All Forum Posts by: Ken M.

Ken M. has started 155 posts and replied 1793 times.

Post: Am I wasting my time investing in the Twin Cities?

Post: Am I wasting my time investing in the Twin Cities?

- Investor

- Zero Down Specialist

- Posts 1,844

- Votes 1,041

Quote from @Stephanie Deppe:

@Jeff Rogers super interesting! I’m starting to get it. One needs to build a network to get the deals. Real estate is a slow burn. It seems that there is so much misinformation out there about how “easy and passive” it is to get going. Good tip re getting to know your neighbors!

You can start by using sources off of this list

https://www.biggerpockets.com/forums/311/topics/1265103-ways...

Post: Is There A Solution To Housing Unaffordability?

- Investor

- Zero Down Specialist

- Posts 1,844

- Votes 1,041

Quote from @Marcus Auerbach:

Quote from @Ken M.:

Quote from @Marcus Auerbach:

In May of 1960 you could have bought a new construction home in Milwaukee for $13,999! That even included AIR CONDITIONING - modern technology!

It took the buyer 30 years to pay off that mortgage. I have the original newspaper ad and found the address; it's worth about $360k today. Let that sink in.

Typical Midwest ranch home: about 1,400 sqft. I am sure the finishes were top of the line, probably avocado green bathroom and orange carpet lol

From AI and for context: The median home price in America in 1960 was$11,900. When adjusted for inflation to 2020 dollars, this price is roughly $104,619.

Prices have gone up so much, and since lending (mortgage repayment) is computed as a percent of monthly earnings, and lenders typically lend 33% to 35% on the "front end" to cover the mortgage payment and taxes, and then maybe 50% to 55% on on the back end to cover all long term debt, thein is the problem.

Either lenders need to increase what they will lend ala 2008, at a much, much lower interest rate, (which long term doesn't work, because borrowers typically carry too much debt anyway)

or house prices have to come down.

People spend what they have. If it isn't house payments, it's toys like boats, bikes and beaches.

It's just a matter of time before it all "corrects" again. You can push a boulder uphill only so far, before you get tired and walkway from the burden (2008) as a culture. All things old become new again.

Post: Buy Houses For Pennies On The Dollar - Fix & Flip, BRRRR, Rental, STR - Learn How

- Investor

- Zero Down Specialist

- Posts 1,844

- Votes 1,041

The shortest, most profitable creative financing deal I've done in a while, is "As long as it took to get a Title Report", using "Subject To". (I simply "took over" his loan). I then sold the property and I had a $20,000 option fee cash and first and last of $1,500 at closing.

So, I made $23,000 in a few days on a property I spent $100 on. (that $100 was to prove it was a bonified transaction).

Then, I had a monthly cash flow of $973. That's Per Month!! (After paying the mortgage, taxes and expenses) (past results do not guarantee future expectations) Yes, I do teach how to do this.

It went so fast, I wasn't sure I had the right buyer. ;-) Strange, eh?

I usually take time to research the buyer, but he had the money and I have tightly written contracts, so it worked. He paid on time for a couple of years, so it cash flowed. Then he cashed me out. From the "cash out", I got another $25,000.

The value of the property had gone up. so he had a great deal and I had a great deal. I wasn't greedy, we both stuck to the agreements and it went well. I was prepared to make the underlying payments if necessary, but he always paid on time, and I stayed in touch with the person I bought the property from, just in case something arose regarding the transaction. Nothing unusual happened and everybody was taken care of and very happy. Yep, you can do this, too.

It's important to know your numbers, but you must have have good sources and know a few tricks as well.

Creative Financing can work well if you follow the rules and know what you are doing.

Here's one creative finance deal I have done and the very positive results. This particular property was in AZ but CA, ID, GA, and TX are good markets too.

Don't confuse buying in good markets with limiting yourself to being from those markets. You can buy in those markets and be from there or in addition, be from places like WA, OR, OK and so on. You just need a little guidance.

https://housecashaz-qloag.wpcomstaging.com/2024/01/04/dm03-learn-10-low-cost-ways-to-buy-a-house/

Yes, I provide the receipts to show this works. If you want a copy just email me, [email protected] and I'll send you "How I did It", "Start to finish". it might help you find similar deals.

Post: Buying Foreclosures Below Market-How The Numbers Work - New? Use Creative Financing

- Investor

- Zero Down Specialist

- Posts 1,844

- Votes 1,041

Quote from @Ken M.:

Buying an "Off Market" property with "Subject To" and "Wraps" & Selling "Lease / Option"

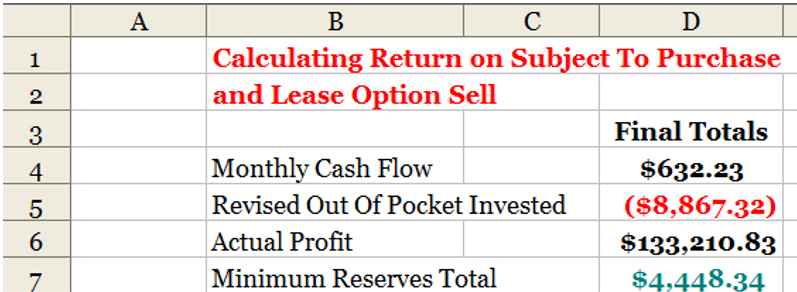

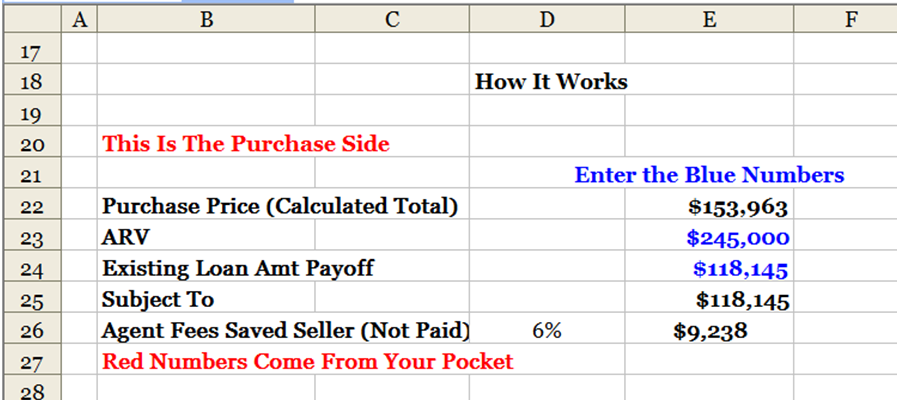

When buying a property to cash flow, you need to know what your expenses are. The following is one I actually purchased in Phoenix that was a pre-foreclosure. The seller and I negotiated the terms. I did not offer a number to him, he told me what he needed. This first portion is the end result. The following portions are how we got there. Click on images to enlarge.

The house was not suitable for the MLS. The seller had waited too long to fix the problem and just wanted out. He said he needed $10,000 so he could move back to his home state. So, this is how we put the deal together.

First, you determine ARV (After Repair Value) so you can see if this one is actually worth buying. In this case it’s worth $245,00 fixed up.,(ARV).

You enter the Blue Numbers only, the rest are calculated. Enter the ARV (it's MLS value after it's all fixed up) on line 23, you get that number from looking at "comps". On line 24 you enter the payoff amount. We’ll take care of the arrears in a minute.

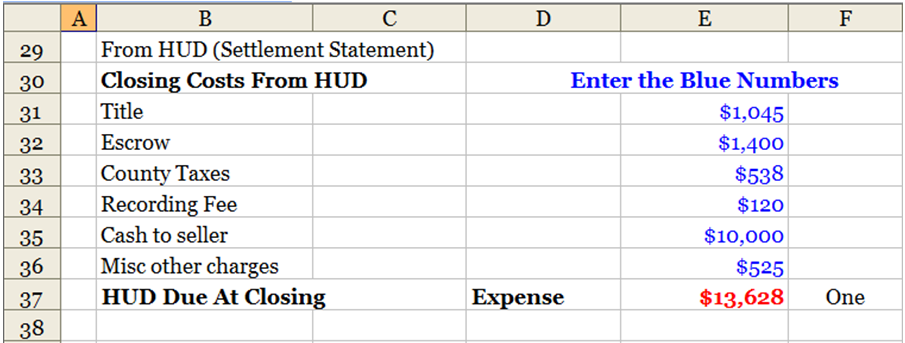

We always go through Escrow and Record, so we need to account for those costs. We Record because it’s the right thing to do and we want to know about any actions that come up against the property. Some people say don’t Record because of the Due On Sale clause, or to use a Land Trust to defeat the DOS which is bad information. If a lender wants to enforce a Due On Sale, a Land Trust violates the DOS anyway so it is ineffective in stopping the Due On Sale call.

Line 35 is always negotiable, but the seller needs enough to rent an apartment and move their belongs or they will become squatters which causes serious problems. There will be closing costs.

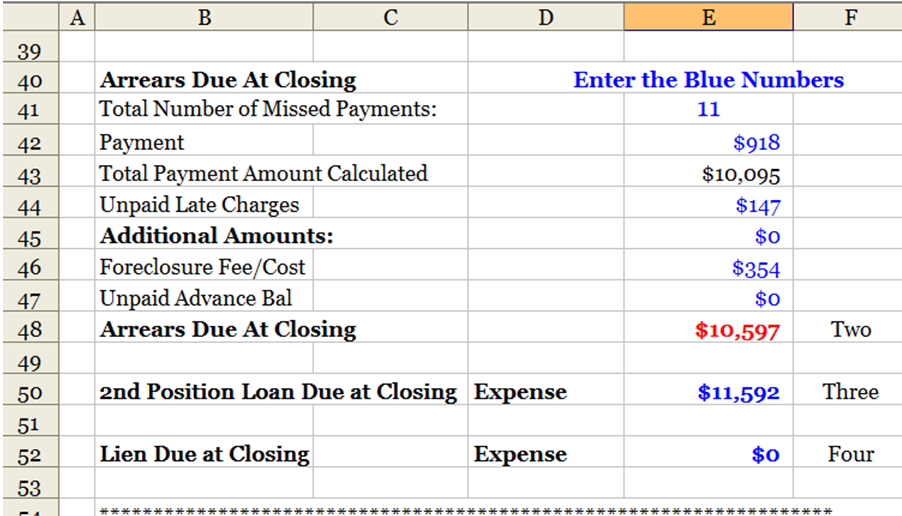

And of course, since this is a pre-foreclosure, the arrears have to be brought current.

Sometimes, a property will have a second loan or lien. Usually those can stay in place, but sometimes you have to pay those to buy the property. You can get the payoff amount from the lender. There is a specific process for doing that properly. If you are new, I would have someone help you with the process.

So, on this property, I paid line 37 $13,628 (which included $10,000 to the seller & closing costs $3,628), brought the loan current $10,597 line 48, took over the 2nd loan of $11,592 and took over the main mortgage of $118,145. I paid $153,862 and got a $245,000 property. But, I didn't need all $153,862, I only needed $24,225 to do so.

When you are new, looking for lenders & considering Fix & Flip, BRRRR, or rental, as a buyer, learn to ask the owner/seller to be one of your private lenders with creative financing. This works in Southern California (CA), AZ, WA, and GA & TX. Slight variations work elsewhere.

Post: flyer time, 1500 door hangers

- Investor

- Zero Down Specialist

- Posts 1,844

- Votes 1,041

Quote from @Daniel Bullock:

@Tony Bacon curious how the door hanger approach has worked so far? Have you found it effective?

The best way to do door knocking, yes, it does work, is to knock, have a conversation, leave a hanger if no one answers.

Post: Is it Ever Worth it to Sell at a Loss?

- Investor

- Zero Down Specialist

- Posts 1,844

- Votes 1,041

Quote from @Brendan Wages:

Good morning,

I'm 24, active-duty military, currently own 2 condos-1 long distance rental with tenants, the other primary residence w/ a roommate tenant, in San Diego. I recently discovered that I absolutely abhor roommate living and started to entertain the idea of selling my current primary residence (2/2) and downsize to a 1/1 so I can comfortably afford a mortgage without the need for tenant rental income to offset cost of ownership.

With that said, I bought my current residence, the 2/2, in March 2025 and will have to sell at a loss. It looks like, according to my realtor, I would need $30k-40k in order to completely payoff current loan (after selling), cover down on closing costs, fees (realtor's quote 1%), deposit or downpayment on a new property. I would love hear hear some opinions on this. Is it worth it for my peace of mind? I am truly going crazy with a roommate... I know for $10k, I'd cut my losses and do it without a second thought. But $30k-40k is a lot... or is not, in the grand scheme of peace of mind and long term appreciation of a 1/1 condo in San Diego?

Additionally, I know I have the option of renting the unit out entirely and then renting a studio for my residence which would put me in a similar position financially as my current situation w/ the roommate. Open to any and all thoughts, suggestions. Thank you!

-Brendan

"active-duty military" and "I am truly going crazy with a roommate."

Now, how does THAT work? Are you an army of one?

Post: Need advice - Soon to be realtor and investor

- Investor

- Zero Down Specialist

- Posts 1,844

- Votes 1,041

Quote from @Ethan Ung:

Completely get that Ken M.

It's just that I was identifying my no expenses as a financially superior way to get ahead of the curve, as well as being able to take care of my parents by physical proximity. I live in a traditional Chinese household and it is common for their kids to stay with them for the rest of their lives, especially when my father is getting old and he's incredibly sick. I can't afford to move out for the sake of moving out and being a "grownup."

I totally understand. Taking care of family is far more important than material gain, in my opinion.

However, investing is material gain. Lenders are material people. They expect certain behaviors and won't lend otherwise. If you come to the point where you need extra financing, perhaps borrowing from a rich uncle is your solution or maybe creative finance. Just don't expect typical investors and lenders to be sympathetic to your life choices. Work around them and carry on.

Post: Buying Foreclosures Below Market-How The Numbers Work - New? Use Creative Financing

- Investor

- Zero Down Specialist

- Posts 1,844

- Votes 1,041

Buying an "Off Market" property with "Subject To" and "Wraps" & Selling "Lease / Option"

When buying a property to cash flow, you need to know what your expenses are. The following is one I actually purchased in Phoenix that was a pre-foreclosure. The seller and I negotiated the terms. I did not offer a number to him, he told me what he needed. This first portion is the end result. The following portions are how we got there. Click on images to enlarge.

The house was not suitable for the MLS. The seller had waited too long to fix the problem and just wanted out. He said he needed $10,000 so he could move back to his home state. So, this is how we put the deal together.

First, you determine ARV (After Repair Value) so you can see if this one is actually worth buying. In this case it’s worth $245,00 fixed up.,(ARV).

You enter the Blue Numbers only, the rest are calculated. Enter the ARV (it's MLS value after it's all fixed up) on line 23, you get that number from looking at "comps". On line 24 you enter the payoff amount. We’ll take care of the arrears in a minute.

We always go through Escrow and Record, so we need to account for those costs. We Record because it’s the right thing to do and we want to know about any actions that come up against the property. Some people say don’t Record because of the Due On Sale clause, or to use a Land Trust to defeat the DOS which is bad information. If a lender wants to enforce a Due On Sale, a Land Trust violates the DOS anyway so it is ineffective in stopping the Due On Sale call.

Line 35 is always negotiable, but the seller needs enough to rent an apartment and move their belongs or they will become squatters which causes serious problems. There will be closing costs.

And of course, since this is a pre-foreclosure, the arrears have to be brought current.

Sometimes, a property will have a second loan or lien. Usually those can stay in place, but sometimes you have to pay those to buy the property. You can get the payoff amount from the lender. There is a specific process for doing that properly. If you are new, I would have someone help you with the process.

So, on this property, I paid line 37 $13,628 (which included $10,000 to the seller & closing costs $3,628), brought the loan current $10,597 line 48, took over the 2nd loan of $11,592 and took over the main mortgage of $118,145. I paid $153,862 and got a $245,000 property. But, I didn't need all $153,862, I only needed $24,225 to do so.

When you are new, looking for lenders & considering Fix & Flip, BRRRR, or rental, as a buyer, learn to ask the owner/seller to be one of your private lenders with creative financing. This works in Southern California (CA), AZ, WA, and GA & TX. Slight variations work elsewhere.

Post: Is There A Solution To Housing Unaffordability?

- Investor

- Zero Down Specialist

- Posts 1,844

- Votes 1,041

Quote from @Marcus Auerbach:

In May of 1960 you could have bought a new construction home in Milwaukee for $13,999! That even included AIR CONDITIONING - modern technology!

It took the buyer 30 years to pay off that mortgage. I have the original newspaper ad and found the address; it's worth about $360k today. Let that sink in.

Post: Is There A Solution To Housing Unaffordability?

- Investor

- Zero Down Specialist

- Posts 1,844

- Votes 1,041

Quote from @Henry Lazerow:

It cost a lot to build in USA. I do not see that changing. Even if rates fall, it will still be very hard for many working class Americans to afford homes. 70 years ago there was less permitting required, less litigation risk/builder insurance required and way less labor regulations resulting in cheaper builds.

Things have changed. Expectations have changed. Not always for the better. :-)