All Forum Posts by: Ken M.

Ken M. has started 153 posts and replied 1785 times.

Post: US Pending Home Sales Plunge Most In 30 Months - (Don't Shoot The Messenger)

Post: US Pending Home Sales Plunge Most In 30 Months - (Don't Shoot The Messenger)

- Investor

- Zero Down Specialist

- Posts 1,836

- Votes 1,037

Thursday, May 29, 2025 - 07:09 AM By Tyler Durden

US Pending Home Sales plunged 6.3% MoM in April - far more than the 1.0% MoM decline expected (below all estimates) - and the biggest MoM drop since September 2022...

Source: Bloomberg

Dragging the Index of Pending Home Sales back down near record lows...

Source: Bloomberg

Sales fell in all four regions with the West experiencing the biggest drop of 8.9%.

As a reminder, pending home sales are often looked to as a leading indicator of existing-home purchases given properties typically go under contract a month or two before they’re sold.

*******************************

it is all about mortgage rates," said NAR Chief Economist Lawrence Yun.

My Answer: Nonsense, it's all about prices are far too high for the debt to income ratio of buyers.

You could cut rates to zero and people still could not afford these prices. He is an economist, why doesn't he tell the truth? What's behind this gibberish?

Our first family home cost us $78,000 @ 8% ($572.34 a month PI) interest and

the same house now is listed at over $1,000,000 @ 6.78% ($6,504.74 a month PI) and then there is property tax (waaaay out of line), and insurance.

On a related inflation scale it would be $228,203 @ 6.78% ($1,484.64 a month PI)

NAR deserves to go away. Misinformation.

Post: Foreclosing before probate opens?

- Investor

- Zero Down Specialist

- Posts 1,836

- Votes 1,037

Quote from @Sean Dougherty:

Quote from @Ken M.:

Quote from @Sean Dougherty:

My question is this:

can they foreclose BEFORE the probate opens?

Thanks Ken I appreciate the reply. Considering that they can foreclose even before probate is opened, this puts the airs in more urgency to sell before the foreclosure.

Are the heirs able to sell the home if there is no probate opened and PR assigned?

There are actually two different things.

1. Who owns the property

2. Who is on the loan

These are very, very different.

"Who can sell a property"

Only people on title, or

someone with power of attorney if the owner is still alive, or

if the property is in a trust, the trustee can sell, or

someone appointed by probate court.

If it it a Deed of Trust state, the lender can sell under certain circumstances, such as non-payment, to protect their interests. It is a process that requires following a specific set of steps determined by each state.

A quick search shows Hawaii is a Mortgage state. That means if the property is in Hawaii, the lender must sue to foreclose, which is a much longer process. A personal representative can be appointed by probate court even while the lender is going through that process. The property belongs to the estate and can be sold, even when in foreclosure, until the lender successfully completes a foreclosure sale.

It isn't hard for a relative to get appointed by the court and then they have legal right to sell along with the legal responsibilities of probating the estate

Many lenders will accept payment from relatives living in the property as though it were from the borrower

The clock starts ticking from when the first payment was missed.

Any missed payments along the way get added to the reinstatement amount.

Those debts do not go away, they just get added to how much you need to make the lender happy again.

Here is the procedure for Hawaii

https://www.alllaw.com/articles/nolo/foreclosure/hawaii-fore...

Post: Subto affecting seller's credit

- Investor

- Zero Down Specialist

- Posts 1,836

- Votes 1,037

Quote from @Patrick Roberts:

Quote from @Noah Laker:

Real estate broker here — I facilitated a subto transaction in 2023 with a VA loan in California.

The seller of that property now wants to buy a new home. However, the lender is including her payment on the property she sold, because the loan is still in her name.

I was always told that “after 12 months of payments through a third party payment processor, the loan will fall off of the seller’s credit.” Pace Morby himself told me this at a conference.

What am I missing? How do we fix this?

This is not accurate at all. A couple moving parts here:

VA Loans, entitlement, and encumberance: as long as the original loan is in existence, it will affect the original veteran's VA entitlement for VA loans. If the loan defaults, this will directly impact the original veteran as well. The only way around this is to have the loan formally assumed by another veteran who has sufficient entitlement (the loan transfers to the new veteran's entitlement). This is also is considered a federal debt and being in default on it will affect the original veteran in other ways as well, such as being ineligible for forbearance and other loss mitigation programs on any other loans.

Credit report: this loan will continue to report on the original borrower's credit report until the creditor reports it paid off. You can try sending the bureaus a copy of the contractual agreement for the subto buyer to show that they are now legally obligated on the debt, but I have not seen any of the four bureaus accept this. This is similar to a divorce situation where one party is awarded the property and debt, but the loan remains as a trade on the other party's credit report. Even though the original party may no longer be responsible for the debt per court order, their credit is still on the line, and nonperformance on the trade in question will wreck the original borrower's credit. I have seen this happen several times, and I have seen it disputed/challenged at the bureaus, and I have seen this dispute fail every time. Anecdotal, but just my experience.

Impacts on future borrowing ability: this will vary by loan type. Fannie/Freddie have provisions for contingent liabilities that allow lenders to disregard debts that are the primary responsibility of other parties after the other party has paid the debt in question for 12 consecutive months. You will need bank statements or copies of the checks to prove this. FHA and VA have different rules. With VA, if there is any chance that you could be held to be obligated on the debt, then it gets included in DTI/residual income. I cant imagine that any competent lender will risk a buyback by allowing a subto agreement to suffice as proof that the original borrower is no longer responsible for the debt.

Guaranties and Insurance: VA and FHA loans are guaranteed/insured by agencies of the federal government. Subto's on these loans give the government standing to file suit against the parties on the loan if/when these go bad. The govt has been asleep at the wheel for a while with respect to this, but that is rapidly changing. The new administration is proactively going after these loans. Pay attention to what Pulte (FHFA director) and the other new directors are saying about fraud in the mortgage market. They're on the hunt for this kind of thing. Furthermore, if a VA or FHA loan has even gone into a workout and has received a partial claim through FHA insurance/VASP, expect the loan to be accelerated in the next 18 months if there has been a change of ownership (like in a subto deal). The servicers/subservicers on these loans are taking the brunt of this and are looking for ways to get bad loans off their books asap. I have heard directly from two different subservicer executives that they are proactively running title scrubs on these loans annually and will use the Due on Sale clause to accelerate these loans.

Newer development with direct lenders: I have seen a couple instances now where lenders are deeming subto transactions as fraudulent and are declining refinances/new loans for the parties involved in these deals. This is more anecdotal and less likely to be widespread, but just know that it is on the radar.

.

2nd - Your comment: "I have heard directly from two different subservicer executives that they are proactively running title scrubs on these loans annually and will use the Due on Sale clause to accelerate these loans."

Can't get clearer than that. In fact it's like the city of Walla Walla, a city so nice they say it twice.

Post: Subto affecting seller's credit

- Investor

- Zero Down Specialist

- Posts 1,836

- Votes 1,037

Quote from @Patrick Roberts:

Quote from @Noah Laker:

Real estate broker here — I facilitated a subto transaction in 2023 with a VA loan in California.

The seller of that property now wants to buy a new home. However, the lender is including her payment on the property she sold, because the loan is still in her name.

I was always told that “after 12 months of payments through a third party payment processor, the loan will fall off of the seller’s credit.” Pace Morby himself told me this at a conference.

What am I missing? How do we fix this?

This is not accurate at all. A couple moving parts here:

VA Loans, entitlement, and encumberance: as long as the original loan is in existence, it will affect the original veteran's VA entitlement for VA loans. If the loan defaults, this will directly impact the original veteran as well. The only way around this is to have the loan formally assumed by another veteran who has sufficient entitlement (the loan transfers to the new veteran's entitlement). This is also is considered a federal debt and being in default on it will affect the original veteran in other ways as well, such as being ineligible for forbearance and other loss mitigation programs on any other loans.

Credit report: this loan will continue to report on the original borrower's credit report until the creditor reports it paid off. You can try sending the bureaus a copy of the contractual agreement for the subto buyer to show that they are now legally obligated on the debt, but I have not seen any of the four bureaus accept this. This is similar to a divorce situation where one party is awarded the property and debt, but the loan remains as a trade on the other party's credit report. Even though the original party may no longer be responsible for the debt per court order, their credit is still on the line, and nonperformance on the trade in question will wreck the original borrower's credit. I have seen this happen several times, and I have seen it disputed/challenged at the bureaus, and I have seen this dispute fail every time. Anecdotal, but just my experience.

Impacts on future borrowing ability: this will vary by loan type. Fannie/Freddie have provisions for contingent liabilities that allow lenders to disregard debts that are the primary responsibility of other parties after the other party has paid the debt in question for 12 consecutive months. You will need bank statements or copies of the checks to prove this. FHA and VA have different rules. With VA, if there is any chance that you could be held to be obligated on the debt, then it gets included in DTI/residual income. I cant imagine that any competent lender will risk a buyback by allowing a subto agreement to suffice as proof that the original borrower is no longer responsible for the debt.

Guaranties and Insurance: VA and FHA loans are guaranteed/insured by agencies of the federal government. Subto's on these loans give the government standing to file suit against the parties on the loan if/when these go bad. The govt has been asleep at the wheel for a while with respect to this, but that is rapidly changing. The new administration is proactively going after these loans. Pay attention to what Pulte (FHFA director) and the other new directors are saying about fraud in the mortgage market. They're on the hunt for this kind of thing. Furthermore, if a VA or FHA loan has even gone into a workout and has received a partial claim through FHA insurance/VASP, expect the loan to be accelerated in the next 18 months if there has been a change of ownership (like in a subto deal). The servicers/subservicers on these loans are taking the brunt of this and are looking for ways to get bad loans off their books asap. I have heard directly from two different subservicer executives that they are proactively running title scrubs on these loans annually and will use the Due on Sale clause to accelerate these loans.

Newer development with direct lenders: I have seen a couple instances now where lenders are deeming subto transactions as fraudulent and are declining refinances/new loans for the parties involved in these deals. This is more anecdotal and less likely to be widespread, but just know that it is on the radar.

.

1st - Your comment: "I have heard directly from two different subservicer executives that they are proactively running title scrubs on these loans annually and will use the Due on Sale clause to accelerate these loans."

Can't get clearer than that. In fact it's like the city of Walla Walla, a city so nice they say it twice.

Post: The Cycle of Market Emotions in Smokies Short Term Rentals: Where we are

- Investor

- Zero Down Specialist

- Posts 1,836

- Votes 1,037

Quote from @Collin Hays:

We're headed that way in about 6 weeks. What I'm concerned about is the all the negative coverage on the news between Gatlinburg and Ashville about storm damage and how it affects travel. As a result we're circumventing Gatlinburg and going east through Knoxville. Hate to miss Gatlinburg, though.

I wonder how many others have the same concerns about storm damage, availability of lodging, gas and food in the area and how it affects your local STRs.

Post: Home Prices Are Falling

- Investor

- Zero Down Specialist

- Posts 1,836

- Votes 1,037

Quote from @Michael Carbonare:

𝐇𝐨𝐦𝐞 𝐏𝐫𝐢𝐜𝐞𝐬 𝐀𝐫𝐞 𝐅𝐚𝐥𝐥𝐢𝐧𝐠. 𝐀𝐫𝐞 𝐘𝐨𝐮 𝐒𝐭𝐢𝐥𝐥 𝐖𝐚𝐢𝐭𝐢𝐧𝐠?

For the first time in over 2 years, home prices in the top 20 U.S. markets are declining.

That “perfect time” you’ve been waiting for? It's here.

Markets like San Diego, Portland, and Phoenix are already seeing drops — and more are expected to follow.

Here’s what that means for you:

Motivated sellers

More negotiable deals

Prime opportunities for creative strategies. Sure, cash on hand makes things easier. But you don't need deep pockets and an 800 FICO.

But many new investors? Stuck. Scared. Watching.

If you've been sitting on the sidelines, unsure how to start, this market shift is your invitation in. There are many members here on BP that are happy to share their experience and know how. You only need to ask.

Home Prices Are Falling Yes, they are.

Post: Sad way to start out but starting out nonetheless.

- Investor

- Zero Down Specialist

- Posts 1,836

- Votes 1,037

Quote from @Chelsea Price:

If it weren't for the love & sacrifices of my now deceased grandparents (I just lost my last living one 2 weeks ago) I'd still be the average American struggling with credit card debt. Thanks to my inheritances I've been able to honor their memory by paying off all my debts FIRST and then proceeding with other ventures. I have no advice or suggestions for you. Just leaving you with my experience that it feels really darn good knowing I did what they would have wanted me to do. I sleep well at night knowing I don't owe anyone (I paid off our mortgage, credit cards, AND 3 cars!) and I'm now free to do whatever, wherever I want.

.

I agree with @Chelsea Price:

There are only 5 kinds of very bad debt.

1. Credit Card Debt

2. School loan debt

3. See #1

4. See #2

5. See #'s 1 and 2

They will ruin your life.

Okay, owing your bookie is the very worst, but that means you have will have a very short life.

Oh, and stop drinking soda, that makes debt even worse with bad health.

Post: Foreclosing before probate opens?

- Investor

- Zero Down Specialist

- Posts 1,836

- Votes 1,037

Quote from @Sean Dougherty:

My question is this:

can they foreclose BEFORE the probate opens?

Post: Subto affecting seller's credit

- Investor

- Zero Down Specialist

- Posts 1,836

- Votes 1,037

Quote from @Noah Laker:

Quote from @Ken M.:

Quote from @Noah Laker:

Real estate broker here — I facilitated a subto transaction in 2023 with a VA loan in California.

The seller of that property now wants to buy a new home. However, the lender is including her payment on the property she sold, because the loan is still in her name.

I was always told that “after 12 months of payments through a third party payment processor, the loan will fall off of the seller’s credit.” Pace Morby himself told me this at a conference.

What am I missing? How do we fix this?

.

Your comment "after 12 months of payments through a third party payment processor, the loan will fall off of the seller’s credit.” Pace Morby himself told me this"

Let's just say "he has been known to be absolutely wrong". More often than you realize.

However, I guess the question is, is it intentional in order to get people to sign up for his group or is it lack of integrity or lack or experience? I guess it doesn't matter now, the damage is done.

You know, borrowers sue over false promises like that.

By the way, why ask those kinds of questions here? Why not at his community instead? oh, you've heard you get deleted from the group if you ask those kinds of questions. Yeah, word has gotten out. Sorry you had to learn this way.

Negative and unhelpful. I also asked Pace’s community on Facebook.

Yeah, you sure got me on that one

Name : Pace Jordan Morby

ADDITIONAL COMPLAINT INFORMATION

| TYPE | COMPLAINT ID | OUTCOME | CLOSED DATE (IF CLOSED) |

|---|---|---|---|

| Disciplined | 2019-04542 | Legal – Revoked | 2019-12-09 |

| Disciplined | 2019-00552 | Legal - Revocation | 2019-07-08 |

| Disciplined | 2019-01410 | Legal – Revoked | 2019-07-26 |

| Disciplined | 2019-01649 | Legal - Revocation | 2019-09-03 |

| Disciplined | 2018-05708 | Legal - Revocation | 2019-04-25 |

| Disciplined | 2018-21 | Legal - Revocation | 2019-04-25 |

| Disciplined | 2018-4172 | Legal - Revocation | 2019-04-26 |

https://www.biggerpockets.com/forums/79/topics/1147286-is-pa...

https://www.biggerpockets.com/forums/50/topics/1225630-due-o...

Sub To at work

For all of you lurkers

Beware get real training if you are going to do "Subject To". Pace Morby is not the guy, In my humble opinion by what I've seen him publish.

@Jay Thomas: Sorry buddy, your comments "if the seller stops paying, you might be responsible, and you'll take on any existing problems with the property and mortgage. Also, you won't have full ownership rights until the mortgage is completely paid off."

are very, very wrong. You're going to get someone sued with that advice.

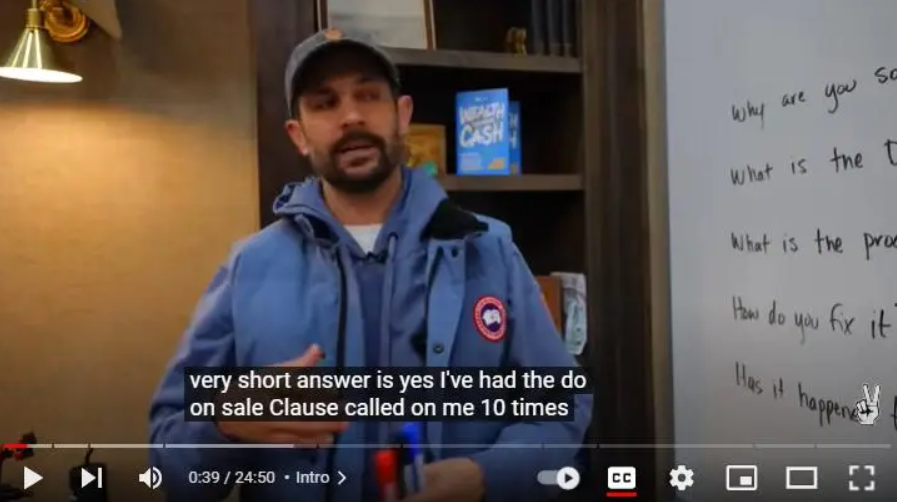

Anyway here is what Pace Morby is saying

Click to enlarge

What he is doing isn't working properly. In 30 years I had the Due on Sale called twice. Once in 2008 and once in 2020. But this guy has had it called 10 times recently. Very scary.

"Yes, I've had the Due on sale clause called on me 10 times"

The liability of having the Due on Sale called is that you have 30 days to pay off the loan in full or the foreclosure process can begin.

Once that gets filed, that puts a foreclosure on the seller's credit report and they can sue you. A lawsuit costs between $25,000 and $125,000 and runs about a year and a half and puts you under scrutiny for everything you do and have done for the last 3 years.

Only the foolish take this lightly.

Post: Foreclosing before probate opens?

- Investor

- Zero Down Specialist

- Posts 1,836

- Votes 1,037

Quote from @Sean Dougherty:

Can a lender foreclose on a home if the owner is deceased and probate has not been opened? Or is it required that probate be initiated, and PR's assigned before the foreclosure can take place?

It's a rather technical problem that an attorney can help you with.