Updated 9 months ago on . Most recent reply

- Real Estate Agent

- Nashville, TN

- 180

- Votes |

- 359

- Posts

Governor Cook, You're Fired!?

Welcome to the Weekly Skeptical Investor BP Article. A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

----

This week, we’re talkin’ a new focus on the weakening labor market/employment #s, a changin’ “dovish” tone at the Federal Reserve, and I show a preview of my latest real estate project.

Let’s get into it.

-----

Today’s Interest Rate: 6.54%

(👇.05% from this time last week, 30-yr mortgage)------

The Weekly 3 in News:- - Warren Buffett is betting on the housing market. Taking a large equity stake in homebuilders D.R. Horton and Lennar (SEC filings).

- - Mortgage Applications are Up, again! We are at 6.5% rates, and since 2022, anytime rates drop to 6% - 6.64% range, housing data improves. We have had three weeks now with mortgage rates below 6.64% and 29 straight weeks of positive year-over-year data (HousingWire).

- - Nashville’s massive East Bank Redevelopment Plan is shaping up. The Oracle world headquarters campus and new Titans stadium will anchor the lovely riverfront greenway development (Nashonomics).

- - Breaking News Bonus - The President has fired Fed Governor Lisa Cook for cause, alleging mortgage fraud (buying 2 primary residences, to get a favorable mortgage rate). This vacant seat could secure him voting control of the Fed’s FOMC interest rate cutting board come May, 2026. But in a turn of events, Governor Cook is refusing to leave her position (I wish the rest of us could just do that). This week is going to be interesting! (White House)

The Fed Changes its Tone (again)

Last week, the Federal Reserve's annual Economic Policy Symposium took place in lovely Jackson Hole, Wyoming. The event featured many of the world’s central bankers, economists, and policymakers talk talk talking (and a few walk and talks) about global economics, focusing on inflation dynamics, labor markets, and policy frameworks. The US Administration’s trade and tariff policies were the primary boogey man in the room.

The bell of the ball was Jerome Powell, of course, and at his keynote speech, all ears were wide open to listen between the lines, and interpret the tea tasseography.

What did he say, and not say?

In short, Powell was more “dovish” than expected (a fancy way of saying/signaling future interest rate cuts and less restrictive monetary policy in his closely chosen language).

Now, if you are getting a little deja vu, you aren’t going crazy. We heard similar cadence from Powell a year ago, when the Fed started cutting rates. But then they stopped abruptly, concerned about trade and tariff policy. So far, it appears that concerns have not been warranted, and extending their restrictive policy into year 3 is likely contributing to the labor market slowdown.

A quick note on how we got hereThe ailing housing market is plagued by a lack of sellers wanting to sell their existing homes, leading to 1 million+ fewer homes sold annually than normal.

Why?

Every Tom, Dick and Harry refinanced their mortgage during the Fed’s wildly low interest rate policy during COVID. So today, 55% of homeowners have a mortgage under 4%, and 80% snagged one under 5%. But today's mortgage rate is ~6.5%. So buyers can't afford to buy, and sellers would have to sell at a price way down to move the market, which they will not do, as long as they have a job. So we are now living with the aftereffects of Fed’s loose monetary policy (which lasted farrrrr too long), the inflation it created and vastly declining homeowner mobility, which is not a good thing. The Housing market represents 18% of our total economy.

There is no free lunch.

Now, we need sustained lower interest rates for home sales to pick up.

Powell’s Language Signals Cuts

The market is a changin’. (Well, to be crystal, it’s been changing since January). Despite the Fed not cutting rates since 2024, the bond market has started the Fed’s job for them. Moving mortgage. Interest rates have been lower each week since 2025 started.

But now, a change.

Last week’s Fed speeches/talks in Jackson Hole (and the minutes for the Fed’s last Meeting were released), signaled the Fed is more likely than not to start relaxing its suffocating monetary policy. Before the Fed’s last meeting, meeting notes showed that a "majority of Fed members see inflation risks outweighing employment risks." However, this was July, just days before the "catastrophic" July jobs report (I wrote on this the other week here).

And last week, Powell’s carefully worded speech clearly signaled a priority shift from inflation to labor market concerns.

Labor > Inflation

In his speech, Powell noted that the shifting balance of risks "may warrant adjusting policy," clearly referring to the labor market.

- On inflation, Powell noted that tariffs/trade effects “are now clearly visible” and are expected to accumulate in the months ahead. But the question is, will they “materially raise the risk of an ongoing inflation problem(?)" Instead, the tariff effect could be a one-time (but not "all at once") series of price increases. I.e. Inflation may not be all that bad (as I have written about extensively ).

- On labor/employment data, Powell said the “situation [now] suggests downside risks to employment rising.” [While labor markets remain in balance], “it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers….This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher unemployment.” I.e. risks to the labor market from a slowing economy are more important.

- On potential interest rate cuts, he cautiously signaled a cut in September: “With policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.”

The Fed is now, as they say in the military, too close for missiles (inflation worry), switching to guns (labor worry).

Jobs reports will dictate rate cuts going forward. And we all know how accurate that data is…It’s going to be a volatile few months.

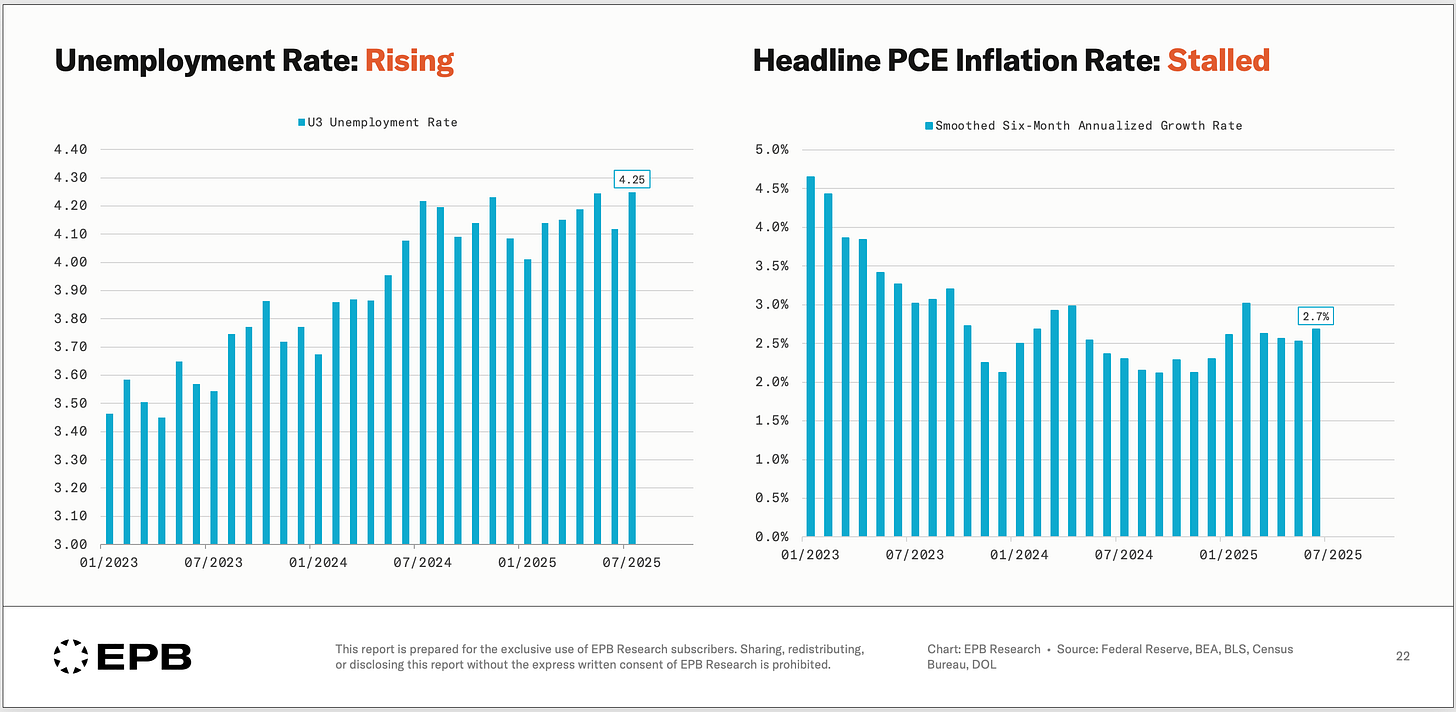

More on Why Labor is Now the FocusAs I wrote the other week, the last jobs report showed an average of just 35,000 jobs being created for the last three months. This was a shockingly horrible revision ownward in the data to the job growth we thought we had.

Here is a great chart, which shows the Fed’s conundrum.

The labor market is trending weaker, and inflation is trending down, but progress on the latter is stalling out.

In two weeks, we will have the final jobs week reports for the Fed to mull over before their September meeting.

Skeptical Counterpoint - Or was Powell doing a masterful job of saying nothing, giving a tentative indication of possible rate cuts while noting tremendous uncertainty?

Yes, he was doing this too, preserving the option to NOT cut if the data moves.

In other words, the Fed will probably cut rates .25% but if the data changes, they won’t.

Adding to My Portfolio

I’m putting my money where my keyboard is: just picked up this nice little duplex here in Nashville’s growing Donnelson area, just south of the famous Grand Ole Opry.

Plan is to renovate the kitchens, throw down new flooring, repair the roof (a tree fell on it), paint/scrape the popcorn ceiling, and spuce up the bathrooms. Plus I’m adding landscaping and 2 lovely decks for outdoor space on each side. May add fencing so tenants can corral their pups.

The Before Kitchen 1.

The Before Kitchen 2.

Target for completion is Halloween; hopefully the final budget for construction won’t be too spooky.

I’ll give you all some updates along the way.

My Skeptical Take:

This version of the Federal Reserve is out in 6-10 months, as a couple of governors retire, one is now under investigation for mortgage fraud, and Fed Chair Powell’s term ends (05-2026).

Fed version 2.0 will include many new faces who agree with the President’s more bullish/pro-growth, loose policy accommodation. Rightly or wrongly.

Aside # 1 - Reassessing the Fed’s Effectiveness

Interestingly, the theme for the Fed’s Jackson Hole meeting was "Reassessing the Effectiveness and Transmission of Monetary Policy in a Changing World." I listened to all the talks; I can’t say there was any “reassessing” of current monetary policy effectiveness. Zero. I fully expect them to try to stop all recessions and risk inflation and larger future recessions as a result. We should question the effectiveness of the Fed’s posture to always try to come to the rescue of the economy and if that is really a good way to run an economy. Current Treasury Secretary Scott Bessent has said they will actually be reviewing long-term federal reserve effectiveness.

Aside # 2 - Mortgae Rates Will Continue to Come Down Without the Fed

A Final Note on Mortgage Spreads - As I have written numerous times, the Bond market has been slowly edging lower and bringing interest rates with it (remember, mortgage rates follow the 10-yr Treasury bond but rhyme with the Fed’s Funds Rate). It does a masterful job of anticipating the Fed’s actions, as the efficient market (usually) does. But, an important note, the Bond market is still skeptical of inflation coming down and sees the economy as running hot. We see this in the spread between the 10-yr Treasury and the 30-yr mortgage rate. In fact, IF those spreads returned to “normal” historical levels, mortgage rates would be 0.46%-0.66% lower than today’s level (historically, mortgage spreads have ranged between 1.60% and 1.80%). So even without the Fed doing anything going forward and IF we get past inflation concerns, the Bond market will bring down mortgage rates to 5.86% - 6.06%, given today’s levels, a notable difference.

This is why I still anticipate mortgage rates to be below 6% in our near future (6 months or less).

Anecdote. In our real estate brokerage business, last week I had three buyers on three different deals get outbid. That kind of stuff hasn’t happened in two years. Slightly lower rates (6.5%) is invigorating the market.

This reminds me of the old adage, when the time comes to buy, you won’t want to.

Contemplation is good, but contemplation without action is bad.

Act accordingly, investors.

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

-The Skeptical Investor

- Andreas Mueller