All Forum Posts by: Nate Herndon

Nate Herndon has started 1 posts and replied 231 times.

Post: Has anyone had an out of state BRRRR actually work in the last 2 years?

Post: Has anyone had an out of state BRRRR actually work in the last 2 years?

- Lender

- Springfield, MO

- Posts 240

- Votes 178

Quote from @Nicholas L.:

Here's one we are refinancing currently for an Oklahoma City BRRRR investor. They purchased using a program that finances 100% of your purchase/rehab on paper, and takes a 15% deposit as cash-collateral that they hold until you refinance.

• $60k purchase

• $35k rehab

• $95k total rehab loan payoff

• 15% deposit = $14,250 "down payment"

• $126k ARV

(confirmed via refinance appraisal, borrower expected this to be higher)

• 80% rate/term refinance ($100,800 loan) @ 6.75% [700-719 FICO]

• Applied $4k of deposit to payoff for an updated payoff amount of $91k

• Cover closing costs with 80% r/t refi + $2k back to borrower at closing (still considered a r/t refi if under $2k) + remaining $10,250 deposit reimbursed after payoff = $12,250 total back to borrower

• $4k of his deposit + closing costs for rehab loan = his "cash" in the deal

• $1,250 market rents

• Total PITI = $765.62

• DSCR = 1.6327

Post: LLooking for lending partner in New London, CT

- Lender

- Springfield, MO

- Posts 240

- Votes 178

@Robert Lindsley give me a call or shoot me an email - happy to take a look at this one with you. I've got a few deals from 5 units to 48 units in process for clients.

Post: DSCR loan lenders/ AirDNA rental income - Baltimore

- Lender

- Springfield, MO

- Posts 240

- Votes 178

Quote from @Ioulian Stoitchkov:

Hi all,

I am looking for DSCR lenders that operate in the Baltimore market. Preferably, those lenders accept rental income from AirDNA as the property I'm looking to refi is on the higher price range.

Thank you!

Please see below for some recent limitations I am seeing on Baltimore properties with a top DSCR program I like to use for my clients:

• Appraisal must be ordered with approved AMC

• No appraisal transfers allowed in Baltimore

• 5% LTV/LTC haircut

• Must be fee simple

• No appraisal transfers

This is not the case across all DSCR programs right now, but these sorts of requirements are pretty common for the Baltimore area at the moment. The biggest impact to investors right now is the pullback on LTV/LTC with a 5% haircut - but I have also seen some programs abandon Baltimore completely.

As for your specific scenario, a property would need to be furnished and listed for rent on a 3rd-party website as a short-term rental in order to use AirDNA market rents (of which 80% would be useable).

If the AirDNA rents were $50k per year, you would get credit for $40k per year in underwriting.

Post: Has anyone had an out of state BRRRR actually work in the last 2 years?

- Lender

- Springfield, MO

- Posts 240

- Votes 178

@Travis Timmons I am certainly seeing plenty of experienced (and new) investor clients repeatedly pursue out-of-state BRRRRs in 2025. What are some of your "metrics for success"? I might be able to take a look at a couple of recent ones where we have financed the purchase-rehab and the refinance and offer up examples of what I'm seeing.

Post: I need a Michigan lender or broker

- Lender

- Springfield, MO

- Posts 240

- Votes 178

@Cameron Porter I would be more than happy to take a look at some deal scenarios with you. I like to send same-day prequal letters - no reason anyone should ever be waiting on that to make an offer.

Post: Finding the best interest rate

- Lender

- Springfield, MO

- Posts 240

- Votes 178

Quote from @Noah Wright:

Quote from @Eric Rosiello:

Quote from @Noah Wright:

Quote from @Eric Rosiello:

I am interested in refinancing a property.

In the past, I’ve gone through the exercise of researching online and/or calling lenders in my area to find the best loan product.

Lenders’ competitiveness changes all the time so it’s worthwhile to go through the exercise every time (as opposed to just going with who had the best rate last time).

I am wondering if there’s anyone out there who is doing this as service ? Hopefully this person would do a better job than I do and would also save me the time of going through the exercise each time I am considering a refi or new purchase.

Thanks!

Eric

Hi Eric,

Absolutely, happy to help!

I'm an independent mortgage broker specializing in investment real estate, including 30-year rental mortgages and short-term construction mortgages.

I have access to a Terminal system that indexes hundreds of lenders based on dozens of qualification criteria. Extremely thorough and robust

@Eric Rosiello, you wouldn't necessarily need a hundred lenders to reference - the top 3-5 programs in the private lending space are always going to shine through. As a broker working only with investment property lending, I'm pairing my clients up with a few of the top programs repeatedly.

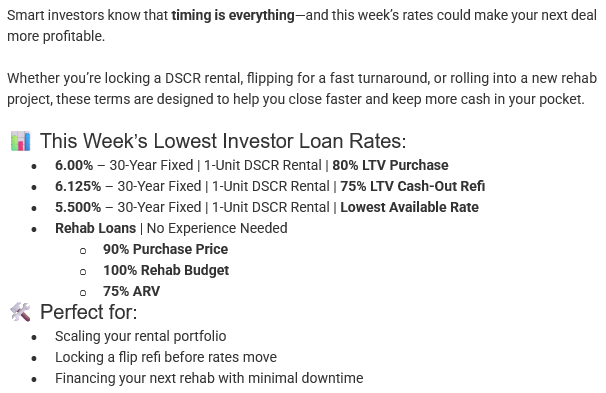

A good broker acts as that comparison tool for you since we have a finger on the pulse of those loan programs on a daily basis. Here's an example of the weekly refinance updates that we send to clients via email.

Post: Financing Question – 7-Unit (4-plex + 3-plex) in Baldwin City, KS

- Lender

- Springfield, MO

- Posts 240

- Votes 178

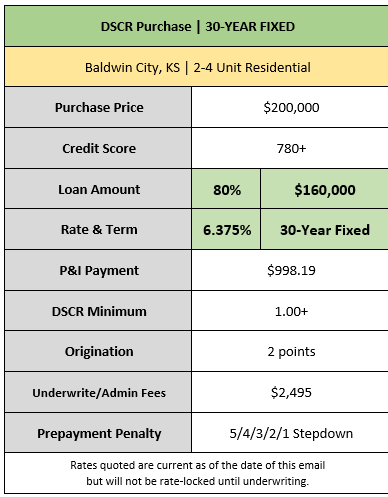

My recommendation would be a 30-year fixed DSCR on each property separately. This allows for more flexibility down the line should they choose to refinance or sell one property, but not do so with the other (vs. a blanket loan that ties the properties together and which may have a release premium).

Here's a quick example of what 2-4 unit residential loans would look like for buyers as long as the appraisals come back marked suburban (not rural - rural-marked appraisals will be capped at 65% LTV).

With Baker University nearby, I think there's a good chance these don't come back marked as rural even though the town is smaller. Any buyers should be eligible for the loans below, pending credit and asset verification.

Post: Very basic BRRRR question that I'm having trouble finding advice on

- Lender

- Springfield, MO

- Posts 240

- Votes 178

Quote from @Tim Schmitz:

I have a 4-plex that is mortgaged in my name, but right after getting the mortgage I quick-claimed the property into my company for better liability protection. So, seems like if I want to refi, I would need to move the property back into my name, since banks don't do mortgages for companies. This seems like a good way to have trouble with mortgage companies. Are most of y'all just keeping properties in your name when you want to do a BRRRR?

For my investor clients, we close DSCR loan refinances in their entity name 99% of the time. I can count one hand the number of deals I have refinanced in someone's personal name out of 580+ in the past 3 years. Those that do close in their personal name either don't have an LLC set up or are against utilizing one for some reason. Should not be a major hurdle for yourself.

Closing in the name of your entity also does the following:

• Prevents the mortgage from reporting as a tradeline on your personal credit

• Does not affect your personal Debt-to-Income ratio

• Maintains the liability protection that you enjoy currently

Feel free to shoot me an email to review how other investors I work with are going about the BRRRR method.

Post: Cash Out Refi Recommendations

- Lender

- Springfield, MO

- Posts 240

- Votes 178

@Jaron Walling yes indeed, $5k in financing costs - for a 65% LTV on the same scenario above, the fees would all be fixed but the rate would improve. There is an opportunity to lower the fees for a higher rate, but the ratio favors a lower rate right now. I'd only recommend building fees into the rate if cash was king - but if that were also the case, we'd probably be talking about a 75-80% LTV cash-out for you vs. 65% LTV.

• 65% LTV rate/term refi = 6.25% (loan amount <$100k is +0.25%)

• 65% LTV cash-out refi = 6.375% (loan amount <$100k is +0.375%)

Post: Cash Out Refi Recommendations

- Lender

- Springfield, MO

- Posts 240

- Votes 178

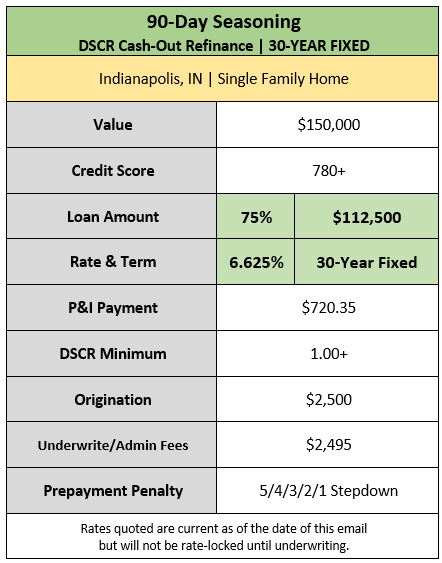

@Steele Kruzel everyone who has posted above has covered good ground for you on ways they could help with your conventional refi. Though the fees on DSCR are higher, that's what I opted for recently on a purchase deal of my own when compared to conventional.

The 7.125% conventional rate (at 75% LTV) vs. a 6.50% DSCR rate (at 80% LTV) was good math on my short-term rental. Here's what the refi could look like on a 90-day seasoning program that Indianapolis investors are using.