Updated about 2 months ago on . Most recent reply

- Real Estate Agent

- Nashville, TN

- 161

- Votes |

- 314

- Posts

So the Fed Cut Rates. But Mortgages are..Higher?

Welcome to the Skeptical Investor weekly BP article! A frank, hopefully insightful, dive into real estate and financial markets. From one real estate investor to another.

-----

This week, we’re talkin’ Federal Reserve Rate cuts! Wait… why are mortgage rates up?

Let’s get into it.

------

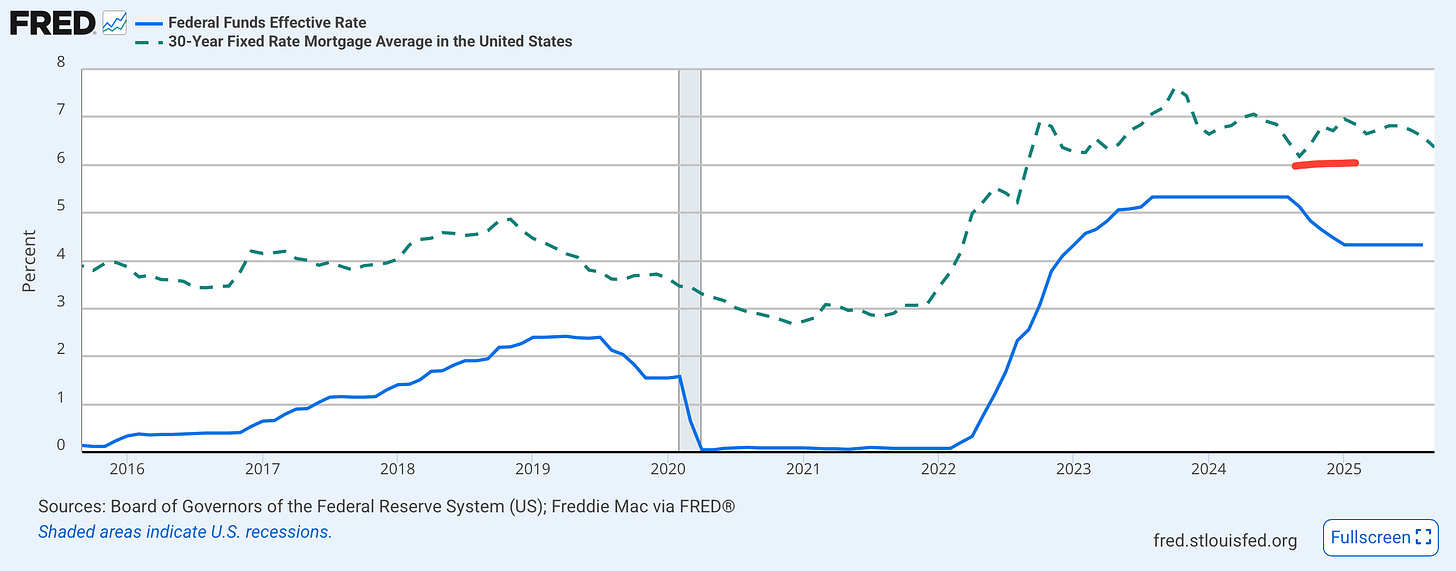

Today’s Interest Rate: 6.35%

(☝️.1% from this time last week, 30-yr mortgage)------

The Weekly 3 in News:- - In 2025, Florida is projected to have the highest annual cost of home insurance at $15,460, followed by Louisiana at $13,397 and Oklahoma at $8,369 (Insurify).

- - Chair Powell is soon to be a lame duck. US Treasury's Bessent says they are interviewing 11 Fed chair candidates (ET).

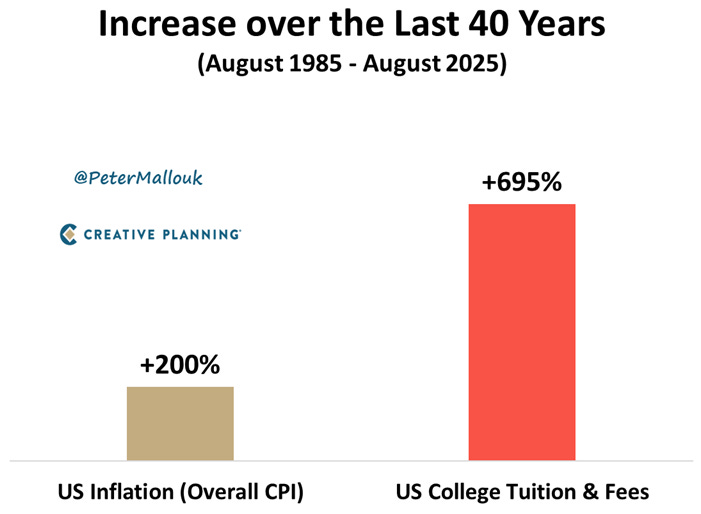

- - Want to talk inflation? Look first at colleges. College tuition is up 695% over the last 40 years ().

-----------

The Fed… What Would You Say You Do Here?

-----------

The Fed… What Would You Say You Do Here?

Yes, the Fed cut rates by .25%, as expected, but…

- -The market was pricing in a little more dovishness, and

- -Remember, the Fed does not control mortgage interest rates.

Keep reading…

“What would you say you do here?”

“What would you say you do here?”

If you listen to the news, you would believe that when the Fed cuts interest rates, it would directly translate to a decline in mortgage rates.

No.

And this avoids important nuance.

Mortgages are predominantly influenced by the market demand for 10-year Treasury bonds, not the Federal Reserve's adjustments to its short-term Fed-Funds rate.

Remember, the Fed does not control mortgage rates. It controls the overnight spending rate between banks. Thus, the Fed has tremendous control over short-term debt (aka the short end of the Yield Curve) and no direct control over long-term debt (aka the long end of the Yield Curve).

The Fed signals to the bond market, and its millions of participants who are all trying to predict the future and decide/guess what price and a given % rate is appropriate for today’s economic risk (put simply). Then all those millions buy/sell the bond at that price and %, which makes the market.

And it is the 10yr Treasury Bond and 30yr mortgage that are competing assets investors buy in our public marketplace, expecting a given return for their expected risk. If investors expect higher risk to the economy, they buy 10-yr Treasuries; if the future seems less risky, they buy 30-yr mortgages (in general). Thus, a reduction in the Federal Funds Rate does not directly or immediately impact 30-year mortgage rates (slightly oversimplified).

But, they do rhyme.

Also, last Fall, when the Fed cut .50% do you remember what happened?

Yup, mortgage rates popped up.

Well, I do declare!… Hey media, don’t act so shocked. You can cool it with the doomer headlines and rhetoric.

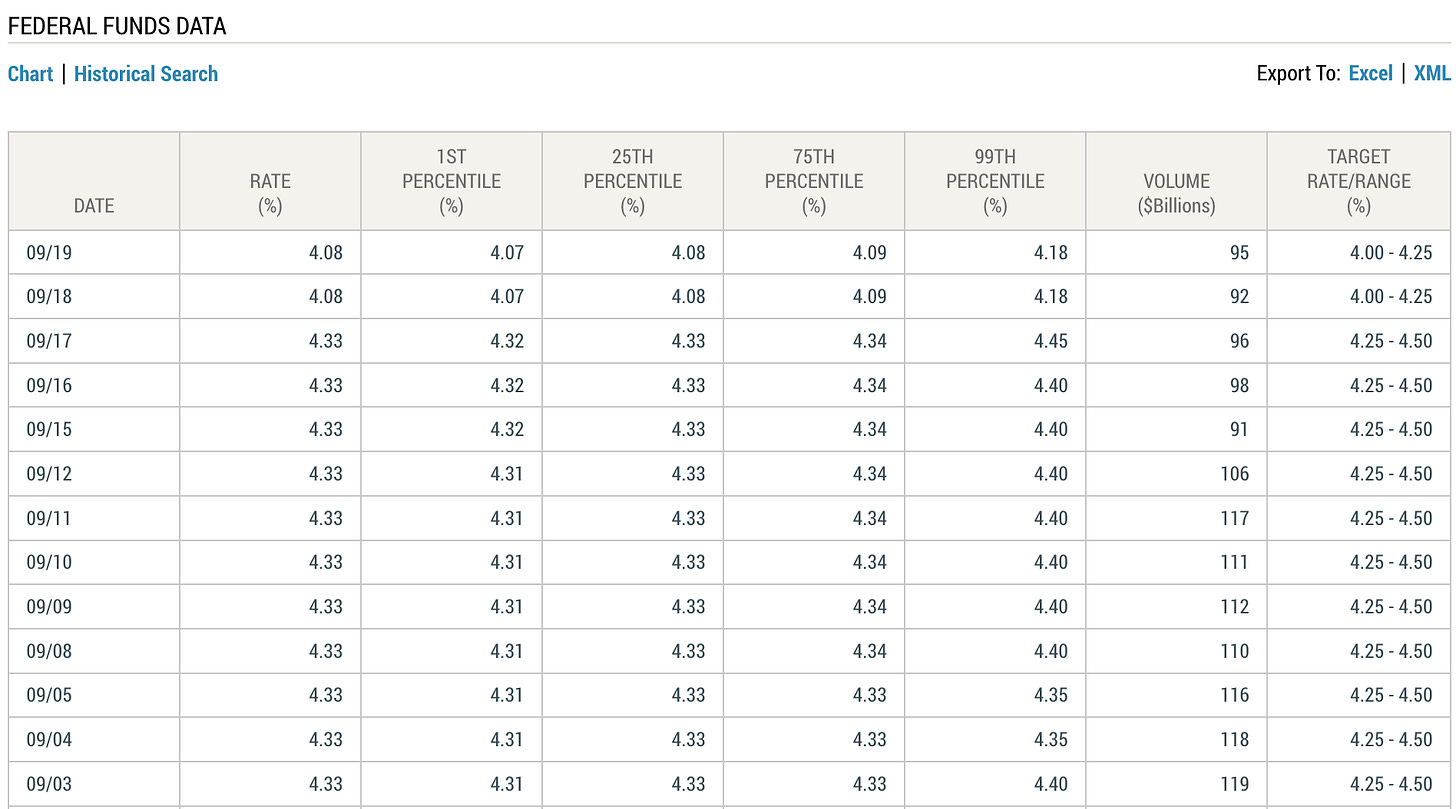

Fun fact, the 10yr Treasury yield rises (and 30-yr mortgages follow, remember) on the day the Fed trimmed rates in about a third of the prior 50+ central bank rate cuts since 1990 (Mishkin). Fed Funds is also a target, not a directive. Even the Fed Funds rate is in constant flux. The new range is 4%-4.25%.

Think of the Fed as a captain on a ship; they can control the boat (Fed Funds Rate) but not the Ocean (the Market).

So, Why Are Rates Higher Today vs Last Week?The market was largely expecting a .25% cut, and thus mortgage rates had already ticked down in anticipation in previous weeks. When the Fed affirmed the market’s assumption, trading of the 10yr Treasury continued on as normal, and in this case, investors sold the 10yr. No reason to buy more, it’s like nothing happened at the Fed b/c that was priced in. Additionally, Powell’s comments during his press conference, which can be more important than the rate decision itself, were not as dovish, ie, there was low certainty in his words that there would be future rate cuts. The latter is important to know.

Fed Is Not DovishIn fact, when answering questions, Powell literally said this was more of a “risk management cut” to hedge against a potential weakening labor market. So the Fed, it seems, has still not gotten religion on labor market weakness, so they begrudgingly cut rates. The market, on the other hand, does believe the labor market is in danger and thus was expecting at least a .25% rate cut ( if not a .5% rate cut) and would have reacted extremely negatively/ volatile if they had not.

In other words, if I may be so crass, the Fed didn’t really want to do it but they needed to do something so the market wouldn’t crash, and because they’re getting so much **** from everyone. The labor market is not solid, so they couldn't use that line anymore with a straight face, but they don't see it as highly problematic either. Even with essentially zero job growth and unemployment slowly ticking up, now 4.3%. It’s interesting.

But, I give them a small shred of credit; this is really the first time the Fed is acknowledging some labor market worries.

The Fed is Still Worried about Tariffs, but Now Admits May not be InflationaryTo be clear, the Fed still fears “inflation in some categories of goods.” But…

Chair Powell now says, “A reasonable base case is that the effects on inflation will be relatively short-lived—a one-time shift in the price.”

They finally admitted it. Not only may tariffs not be inflationary, but that is most likely. However, he did also hedge later in his speech, saying “it is also possible that the inflationary effects could instead be more persistent, and that is a risk to be assessed and managed. Our obligation is to ensure that a one-time increase in the price level does not become an ongoing inflation problem. Their overall effects on economic activity and inflation remain to be seen.”

In fact, Powell said that what’s happening in the labor market may have more to do with immigration rather than tariffs:

“But I would say if you're looking at why employment is doing what it's doing that's much more about the change in immigration. So the supply of workers has, obviously, come way down. There's very little growth, if any, in the supply of workers and at the same time demand for workers has also come down quite sharply and to the point where we see what I've called a curious balance (Powell).”

Fair points. And thank you for the admission that inflation may be sticky, but meaningful reinflation worries should be behind us.

So, looking forward, it is the labor market we should be paying attention to for potential future rate cuts.

But they are not yet willing to admit the labor market is flashing serious red alerts.

Hence, why we only got a .25% cut.

But the market wanted more. Either a .5% cut or a more dovish tone in his comments, signaling future cuts. Neither happened, so mortgage rates have gone up a bit since.

That’s why.

Future Rate Cuts in Question.Importantly, a rate cut in October is NOT certain; in fact, today several Federal Reserve Governors said publicly that it is not.

Case in point: Atlanta Fed President Raphael Bostic said inflation makes him hesitant to support an October cut: "I today would not be moving or in favor of it, but we’ll see what happens (WSJ)."

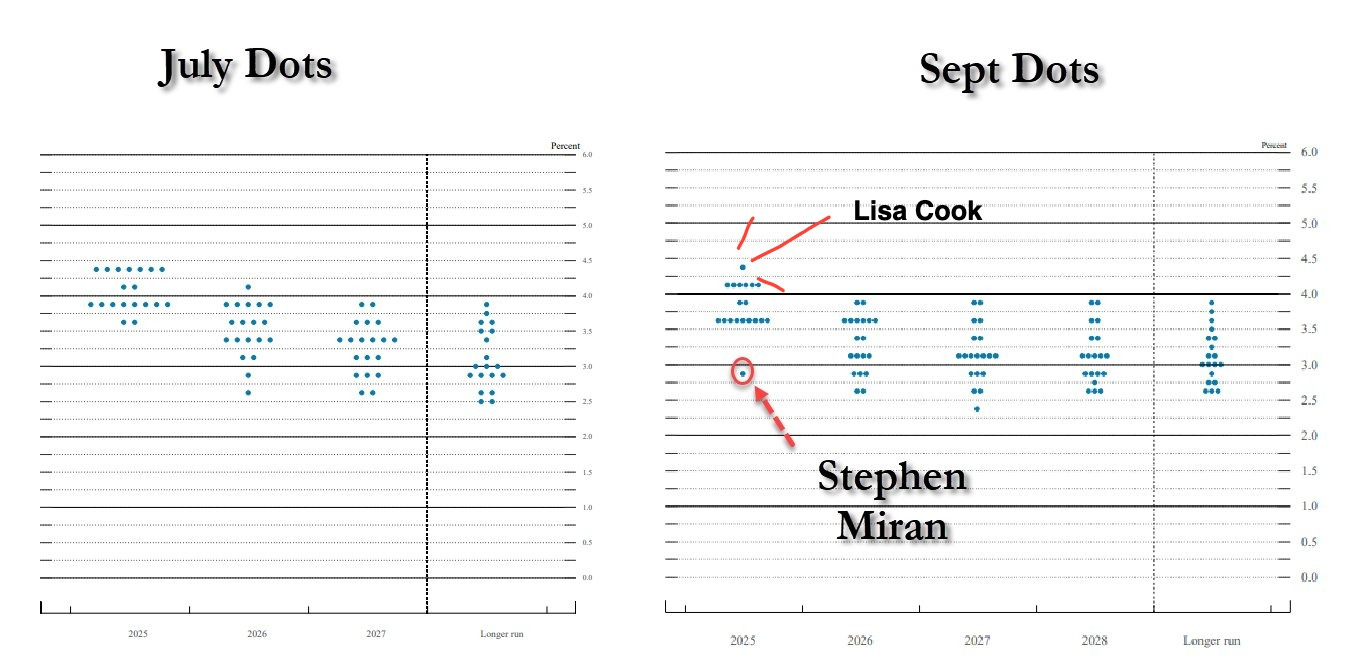

Counterpoint: The President will name a new Fed Chair in May, who will very likely be dovish. And he also recently appointed one Governor, Stephen Miran, who was confirmed just in time to vote last week on the Fed rate cut. The Fed reports individual governors’ votes for rate cuts anonymously via its Dot plot.

Gee, I wonder who this was…(voted for a .5% cut).

AND one voted for a rate hike! (likely Cook, who may be fired soon).

Expect this soon: Treasury Secretary Bessent said today they have interviewed 10 candidates to replace Fed Chair Powell. Mortgage rates could fall faster than expected if they name a replacement before May, and who could act as a . This could move markets and relegate Powell to lame duck status.

Stay tuned.

We are still in a Restrictive Fed Policy Environment.Remember, we are still in a restrictive environment. At this meeting, the Fed “…judged it appropriate at this meeting to take another step toward a more neutral policy stance (Chair Powell)… and continue[d] reducing the size of our balance sheet” (ie, quantitative tightening, not easing). The only outstanding question is, how long will it take to get to neutral? This is what the market will continue to react to.

So, for now, this is as good as it gets for mortgage rates. The 6.2-6.5% range. And, depending on the above, they will continue to tick down. Frustratingly slow. However, the spread (the difference between the interest rate on the 10yr Treasury and the 30yr mortgage) will also continue to compress to normal levels, bringing down rates even without the Fed. A normal spread is about 1.6% today's spread is 2.2%.

We have some room to go.

But again, without the labor market breaking (it may be already, and we don’t know it), the Fed and the 10yr will not signal enough worry to bring down mortgage rates any quicker. It will likely still be 12-18+ months before we get to neutral. And IMO it will be closer to 12.

The labor market will keep cooling as long as long as policy is restrictive. So I woudl urge the Fed to get over its inflation PTSD, and cut rates! The Fed needs to move toward neutral policy and protect the labor market, which has been the best labor market since the late 1990s!

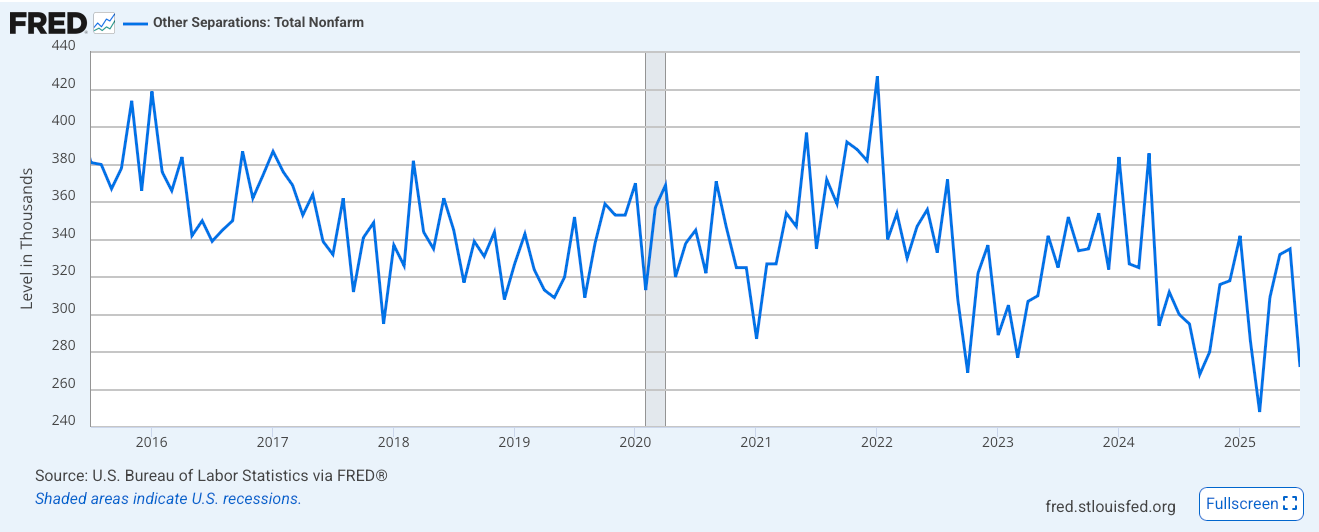

Remember, we still have low historical job separations…

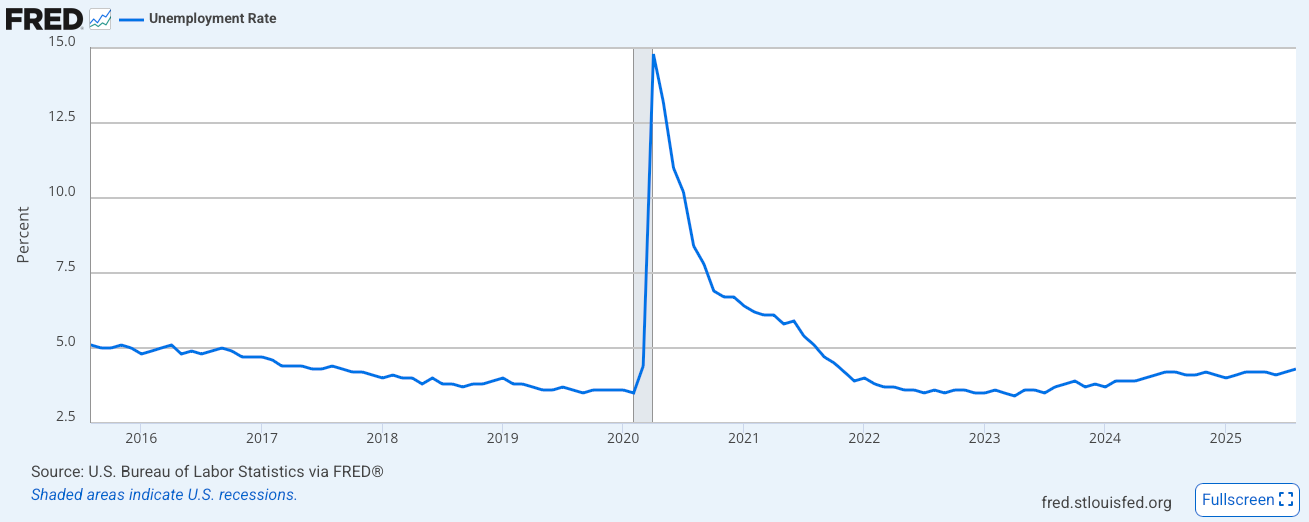

…and low unemployment…

For now….

And now, this….

Tangent Alert! And then I saw this article from the ….

We are NOT in a “loose” (aka accommodative) monetary policy. The Fed is continuing to reduce its balance sheet (aka quantitative tightening) and is keeping rates higher than the RR neutral rate.

Where the hell did you go to economics class?

But I digress….

My Skeptical Take:

I feel like I’ve become some version of a Federal Reserve whisperer, and I really wish that wasn’t the case. I don’t want to think and talk about the Federal Reserve constantly. Much like I bet most people want to see and think about politics all day.

Let’s just get back to neutral policy (let alone loose or accommodated policy) and stop strangling the labor market over unwarranted fears about a one-time tax (aka tariffs) that’s likely not inflationary, which you finally just admitted.

What the **** are we doing here? Let’s let the economy cook!

But even amidst all this hoopla, I still do think we get to 5.xx% rates in the Spring. As long as no crazy politics enters (like Fed Gov Lisa Cook saying we should have a rate hike, what the actual F, Ms Cook??).

My message to the Fed Governors: A year ago, you cut .50% when the unemployment rate was lower, payrolls were in the triple digits, and inflation was higher.

So, why not cut .5% now?

Fed Powell admitted in his speech that the labor market is “somewhat softer…and, the downside risks to employment appear to have risen. In our SEP, the median projection for the unemployment rate is 4.5 percent at the end of this year and edges down thereafter.”

Why not signal future cuts in 2025?

Fun fact they are cutting more, in one new area…Fed jobs.

In the question-and-answer session after his speech, Chair Powell said they would begin a 10% headcount at the Fed, and maybe do more reductions in the future. Bravo. This has been a point of criticism at the Fed. There are 24,000+ employees in total at the Fed/Central Banks (Fed annual report), which begs the question…

…how many economists does it really take to screw in a lightbulb?

Until next time. Stay Curious. Stay Skeptical.

Herzliche Grüße,

-The Skeptical Investor

- Andreas Mueller