All Forum Posts by: Ken M.

Ken M. has started 149 posts and replied 1757 times.

Post: Subto affecting seller's credit

Post: Subto affecting seller's credit

- Investor

- Zero Down Specialist

- Posts 1,807

- Votes 1,027

Quote from @Noah Laker:

Quote from @Ken M.:

Quote from @Noah Laker:

Real estate broker here — I facilitated a subto transaction in 2023 with a VA loan in California.

The seller of that property now wants to buy a new home. However, the lender is including her payment on the property she sold, because the loan is still in her name.

I was always told that “after 12 months of payments through a third party payment processor, the loan will fall off of the seller’s credit.” Pace Morby himself told me this at a conference.

What am I missing? How do we fix this?

.

Your comment "after 12 months of payments through a third party payment processor, the loan will fall off of the seller’s credit.” Pace Morby himself told me this"

Let's just say "he has been known to be absolutely wrong". More often than you realize.

However, I guess the question is, is it intentional in order to get people to sign up for his group or is it lack of integrity or lack or experience? I guess it doesn't matter now, the damage is done.

You know, borrowers sue over false promises like that.

By the way, why ask those kinds of questions here? Why not at his community instead? oh, you've heard you get deleted from the group if you ask those kinds of questions. Yeah, word has gotten out. Sorry you had to learn this way.

Negative and unhelpful. I also asked Pace’s community on Facebook.

Yeah, you sure got me on that one

Name : Pace Jordan Morby

ADDITIONAL COMPLAINT INFORMATION

| TYPE | COMPLAINT ID | OUTCOME | CLOSED DATE (IF CLOSED) |

|---|---|---|---|

| Disciplined | 2019-04542 | Legal – Revoked | 2019-12-09 |

| Disciplined | 2019-00552 | Legal - Revocation | 2019-07-08 |

| Disciplined | 2019-01410 | Legal – Revoked | 2019-07-26 |

| Disciplined | 2019-01649 | Legal - Revocation | 2019-09-03 |

| Disciplined | 2018-05708 | Legal - Revocation | 2019-04-25 |

| Disciplined | 2018-21 | Legal - Revocation | 2019-04-25 |

| Disciplined | 2018-4172 | Legal - Revocation | 2019-04-26 |

https://www.biggerpockets.com/forums/79/topics/1147286-is-pa...

https://www.biggerpockets.com/forums/50/topics/1225630-due-o...

Sub To at work

For all of you lurkers

Beware get real training if you are going to do "Subject To". Pace Morby is not the guy, In my humble opinion by what I've seen him publish.

@Jay Thomas: Sorry buddy, your comments "if the seller stops paying, you might be responsible, and you'll take on any existing problems with the property and mortgage. Also, you won't have full ownership rights until the mortgage is completely paid off."

are very, very wrong. You're going to get someone sued with that advice.

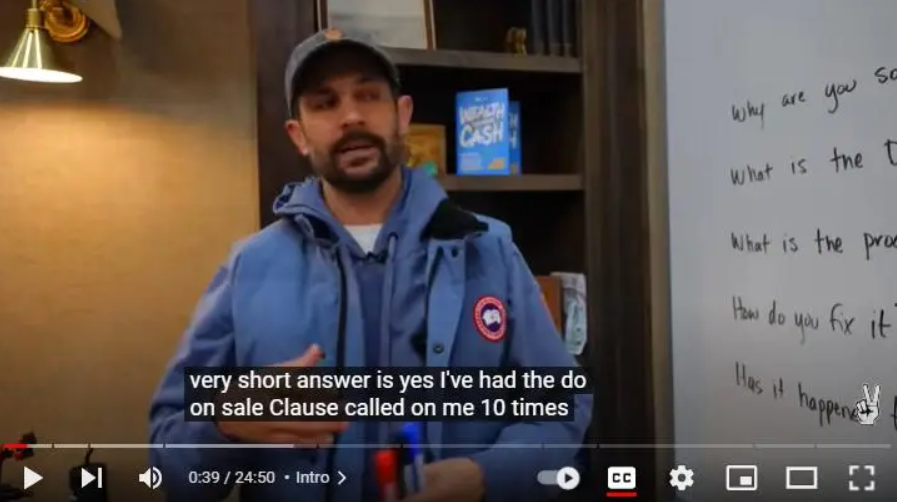

Anyway here is what Pace Morby is saying

Click to enlarge

What he is doing isn't working properly. In 30 years I had the Due on Sale called twice. Once in 2008 and once in 2020. But this guy has had it called 10 times recently. Very scary.

"Yes, I've had the Due on sale clause called on me 10 times"

The liability of having the Due on Sale called is that you have 30 days to pay off the loan in full or the foreclosure process can begin.

Once that gets filed, that puts a foreclosure on the seller's credit report and they can sue you. A lawsuit costs between $25,000 and $125,000 and runs about a year and a half and puts you under scrutiny for everything you do and have done for the last 3 years.

Only the foolish take this lightly.

Post: Foreclosing before probate opens?

- Investor

- Zero Down Specialist

- Posts 1,807

- Votes 1,027

Quote from @Sean Dougherty:

Can a lender foreclose on a home if the owner is deceased and probate has not been opened? Or is it required that probate be initiated, and PR's assigned before the foreclosure can take place?

It's a rather technical problem that an attorney can help you with.

Post: Subto affecting seller's credit

- Investor

- Zero Down Specialist

- Posts 1,807

- Votes 1,027

Quote from @Noah Laker:

Real estate broker here — I facilitated a subto transaction in 2023 with a VA loan in California.

The seller of that property now wants to buy a new home. However, the lender is including her payment on the property she sold, because the loan is still in her name.

I was always told that “after 12 months of payments through a third party payment processor, the loan will fall off of the seller’s credit.” Pace Morby himself told me this at a conference.

What am I missing? How do we fix this?

.

Your comment "after 12 months of payments through a third party payment processor, the loan will fall off of the seller’s credit.” Pace Morby himself told me this"

Let's just say "he has been known to be absolutely wrong". More often than you realize.

However, I guess the question is, is it intentional in order to get people to sign up for his group or is it lack of integrity or lack or experience? I guess it doesn't matter now, the damage is done.

You know, borrowers sue over false promises like that.

By the way, why ask those kinds of questions here? Why not at his community instead? oh, you've heard you get deleted from the group if you ask those kinds of questions. Yeah, word has gotten out. Sorry you had to learn this way.

Post: Foreclosure after Bankruptcy

- Investor

- Zero Down Specialist

- Posts 1,807

- Votes 1,027

Quote from @Sean Dougherty:

Hi all,

I have numerous leads where the homeowners declared chapter 7 bankruptcy 5-10 years ago. Since then, they have severed all ties with the homes. And only recently has the foreclosure proceedings begun.

The lender is not looking to collect any debt from them as that has all been relieved. The lender is simply looking to repossess the property through the foreclosure process.

Are the homeowners at all affected if the home forecloses at this point? Will their credit be affected? Could they short sale their home at this time?

For clarification on this issue, look up "Unless they "re-affirmed" the debt". If they reaffirmed the debt, they have taken over the mortgage debt in this case, post filing and only their none mortgage debt is discharged.

In situations where a debtor wishes to retain the property (such as in a homestead exemption), and can afford the payments, he can with court approval, begin making payments on the property again and keep the property.

There are many variations of using chapter7 and chapter 13 to remove debt but keep the primary home.

While bankruptcy has federal rules, there are also state rules and above all, the court allows for lenders and borrowers to have considerable latitude in dealing with the problem, depending on what each side wants to accomplish. As odd as it may sound "it's all negotiable" and as long as other creditors don't object and the rules are followed, the court will generally agree.

Post: Tax Inquiry: $12k to replace AC

- Investor

- Zero Down Specialist

- Posts 1,807

- Votes 1,027

Quote from @Terri P.:

Thank you everyone for your input! I got another bid for under 10k with a 3 year warranty on labor, 10 years on parts. I am replacing the entire system (Goodman 2-ton 13.4 SEER2 Gas/Electric). This doesn’t include any needed ductwork (TBD). I replaced the capacitor last year for almost $500 (because it only goes kaput during a heatwave and you need it asap). I don’t want to spend more money on a control board for something else to break during another heat wave. All of my renters are working professionals and I try to treat them (& my property) well. This is a small single family home and to answer someone, rent is $2300 and cashflow $500 (before this new HVAC system).

Post: Foreclosure after Bankruptcy

- Investor

- Zero Down Specialist

- Posts 1,807

- Votes 1,027

Quote from @Sean Dougherty:

Hi all,

I have numerous leads where the homeowners declared chapter 7 bankruptcy 5-10 years ago. Since then, they have severed all ties with the homes. And only recently has the foreclosure proceedings begun.

The lender is not looking to collect any debt from them as that has all been relieved. The lender is simply looking to repossess the property through the foreclosure process.

Are the homeowners at all affected if the home forecloses at this point? Will their credit be affected? Could they short sale their home at this time?

Yep, the foreclosure will show on their credit report if a foreclosure is filed. It's still listed in their name even if previously discharged in bankruptcy. They have to add a note to their credit report that the foreclosure was previously included in the bankruptcy for lenders to understand that.

Your comment "Since then, they have severed all ties with the homes" I take that to mean they no longer live there. Well, someone is paying property taxes or the county would raise a fuss.

Can they short sale: the bankruptcy only deals with pre-filing debt. Any payments due after the filing are still due. 5 years of missed payments is a big chunk of money. Unless they "re-affirmed" the debt, (which they would be advised against by their attorney unless there were extenuating circumstances), and take responsibility for payments after the filing, they have no defense against a foreclosure.

Completing a foreclosure gives the bank the most "clear title" they an get, depending on state allowances and is far better for the bank at this stage than a short sale.

I haven't tried buying a short sale property in these circumstances but I don't see why a bank would consider it based on what they have already been though with this property. How would it benefit the bank?

Post: You Don't Need To Be Good At Sales To Get Your First Deal

- Investor

- Zero Down Specialist

- Posts 1,807

- Votes 1,027

Quote from @Michael Carbonare:

𝐘𝐨𝐮 𝐃𝐨𝐧’𝐭 𝐍𝐞𝐞𝐝 𝐭𝐨 𝐁𝐞 ‘𝐆𝐨𝐨𝐝 𝐚𝐭 𝐒𝐚𝐥𝐞𝐬’ 𝐭𝐨 𝐆𝐞𝐭 𝐘𝐨𝐮𝐫 𝐅𝐢𝐫𝐬𝐭 𝐃𝐞𝐚𝐥

“I’m not a sales person.”

Neither are most of the investors closing creative deals right now.

The idea that you need to be slick, pushy, or persuasive to succeed in real estate?

Total myth.

What you really need is:

An offer that solves a problem. That problem is often unwanted or unmanageable debt.

A simple conversation that clarifies how your solution addresses that debt. For example, monthly income that covers their monthly expense.

The ability to listen more than you talk.

Sellers aren’t looking for a pitch. They’re looking for help.

Creative strategies are help when done right.

Most of the new investors I know with start off nervous, awkward, and uncertain. I certainly did.

A few weeks later, I was having confident, low-pressure conversations with sellers. You will too.

It’s not magic. It’s reps, feedback, and guidance.

You don’t need sales skills. You need people skills.

If you’ve been holding back because you’re “not good at sales,” DM me. I'll send you an audio file of my conversation with a homeowner who had a vacant $2.1M condo.

Well,

I disagree. ;-) Politely, but I disagree.

If you aren't making the phone calls and talking to people, you'll never get a deal. It's a lifestyle.

That's called sales where I come from.

Post: How to know if MTR market is saturated

- Investor

- Zero Down Specialist

- Posts 1,807

- Votes 1,027

Quote from @Sherry T.:

Thanks everyone for the generous advice and actionable steps I can take!

@Claudia Buchegger, I appreciate your insight into the traveling nurse markets. It’s interesting to know that FF is not reflective of true vacancy.

@Ken M. do you have a recommended method to look up this info? I quickly checked a big chain and it wasn’t very clear what the vacancy was.

@Nick Maugeri You’re right, the financials have to make sense. I think I can reasonably get $1000 more per month with MTR but would incur $400 more utility expense per month. I’m a long distance investor so I’d need to figure out the logistics as well as my current PM only manages LTR. I’d probably first try out self managing with a single unit when there is a natural turnover, as @Miguel Del Mazo suggested.

That info usually comes from the local hospitality group or local hotel trade association or local revenue board.

Post: Safe to Accept Gross Income of 2X the Rent for Tenant Applicants?

- Investor

- Zero Down Specialist

- Posts 1,807

- Votes 1,027

Quote from @Tricia O'Brien:

Hello BP Folks!

Has anyone accepted tenants for a SFH who have a gross income of only 2.2X the rent or 2.4X the rent, and did that work out well for you?

I hired a new property manager for my rental property in California (SFH, 3 bedrooms, 2 bathrooms, 2 car garage, fenced in yard), and told her my screening criteria were: Gross Income at least 3x the rent, credit score at least 600, good landlord references. Asking rent currently is: $2300/month. After 2 weeks, she presented me with an applicant with income 2.2X the rent and then a week later someone with income of 2.4X the rent. I declined them both. When I told the PM, "She makes 2.2X the rent," she said, "They're close to 3X the rent."

In looking at Zillow ads for another PM company, I noticed that this company is asking for a minimum gross income of 2.8X the rent.

Is this the new normal? What happened to the old standard of gross income of 3X the rent?

It feels too risky to me to take someone that you know from the beginning is going to be paying almost 50% of their gross income on rent and utilities, plus they might have credit card debt too.

I told the PM to lower the rent to $2200/month, and she said it's still going to be hard to find someone that makes $6600/month.

What to do? What are your minimum income requirements?

Thanks in advance for your input! :)

Look at your replacement costs. If you have to evict, what is your cost of finding a replacement tenant? Couple of months of missed payments, legal fees, cleaning cost, vacancy, etc. You want to make that as unlikely an event as you can get away with.

What is the policy with your property manager? Does your PM get money for placing tenants? Might there be a hidden agenda? Some property managers charge a month's rent to fill a vacancy. If they fill a vacancy with a poorly qualified candidate, they are likely to have to fill that vacancy again pretty soon, aren't they? (because you will be evicting the tenant)

Some property managers use that technique to enhance their bottom line. Obviously I don't know on this PM, but you should figure out if that is a driver in their decision making.

Post: Any short sale experts - breach of contract advice?

- Investor

- Zero Down Specialist

- Posts 1,807

- Votes 1,027

Quote from @Brian Stike:

First,

YES - I plan to reach out today to a real estate attorney.

Looking for advice and if anyone has encountered this before just to get some preliminary data before making phone calls to lawyers.

I have, under contract, a single family home that is a short sale. The sale contract was fully signed and my agent was informed that the primary lender accepted the offer. The offer more than covers the outstanding 1st lien, based upon what I've seen in the county mortgage records online.

Closing day came and went - and then suddenly a day or two after the closing date was to occur I receive notice that the seller "needs to send a cancellation notice, as there is suddenly a 2nd lien who won't agree to the sale."

Rumor is that the 2nd lien is a general contractor, but I find zero record of this in the county websites.

I've already paid for liability and flood insurance (had to be paid before close, I paid it 24 hours before the closing date) and now I'm being asked to sign a document basically mutually agreeing to cancel the sale. I'll now need to fight to get the insurance cancelled and refunded, and something just seems very fishy about this whole situation.

I do not understand the following:

- How can there suddenly be a 2nd lien, with no evidence of such on the county websites, and how could the seller have agreed to the sale and executed the sale contract fully to begin with, stating that the short sale was accepted a month ago if he had evidence of this second lien?

- Doesn't the execution of the sale contract bind the seller to sell me this property? Once he signed and accepted this offer - he can't suddenly decide that he needs more money to close out a 2nd lien. If that were the case - he should have never accepted the offer to begin with, correct? In FL law, there are only certain reasons why a seller can cancel a contract (buyer can't get financing, force majeure, mutual agreement of both parties, title issues, etc)

- Can this 2nd position lien holder prevent the sale of the property, even though the sale was allegedly agreed upon by the primary lien holder? Again - I see no evidence of a 2nd lien in the county websites, but apparently its a G.C. who did work on the home.

- Can I still force this sale or somehow recover damages from this seller? I'm certain I won't get every penny of my insurance payment back (had to pay 6 months in advance), I've had GCs and builders out to the space to give quotes, I did a sewer line camera inspection, etc.

I know some of this is the cost of doing business as a real estate investor (sewer main inspection, for instance) - so I'm not concerned about that. I' m more concerned with the $2400 in insurance costs, the seemingly fishy way this is all going down, and the lack of transparency around this sudden "2nd lien".

I also plan to call the title company this am and see what info they have.

Does anyone have any suggestions, information, tips, etc?

Thanks!!

Only then will you know your next step.

Do that before you blow a gasket. You are paying your agent to take care of these burps. If they can't manage it, have a three way discussion with your agent, their broker and you.

By the way, to spend thousands and thousands ($10,000 to $25,000) of dollars to try to enforce a contract and the distraction it creates, rarely gives the outcome you think you deserve, The court will most likely side with the home owner, might award you monetary damages for money spent (not including legal fees) but is highly unlikely to force the sale.

Then you have to collect. Good luck with that.

My number one rule when someone backs out of a contract, let them go. You never really had a "meeting of the minds". A legal requirement for selling a property.

Oh, and defending your contracts, One such person outright lied in court. I caught the judge between sessions, mentioned that to him, and his response was "everybody lies in court".