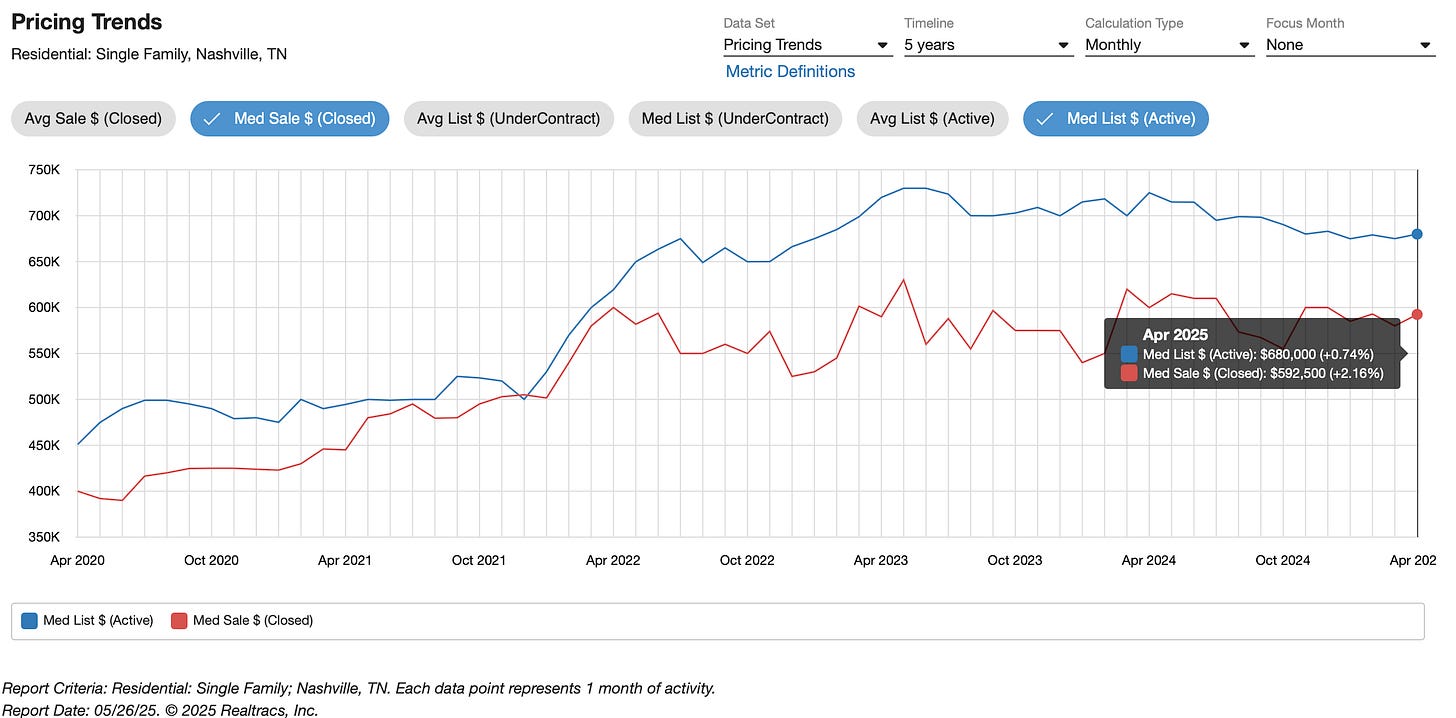

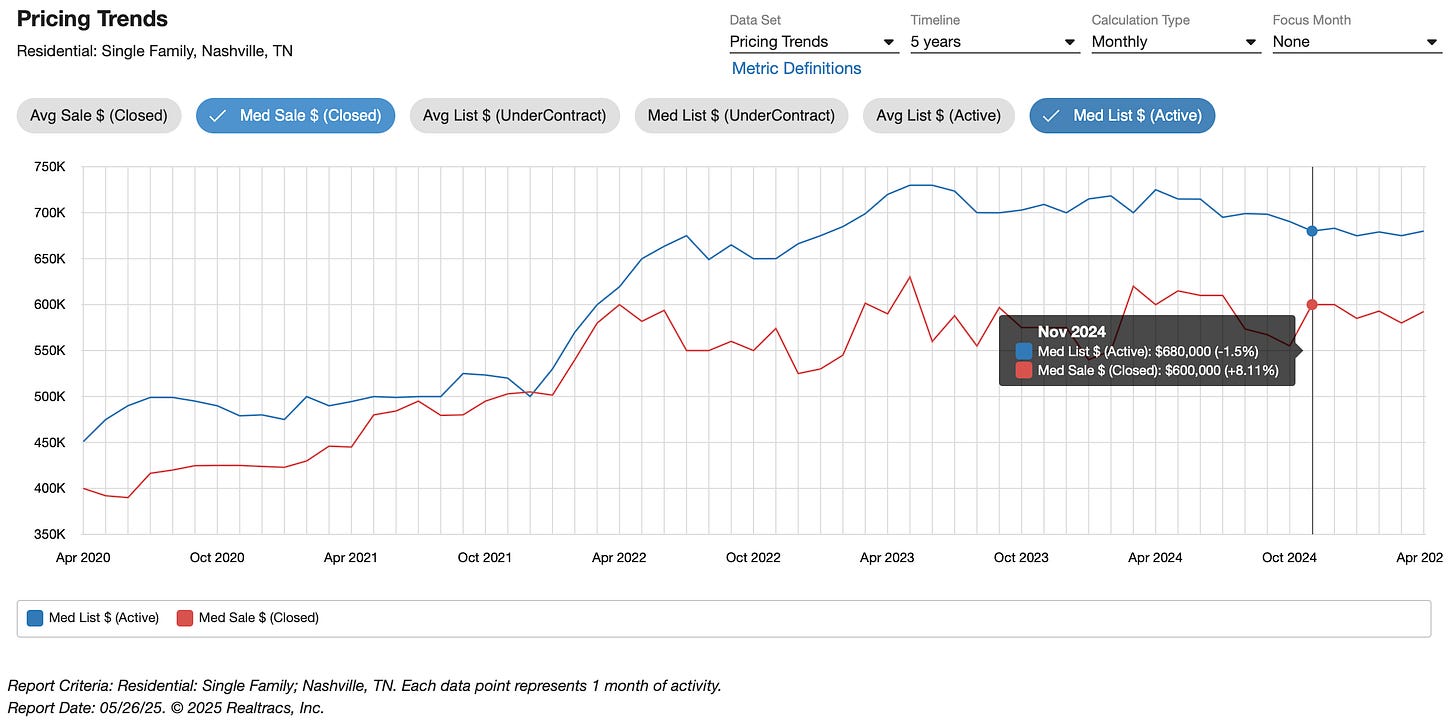

And see that tick up in November data, tightening the ratio of list-to-sale price? Know why it tightened?

Remember what happened last September?

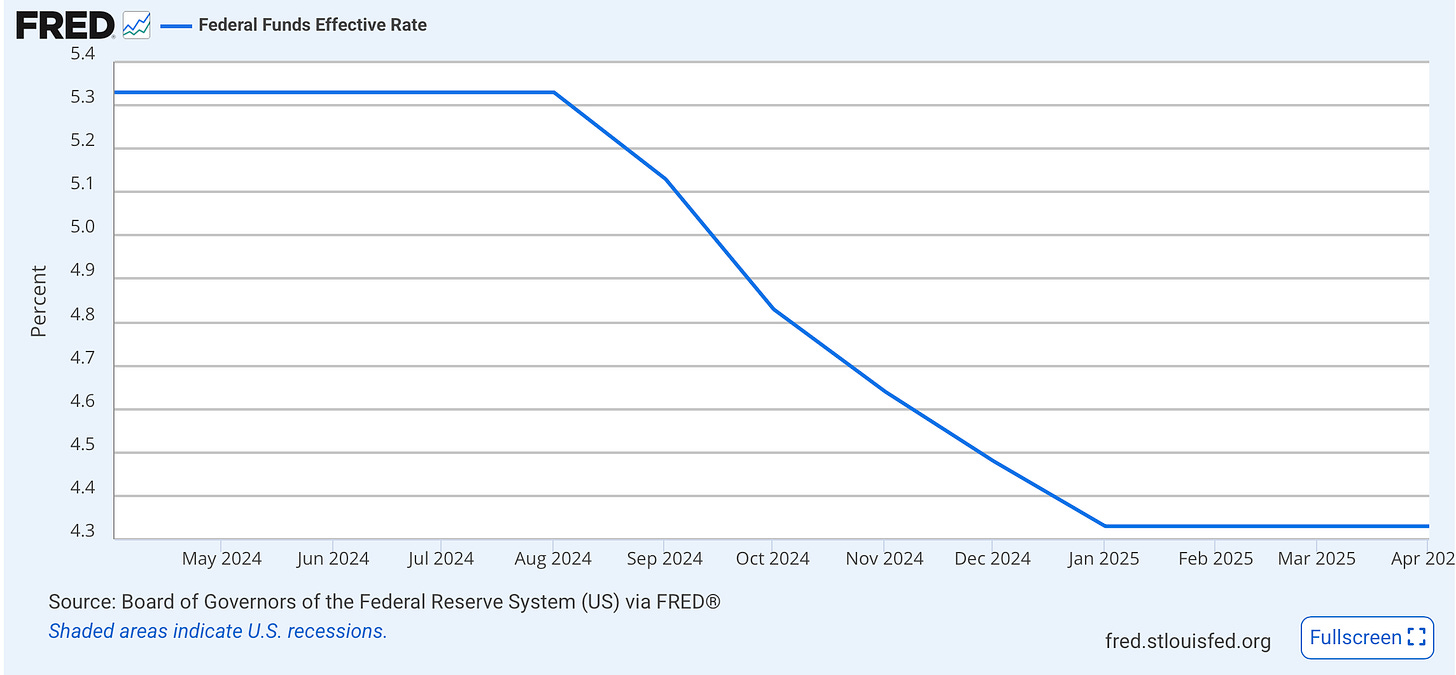

The Fed started cutting. And the home list-to-sale ratio tightened.

But then they stopped cutting in December. And since then, well, you guessed it, homebuying demand flatlined (driven by bond prices, which took mortgage rates back up to 7%).

So while it is true that home affordability is low, this is a direct result of higher interest rates, not a systemic financial or housing crisis, as there was during ‘08-09. The Federal Reserve is holding rates artificially high on purpose, in an effort to slow inflation.

This is why we will not see a meaningful decline in home prices, in my humble data-driven opinion.

Further, inflation is progressing down, and is now almost back to its 2% target, which we all see in the grocery store and gas station. Hell, egg prices have fallen back to reasonable levels, down ~50% since March.

What this means is - and it might be 10-18 months - but mortgage rates will fall. And once they do, home prices will spike higher than ever as literally millions of households get back into the market looking for a home. And then again, when rates hit 6% and then 5.5%, demand will hit rabid zombie levels. And rising demand will mean home prices 👆.

And you will have wanted to have purchased that property already.

So…Buy now, or Wait?

It’s the age-old (lazy) question: should you buy now or wait?

Let’s look at an example of a typical single-family home and see what the digits tell us.

Why Buying is better: Example CaseLet’s say you are purchasing a home for $400k in Nashville, TN, using my home market as an example.

At 7%, your mortgage is ~$2560.

Let’s assume it takes 12 months for rates to come down and the “normal” rate will be 5.5%. (The 3-4% COVID-era mortgages are likely never happening again, so let’s just forget about that pipedream).

Purchasing that home today will cost you 12 months of higher interest at 7% (vs 5.5%), or $6006 in additional interest costs.

So, if you purchase a home today you will want to make sure you get a deal, and pay $6006 less for the home than comparable homes.

Then, the plan would be that once rates come down, you refinance your current loan into that lower 5.5% (or lower) rate.

Importantly, make sure to select the right lender, ask your Realtor for their preferred lender list, which any self-respecting one should have in their hip pocket (you can DM me for mine).

And let’s not forget we are in a buyer’s market. Why stop at $6006 off the purchase price? We can be much more aggressive in our home purchase negotiations. Just last week, I got a client $45k off the purchase price, which is below market value, below the comparable median sales price. That’s saving 7.5x the extra costs of stomaching the 7% interest rate. Boom.

And, remember that home will appreciate 5% on average. (Much more if you do some improvements).

So, in those 12 months while you are waiting, that’s an additional $20,000 you are missing out on, or ~3x the amount you were trying to save in interest by being “patient and waiting.”

Home prices rarely go down. Since 1988, it’s really just happened once in a meaningful way, and that was the Great Financial Crisis, focusing on housing and bad financial practices.

So, what have we learned? As long as you can afford the higher mortgage, it likely makes far more financial sense to just eat that higher mortgage cost and refinance later into a more normal rate. Even if it takes twice as long for rates to come down the math still makes total sense. In fact, your real estate investment will likely make you several times your money back. And if you can improve the home through renovation, even if DIY / moderate, your wealth will grow even more.

But wait, there’s more.

When you own a home, vs rent, you can also:

- deduct the interest you pay right off your taxes,

- move out and rent it, and then depreciate the asset itself off your taxes

- and if you sell it, you are exempt from paying $250k in taxes on the appreciation gains ($500k if you are married).

Now for the cresendo….

Do you think homeownership is unaffordable, out of reach, impossible, too expensive for you?

Hogwash!

You can “House Hack.”

What’s that? Well, kind sir / ma’am, get ready to have your mind blown.

The House Hack: A Strategy for Everyone

The question I most often get asked about getting into real estate investing is: “Well, what do you think I should do?”That’s a lazy question…

There are literally 100s of strategies in real estate investing. Short-term rentals, single family homes, small multifamily, medium-term furnished rentals, self storage, commercial 100 unit multifamily, retail, strip malls, mobile home parks, etc…

But if you are looking to start, and especially if you are young, have few obligations, or don’t have much cashola in the bank…

You, yes you, can House Hack.

I strongly believe this is the best way for anyone to get into real estate. I love this strategy.

There are several variations to house hacking, but in essence, house hacking is when you live in the home and generate income by renting part of it.

Hot take alert: Normally, I tell clients that living in your home is not an investment. Your primary residence is a liability, not an asset.

Well, that is still true, but not when you Hack that House, baby!

As an individual who intends on living in the home, you can obtain a subsidized loan from the bank, called an FHA loan. The government's Federal Housing Administration backs this loan, meaning they guarantee the loan for the bank, incentivizing banks to make this type of loan, even if the borrower, you, is considered higher risk, has poor credit, or doesn’t have much $. You can typically obtain a loan for 3.5% down, and the interest rate is lower than the market rate for a 30-year mortgage. There are, however, additional fees, including mortgage insurance and an upfront FHA fee, which helps fund the program. But, you can buy a house for 3.5%! (a 5% conventional loan is also a great 1)b) option, if you have 5% saved. Ask your lender).

But that’s not why this is so powerful.

There is no limit to the number of homes you can buy with FHA loans. FHA loans, despite popular belief, are not for first-time homebuyers. In fact, you can buy a new FHA home every year; it just has to be your primary residence, i.e. where you live.

So long term, you can use the FHA loan program to grow a portfolio of properties and only have to put 3.5% down each time. You just need to keep moving into them, hopefully do some improvements while living there, rent out a portion of the home (like the guest bedrooms or walk-out basement or finished garage), then rent it out fully when you move out, and into your next home.

And if the area you are renting is considered a separate living space (like an in-law suite or duplex unit or ADU with a kitchen) you can use the presumed income from that unit to help you qualify for the FHA loan! BOOM.

If you can save 3.5% for a $400,000 home, that’s just $14,000. (And if you are a savvy investor, you can get your awesome realtor to negotiate a credit back at closing to reduce the down payment even further. (DM me).

$14k (or less, again, if you negotiated a credit) is MUCH less than the $100,000 you would typically need to save for the traditional 25% down investor loan or 20% primary home loan.

So, with that same $100,000 for a standard home purchase, you could buy…

…checks notes…

SEVEN $400,000 FHA homes.

This is why house hacking is so powerful. You can do one per year, and don’t forget to supercharge this by renting out individual rooms, in-law suite basements, finished garages, short-term-rental backyard yurts…while you are living there.

But wait, wait,,,there’s still more…

There is also a second option, since you are living in the home.

The Federal Government, in an effort to further incentivize home ownership, allows you to sell the home you live in and pay no tax on the sale.

Zero. With a few small limitations. Yes, the government actually did something fantastic.

Specifically, the IRS rule is, if you live in a home for 2 of the last 5 years, you can sell that home and you are exempted from any capital gains tax on up to $250,000 of the profits ($500,000 if you are married. Who said your spouse never gave you anything :).

So let’s say you bought a place for $500,000. Now you are a little older and have a better job so you have some cash. You can put $100,000 into it (much much less if you so the work yourself, like I had to do when I was young) and it’s now worth $650,000. After 2 years have passed, you decide to sell it. Now, remember we are house hacking so we only put 3.5% down to purchase the home, or $17,500, so we borrowed $482,500 to buy the home. Let’s also assume closing costs/fees of $10,000.

So after selling it, you are left with a profit of $650,000 - ~$482,500 - $100,000 - $10,000 =$57,500

Now, normally you would likely pay ~15% capital gains tax on that or $8625, but not today! Remember you are exempt from this tax since you lived in the home for 2 years and the profits were under $250,000 if you are single ($500,000 if married).

So your total return / profit remains $57,500 and your return on investment is $57,500 / (100,000+ 17500) = 49%!

Or expressed as an annual return that’s (49/ 2) = 24.5%!

(Drop me a note if my math is off, doing this on the fly! Literally, I’m on a plane now).

You can do this “Live In Flip” model every 2 years.

Almost All of My Homes Have Been House Hacks

When I was young, single, and broke making $30k/yr in Washington DC this is how I started investing. I bought a home every 2 years, moved in, rented out rooms to buddies to cover my mortgage, fixed it up (much myself), sold it and reinvested the tax-free earnings in a new home.

It just took a little sweat and a different lifestyle, which wasn’t bad at all, frankly, and I met some great people I am still friends with to this day.

I didn’t know the catchy “House Hack” alliteration at the time, I just knew I needed to save some money so when I took a lovely lady on a date I didn’t have to take her to Crackerbarrel (No offense CB, and back then I usually cooked dinner anyway. Cooking is another superpower strategy to save money).

But I didn’t stop there. For more than 10 years (ok it was longer, I was a frugal peasant, what can I say), far after I needed roommates to afford the mortgage, I continued to rent out the spare rooms in my house. I just threw up a listing on Craigslist or Facebook or Zillow or AirBnb. Saving on housing costs was a game changer for me, and gave me a wealth-building advantage even over folks I knew were making 2 or 3 times my mediocre government salary.

Remember, saving a dollar is far far more valuable than making a dollar because you have to pay taxes on the dollar you make. In fact, you will have 50% more money in the bank if you save $1 vs making an additional $1, assuming a 33% tax rate.

Go ahead, do the math. I’ll wait.

Eventually, I house-hacked enough times to be able to afford the standard 25% down payment to buy a standalone investment property without moving in. I would do large renovations (you have to, to get cash out) refinance them afterward, pull cash out and buy another investment property (aka the BRRRR Method, if you are familiar. Hat tip to David Greene). And then I would do another, and another, and another….

And I also did not stop buying, moving in, renting, improving and selling a new primary residence House Hack, every 2 years.

So what’s the downside? It takes a little lifestyle sacrifice. You have to move every 2 years, and live with housemates (unless you get a duplex). But that’s it.

Again, this is why I assert that anyone can start growing a real estate portfolio. No fancy tricks. No gurus. No overleveraging, bridge loans, hard money, or mob boss loan sharks. This is one of the most tax-advantaged, low-risk ways to make money, period. In real estate, or otherwise.

And if you say you are hungry to get started in real estate, but aren’t willing to do the work - aren’t willing to have some sort of posh lifestyle sacrifice - well, that’s a fine personal decision, but just be aware that it’s a poor financial one.

Anyone can do it.

What say you?

And, here is the story of my dad…

My Skeptical Take:

People need homes, be they renters or owners. This problem is not going away. It’s become a chronic issue in America. And delayed household formation is revealing a rental opportunity to serve late 20-30 somethings who may rent 10 years longer than previous generations. This is a core thesis of mine, as a real estate investor.

More beginners (and everyone really) should House Hack.

It is a great financial decision. Plus, getting involved as a landlord is also good for humanity. We have a severely limited housing supply, and we need every investor we can get to pitch in. After all, the government doesn’t build homes; investors do. House Hacking provides more housing units to the market, at an affordable price.

And, again, anyone can do it.

But don’t take my word for it. Let me tell you a story about the wild lifestyle sacrifice my dad made.

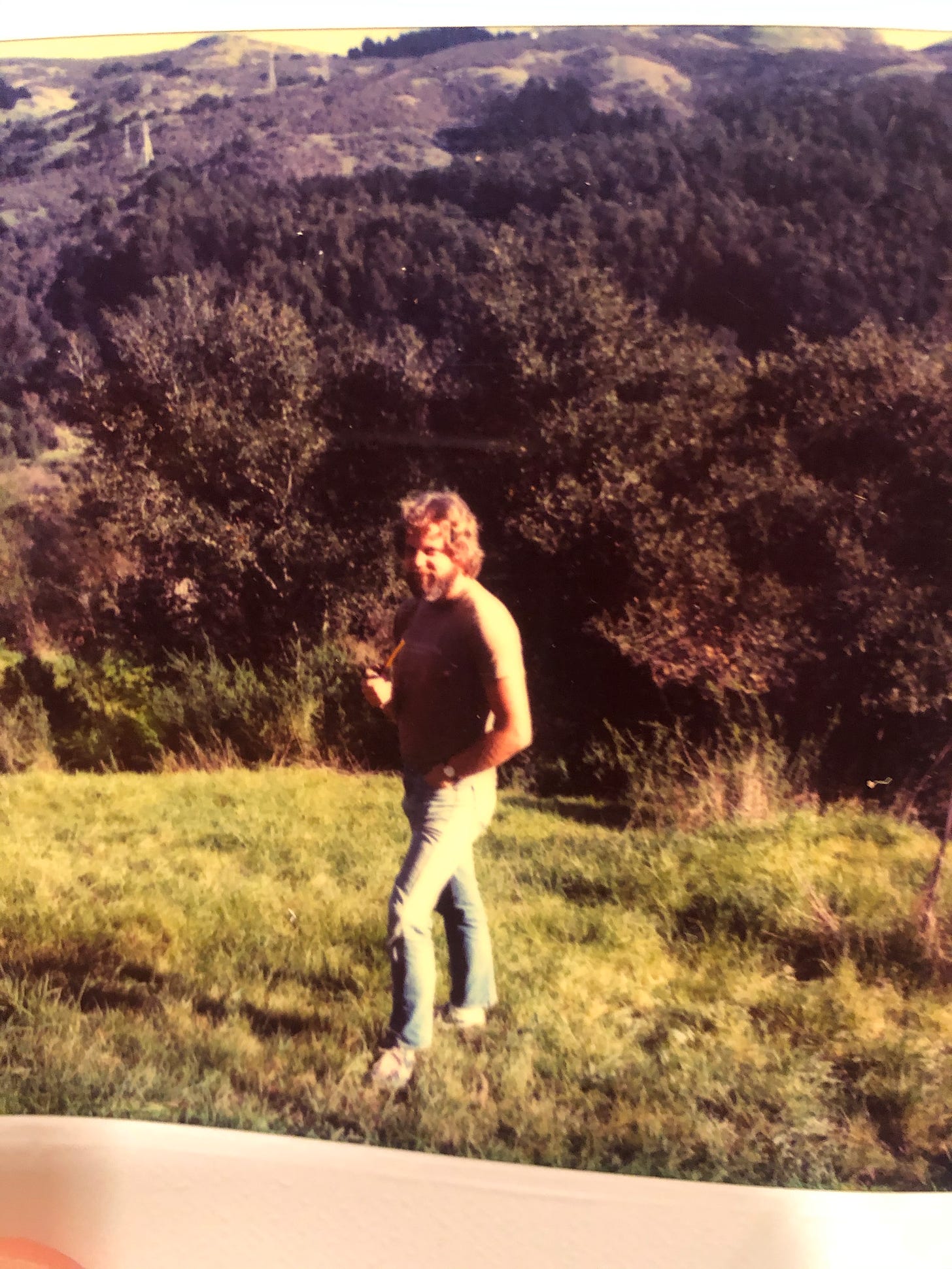

The Ultimate House Hacker: My Dad.My dad was the ultimate house hacker, before it was in vogue. In 1976 he bought a piece of land on a cliff in Kensington, CA for $70k. He built the home himself over the course of 4 years, relying only on a few subcontractors to lay the large pillar foundation into the property’s steep grade. But he didn’t rent an apartment while he built it. No, No… He was a little bit of a barbarian. He slept in a tent in the backyard for 2 years until the home was livable. Camped and cooked by fire and roughed it.

He was a general contractor, so he had the skills, yes (although he candidly told me he had never built a full house before), but to afford the land and materials, he couldn’t stop working. Every hour in between construction jobs was time spent building the house.

He was even attacked by a mountain lion one night in 1978, which I hear was quite the tussle. Good thing he survived, holy hell.

But that’s not all.

When he was close enough to finishing, around the time I was born, as the beautiful redwood home was coming to life…

… did we move in and start living it up?

No.

We moved in to the basement and lived in the lower level with a small kitchenette and he rented out the main home upstairs to maximize rents. Pictures of the main living space in the 70s Kensington, CA cabin below.

That red wood-burning stove is a little nuclear engine. Heats the whole upstairs no problem.

Now, do you need to go to this extreme?

It’s probably not for everyone, unless you are a little crazy. (I may be a bit. Hell, I once slept in my office for 6 months in my 30s while I was gut renovating a House Hack. I invented a few chef-mike dishes that were pretty amazing, if I do say so myself).

But maybe you can live through a little renovation on your home, or better yet, use some elbow grease to do some of the work yourself? YouTube University can teach you most everything. Tile that shower. Finish out that garage bedroom or basement. Add appliances. Paint. Landscape. etc…

After all, I think there is a little barbarian in all of us.

In Memory, on this Memorial Day, of an old Army vet. My Dad. Allan Mueller. (1941-2019)

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

-The Skeptical Investor

- Andreas Mueller