All Forum Posts by: Chris Seveney

Chris Seveney has started 371 posts and replied 18840 times.

Post: Did Brandon Turner really lose $14M of investor money while pocketing $4.4M???

Post: Did Brandon Turner really lose $14M of investor money while pocketing $4.4M???

- Investor

- Virginia

- Posts 19,701

- Votes 17,314

Quote from @Brian Burke:

Quote from @James Wise:

Quote from @Mike Williams:

We’re aware of the chatter circulating in online forums, as our investors often bring it to our attention. Recently, some misinformation has been shared regarding our investment in Heights on Katy Apartments in Houston.

We typically don’t get involved in forum discussions since they’re meant to be spaces for investors to speak freely, share opinions, and sometimes even vent. A little banter or criticism comes with the territory, and that’s fine. But in this case, speculation has crossed the line into misinformation.

To be clear: the claim that Open Door Capital or its principals “pocketed” $4.4 million from the Heights on Katy investment is false. No such distribution ever occurred. The property was purchased for $70.4 million, and any fees associated with the acquisition were standard and fully disclosed in the offering materials.

Real estate markets over the past two years have been challenging, especially multifamily in Sunbelt regions, and Heights on Katy has not been immune. We’ve worked closely with our partners and investors to navigate those headwinds responsibly, to try and protect investor capital, and to communicate openly throughout the process.

We can’t monitor every forum thread out there, but if you’re an investor (or even a prospective investor) and have questions, just call us directly. Our team is always available to discuss and provide any supplemental information or property specifics with investors.

-Mike Williams

Open Door Capital | odcfund.com/disclosures

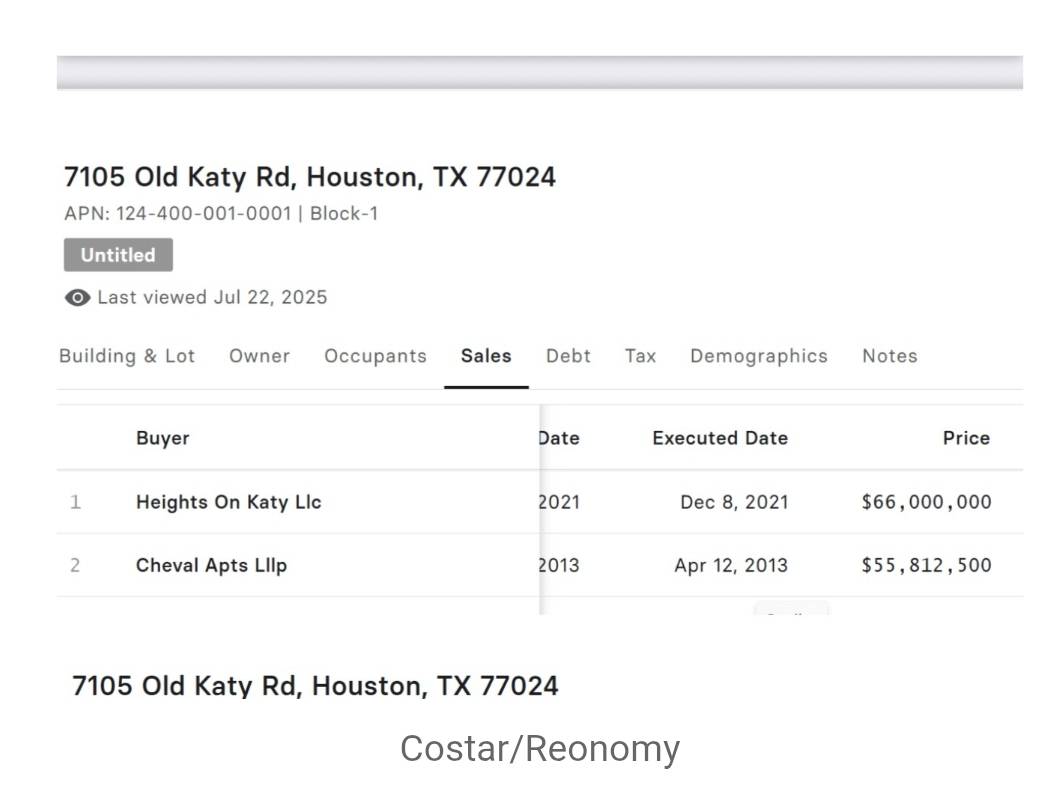

So to clarify Mike. You're saying the purchase price was $70.4 Million, not the $66 Million as shown in what appears to be a screenshot from Costar?

Are you saying this screenshot that's been published online is fake and or doctored?

I don’t know about this deal and I’m interested in Mike’s answer, but Texas is a non-disclosure state. That means that purchase prices aren’t publicly disclosed and CoStar and other data providers are forced to use other means to arrive at an estimate of purchase price. These methods include reverse engineering the loan amount (like that is even remotely reliable?!). Sometimes they do contact the buyer, seller, and broker and ask to confirm the price, and sometimes they will share the actual price. And often times they don’t—it compromises their argument for tax protests.

I’ve owned a lot of apartments in Texas (don’t anymore) and I subscribe to CoStar. I’ve looked up my own properties over the years, and once in a while CoStar was right, and often they weren’t.

if the basis for the allegations lodged against ODC in this thread are based only on a CoStar reported purchase price, there is very likely much ado about nothing here. Not to minimize the claim that investors lost money—I wouldn’t know. But the only way to know the price, fees, and what the sponsor pocketed is to hear it from the sponsor or their investors. Costar isn’t much help here—especially in Texas.

I went back read the linkedin post and thought the same thing, how did they get the purchase price? he notes "Until I got the actual recorded purchase price?" What does that mean? He would have had to get the CD, which I doubt he got, if he had it why not post that as your backup in the article? As mentioned if co-star - how accurate? Datatree shows the $70M number.

Some other things in the Chatgpt written article note about the unit offering price is arbitrary - that is VERY common as if you do not have a third party valuation done then you basically have to put this.

There are some valid questions like where did they burn through the money etc. and this may not be a great investment in hindsight. So questions should be asked, but there is not enough evidence that I can find to say they walked away with $4M.

Here is link : https://www.linkedin.com/pulse/when-sec-looks-ways-do-cases-...

Post: Let’s talk about note exit strategies.

- Investor

- Virginia

- Posts 19,701

- Votes 17,314

Quote from @Barbara Johannsen:

What’s your preferred move — hold, flip, or restructure? I’d love to compare approaches with others in the note investing space.

recommend you actually post these in the group specifically for note investors....

Post: The Downfall of BiggerPockets Forums?

- Investor

- Virginia

- Posts 19,701

- Votes 17,314

Quote from @Joel Owens:

I think forums are almost dead these days. Most of the people contacting me now are seeing me on dozens of podcasts or asking chat GPT or similar about NNN and I pop up. Life is so fast for high income earners they want answers in seconds or minutes to find someone to do business with. They don't want to search for days or weeks.

I am talking people making millions of dollars a year of income or higher.

I haven't gotten a direct lead off this site worth anything in years. Most of it is spam or junk.

Part of the issue is people put a question in chatgpt to get an answer and they think its the correct answer. Real estate is not like a math problem where 2+2 is four. Real estate is mostly gray and taking advice from AI that reminds me like a guru, will give you high level answer but then when it dives deep it is a lot of mistakes. Reality is your best advice is going to come from a human who has been doing it and can discus the situation, but if you think a computer program is going to give you better information today, I am sorry but you are wrong.

Post: How useful can a 100% financing option be for you?

- Investor

- Virginia

- Posts 19,701

- Votes 17,314

Quote from @Steve Dorian:

If indeed you have the option of taking a 100% financing for your residential and commercial deals, would you consider it useful?

it depends. What is the interest rate the lender is charging for the money. IF it is cheaper than my cost of capital then yes, if it is more than no. When we take financing, we are strategic about it, we do not "need it" but could use it to enhance the outcome without imposing significant risk. I know people who do not need the money but want ease of capital and giving them 100% can work, then you have people with zero cash or reservecs and giving them 100% will end in disaster. So it depends.

Post: Selling Performing Notes to Fund Your Next Real Estate Project — Experiences?

- Investor

- Virginia

- Posts 19,701

- Votes 17,314

Quote from @Victoria OHare:

Hi BP Community,

I’m curious how other investors are navigating performing residential mortgage notes. Some investors sell notes they hold to unlock liquidity for new flips or investments, while others prefer to hold them for ongoing cash flow.

A few discussion questions:

- Have you sold performing notes before? What influenced your decision?

- How do you handle due diligence on smaller notes versus larger pools?

- What lessons have you learned in pricing or timing the sale of notes?

Thank you!

We sell performing loans, we typically sell when we have other opportunities and look to recycle cash. Due diligence on a note is the same whether its on 20 in a pool or one loan. We do it all in-house. Regarding lessons learned, I have about 300 podcast episodes of lessons learned in note investing.

Post: Does a QUIET TITLE action WIPE an older mortgage ?

- Investor

- Virginia

- Posts 19,701

- Votes 17,314

Quote from @Michael Morrongiello:

Technically the 2nd lien slid into FIRST Lien position when the superior 1st lien got paid off and released. However I agree with the Motion for summary judgment surrounding the QUIET TITLE action affirmed its likely NOT a collectable debt and YES we are getting a more firm legal opinion on that...

Appreciate the insights....and caution

what did an attorney say?

Post: What Strategies Do You Use to Value & Sell Performing Notes?

- Investor

- Virginia

- Posts 19,701

- Votes 17,314

Quote from @Victoria OHare:

Hi BP Community,

I’ve been focusing lately on buying and selling residential mortgage notes, particularly first-position, performing notes. I'm curious to hear how others in this space are valuing and exiting notes.

A few discussion questions:

-

What metrics do you weigh most heavily (LTV, payment history, discount rate, etc.)?

-

When do you decide to hold a note vs sell it?

-

For those who sell, how do you find buyers and structure closing?

Happy to share what I look for as a note buyer too, if that’s helpful for others.

LTV is critical in performing notes. When I see people buying newly originated paper at 90% LTV or greater for a 10-12% return I shake my head. Way too much risk for that type of return.

Regarding structuring closing, we use third party custodian for collateral so we execute LSA and then send all collateral to the end buyer. Typically we do this with scanned versions and not send the original unless its an institutional client that also ahs a custodian and get bailee letter.

Post: 📈 U.S. News Highlights Surge in Mortgage Note Investing — What’s Your Take?

- Investor

- Virginia

- Posts 19,701

- Votes 17,314

Quote from @Don Konipol:

Quote from @Victoria OHare:

Hey BP community,

I recently came across an article on U.S. News discussing the growing interest in mortgage note investing, especially in today's market. The piece highlighted how investors are turning to performing notes as a stable alternative to traditional real estate investments.

As someone actively involved in this space, I wanted to open up a discussion:

-

Have you considered investing in mortgage notes?

-

What are your experiences with performing vs. non-performing notes?

-

Any tips for those looking to get started in this niche?

Looking forward to hearing your thoughts and experiences!

yep. many of them are also pay to play where those mentioned in the articles will sponsor "pay" a fee for the article.

Post: : Scaling Through Private Lending — What’s Working for You?

- Investor

- Virginia

- Posts 19,701

- Votes 17,314

Quote from @Michael Santeusanio:

Private funding has become a big part of how investors scale their portfolios.

If you’ve raised or used private money, what tips would you give to someone just starting out?

Whatever you think it will cost or how long it will take. Triple it...

We have raised $50M+ over the past 3 years but it is a grind. Also I would argue you cannot do it alone (and manage the fund), you need someone who can raise money on your team.

Post: Good CRM Program Recomendation

- Investor

- Virginia

- Posts 19,701

- Votes 17,314

Quote from @Stephen De Vita:

Hello,

I am on the look for a CRM. I was wondering anyone has any experience with them. How much are you spending for them?

Stephen

we use gohighlevel. But there are many and all pretty much do the same thing. Its like picking a car, they all get you to point b from point a but have a few different bells and whistles.