Updated about 2 years ago on .

- Real Estate Agent

- Nashville, TN

- 178

- Votes |

- 353

- Posts

The Real Shrinkflation? It's not potato chips. It's....Real Estate.

- Real Estate Agent

- Nashville, TN

Welcome to my weekly article, which I dub 'A Skeptical Dude’s Take on Real Estate,' coming at you live from Nashville, TN. Every week I write a brief, hopefully insightful, dive into real estate and financial markets, for all you tubular dudes and dudettes out there.

What am I listening to? - 90’s Rap, getting my Monday started off right with a little Biggie.

Where am I? - Nashville coffee shop, Frothy Monkey on 51st. Fantastic latte. But the bacon the today was… meh. Y’all gotta make that fresh to order people.

Today We’re Talkin:

- - The Weekly 3 - News and Data to Keep you Informed

- - Rate Cut Downgrade

- - The REAL Shrinkflation

- - In Case you Missed it: The President’s New Housing Proposals are Problematic

- - The Bottom Line

- - Inflation is remaining Stubborn. Prices for everyday things like eggs and shelter are rising faster again (Axios).

- - Broccoli Sprouts are Cancer Fighting? Study shows growing broccoli sprouts at home and consuming them daily counteracts carcinogenic effects of chemicals in food / environment (NIH, Amazon Link).

- - Nashville University Belmont Embracing AI in Education (NBJ).

Today’s Interest Rate: 7.09%

(☝️ .17% from this time last week, 30-yr mortgage)Well, crap. Mortgage interest rates are not “calming down” as I said last week. We are back up above 7%. Bond market did not like the inflation data that came out in the PPIat the end of last week and sold off. Mist!

Several of the ‘large finance houses’ took notice too, GoldmanSachs now sees 3 rate cuts, beginning in June. This is a revision from 4 cuts, beginning in March (and I believe this is their 3rd forecast revision showing fewer and delayed Fed rate cuts).

Shrinkflation

Shrinkflation

There is inflation and now we have “shrinkflation,” where something appears to not be as expensive / the same price but the size of the offering is now smaller/less. Even the President is talking about it, bringing it up both during the Super Bowl and again during his State of the Union address. But this topic has mainly been around consumer goods, “Hey my bag of Doritos is now 10% smaller” etc…. But you know what else is shrinking? New homes.

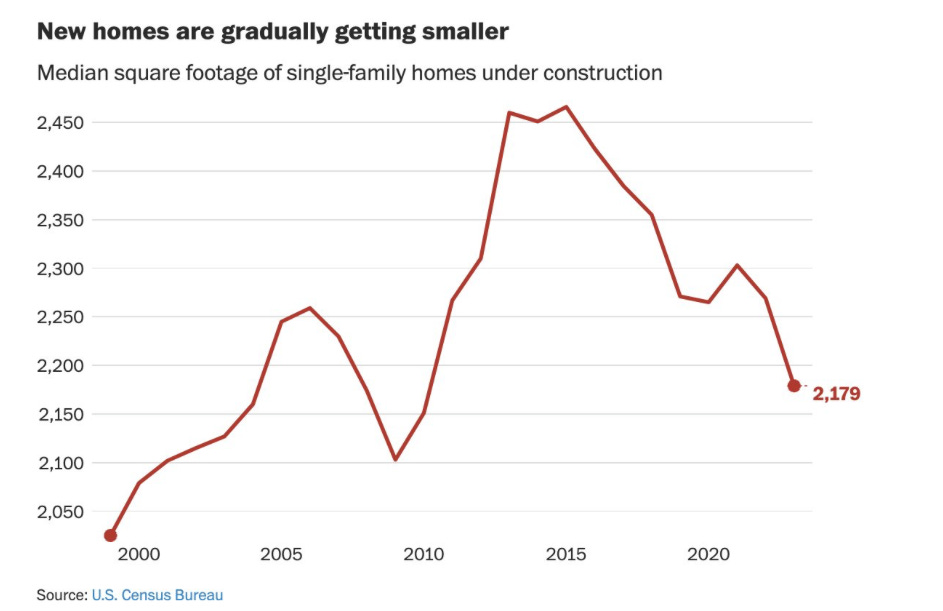

Housing Shrinkflation and Home PricesHomes are also getting smaller, well new homes that is. The median new home size is now 2179 sq/ft, down ~11% since 2013. However, we are seeing more townhomes being built, which often are smaller on average than a single lot / single family home.

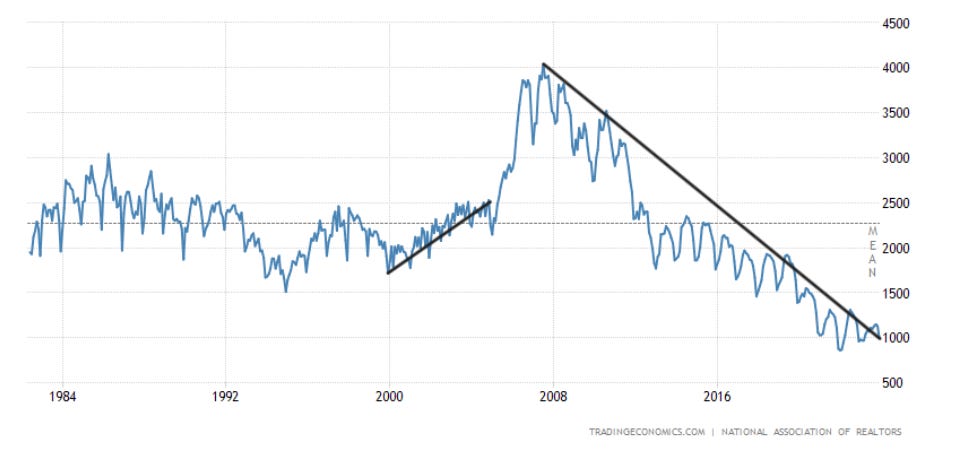

Price are still up however. Why you ask? Supply is low low low. High interest rates body-slammed supply numbers in 2022, as I detailed last week. This was part of the “most significant homes sales crash ever, and still, in 2024, homes sales are trending at all-time lows,” says economist Logan Mohtashami. Active homes for sale normally are 2-2.5 million. Today, we are at less than half that, 1 million. And when we had our last housing crash it was a very unique time. Housing inventory was at 4 million. So we are in a very different time today. This is why the housing market, in terms of home prices, has remained so robust despite high interest rates.

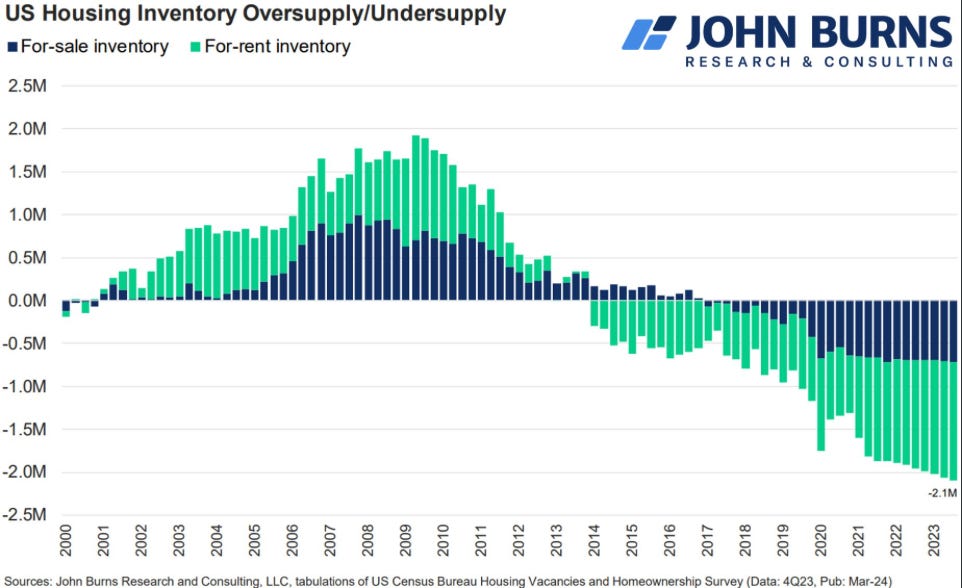

If we want to slow the rapid appreciation of home prices, we need more supply. The cost of homes, rent, shelter etc… is still outpacing wages and most types of goods/services. We see this in the inflation data. We need to tame prices and to do that we need more supply. One year ago, housing economists said the U.S. housing market was “undersupplied by 1.7 million homes.” Now, they say that number is 2.1 million.

Home prices continue to appreciate too rapidly. I say this as a real estate investor, who benefits from home price appreciation. But I have long term thinking, not quarter to quarter. The last few years is not normal. For a long term healthy market (which I would argue is most important) we should prefer a more steady / predictable price appreciation, not something this rapid. Something will break. I don’t know what, but something will.

Can we roll back prices?In short, no. And you DON’T want that. For home prices to disinflate back to 2019 levels, home prices would have to crash 41%. Millions of homeowners would then be underwater on their mortgage - owing more than it is worth - and would likely foreclose / declare bankruptcy, creating a credit crisis, unemployment would spike to 10%+ and on and on… No, no the price of homes, and really everything we pay for, is here to stay. This is the long-term price of inflation (no pun intended). What we should want is for the rate of price appreciation (inflation) to level off in the 2-4% / yr range. That’s what the Fed is trying to do for total inflation (their number is 2% but that may be difficult for a while) by raising their Fed Funds rate.

You want to know what the real shrinkflation is? It’s combining the inflation numbers with the higher cost of credit/borrowing. Remember, the Fed raised rates because of high inflation. So both things were happening at the same time since 2022. So, for example, rather than the peak of 9% inflation last year, adding the cost of credit on top of that we actually peaked at 18% last year. This cost of debt comes through where people have to borrow to afford the item, like a car, or business Capex and of course, a home. This explains why consumer sentiment has remained depressed despite unemployment being extremely low and inflation is down dramatically (9% to 3.2%).

Y’all likely know this already. You have seen it for 3 years in your daily lives, when you go to the store, or buy a used car, try to buy a home, order parts for your widget company etc…So in summary, prices are here to stay and we need more homes to be built, likely catalyzed by proper incentives / less onerous regulation.

Well all that Sucks, What’s the Positive?It should be said, we are extremely fortunate here in the US. We have this thing called the 30-yr fixed mortgage, primarily because of the structure of the mortgage market with government backed mortgage securities. And since the qualified mortgage law in 2010, these loans have remained solid, and thus, so has the mortgage securities market. I don’t say this often, but good job U.S. Congress / government! (Better late than never, full disclosure I was working in Congress at this time).

So, unlike the 2008 Great Financial Crisis, today we don’t have high homeowner distress, which result in distressed sales and home price cliff dives. This dearth of distress is another reason today’s home prices will remain elevated to stable, despite higher mortgage rates. What could pierce the housing market armor? Unemployment spiking up, it’s the great equalizer. This is why the dreaded recession is often talked about, it usually portends high unemployment, which is an economic killer.

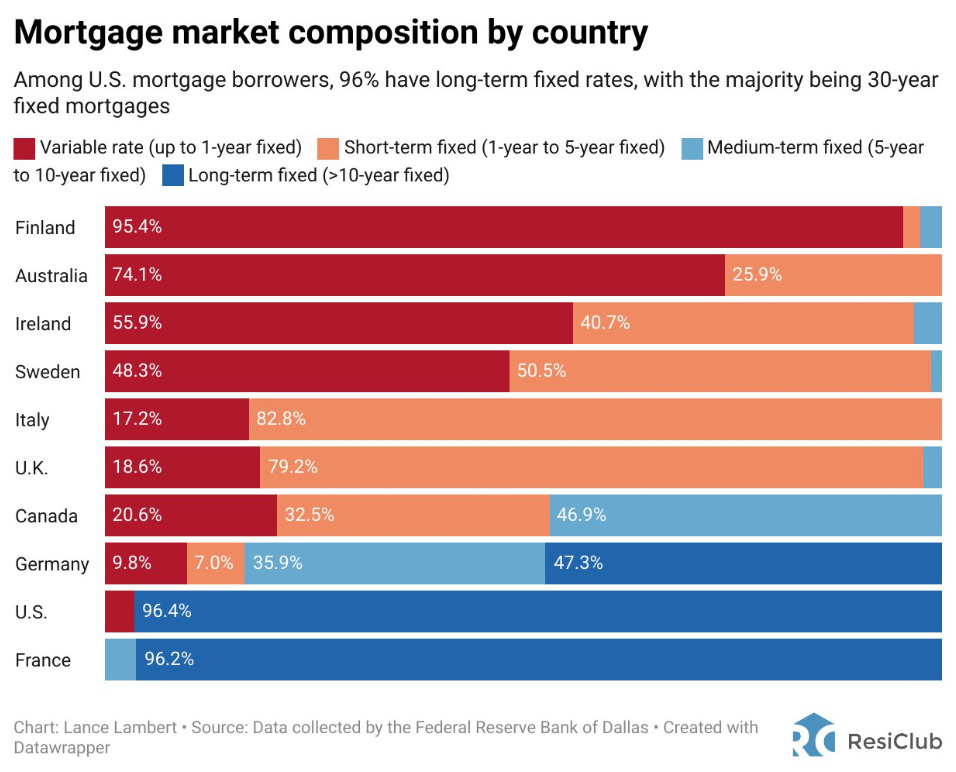

If you were in most of the other highly developed countries in the world, you would likely have a variable mortgage rate that would suddenly change on you when interest rates change, the Mr. Hyde of mortgages. “In the UK ‘more than a million households will see a significant jump in monthly payments’ this year as ‘the next batch of UK homeowners to have their mortgages repriced are preparing to make personal sacrifices”(Bloomberg). Imagine your mortgage going from $1500 to $3000? Just look at the % of mortgages in other countries that have variable rates:

God Bless America.

In Case you Missed it: The President’s New Housing Proposals are ProblematicSince it was a big f*$%ing deal headline, I’m re-linking my analysis of the President’s housing proposals he unveiled last week during the State of the Union. Worth a read for all you prospective homeowners/investors.

Bottom Line

There is always reason to be positive!

The Skeptics Take: America is Amazing. Some countries may have faster growth in good times, but über-crash in bad times. Long-term fixed debt calms the short term market volatility. So while things may seem difficult right now, remember the US is doing absolutely fantastic compared to everyone else. Hell, ~99% of mortgages in United Kingdom, Finland, Australia, Ireland, and Canada are short term, variable debt. Verrückt! Times may seem tough right now. Everything costs more than just 1, 2, 3 years ago. And not just a little, a lot! But unemployment is at record lows, literally the lowest ever. And despite high inflation and the necessary reaction of high rates (even though it was the government that caused the inflation in the first place) the economy is humming, stock market up, home prices for homeowners have contributed immensely to their net worth, technology is doing amazing things and providing ample opportunity for those born into less fortunate situations to escape and succeed.

Life is good. And as my dad used to say, “this too shall pass.”

In other words, Stay Skeptical but positive y’all. There is always opportunity.

Most Interesting Tweet(s) of the WeekKids these days! Looks like a helicopter parent situation. Pull up those bootstraps little birdie.

That’s it for this week. If you are interested in digging deeper into any of these ideas or just want to talk real estate investing - which I always love doing - don’t hesitate to reach out. You can email me direct, I try to answer all the emails I get personally. [email protected]

Again, stay skeptical, all you dudes and dudettes.

Herzliche Grüße

-Andreas

* The preceding has been my opinion only, the views are my own, and are intended for educational and entertainment purposes only and does not constitute financial advice.

- Andreas Mueller