All Forum Posts by: Eric Fernwood

Eric Fernwood has started 64 posts and replied 793 times.

Post: AI-bubble? What will happen to real estate when it bursts?

Post: AI-bubble? What will happen to real estate when it bursts?

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

The impact largely depends on the tenant segment that occupies your properties. If your tenants work in AI-related roles, you could see some effect on occupancy. For tenants in other fields, the impact is likely minimal (at least for the near future).

What we are seeing, however, is a broader shift. As AI replaces certain software development and rule-based, routine desk jobs, the greater risk may come from ripple effects across related industries rather than from AI companies themselves.

We have not experienced significant impact on our client’s properties. For example, during the 2008 financial crisis, our clients saw no decrease in rent and no vacancies. By contrast, properties targeting low-wage tenants were hit hard, with many multifamily abandoned and eventually foreclosed. That’s why it’s essential to understand the demographic your property attracts, the right tenants make all the difference.

Post: When Is It Actually a Good Time to Sell Real Estate?

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Joseph Snyder,

Thanks for the kind words.

“How do you usually calculate if rents…”

We compare the rent growth rate vs the inflation rate over a given period. We calculate the Compound Annual Growth Rate (CAGR = (Ending Median Rent / Beginning Median Rent) ^ (1/years) - 1) between 2015 and today, for properties that conform to our target property profile. On inflation, we usually use the inflation data from the Bureau of Labor Statistics.

Comparing the CAGR for rent and inflation is how we determine whether rents outpace inflation.

“Renovation enhancements…”

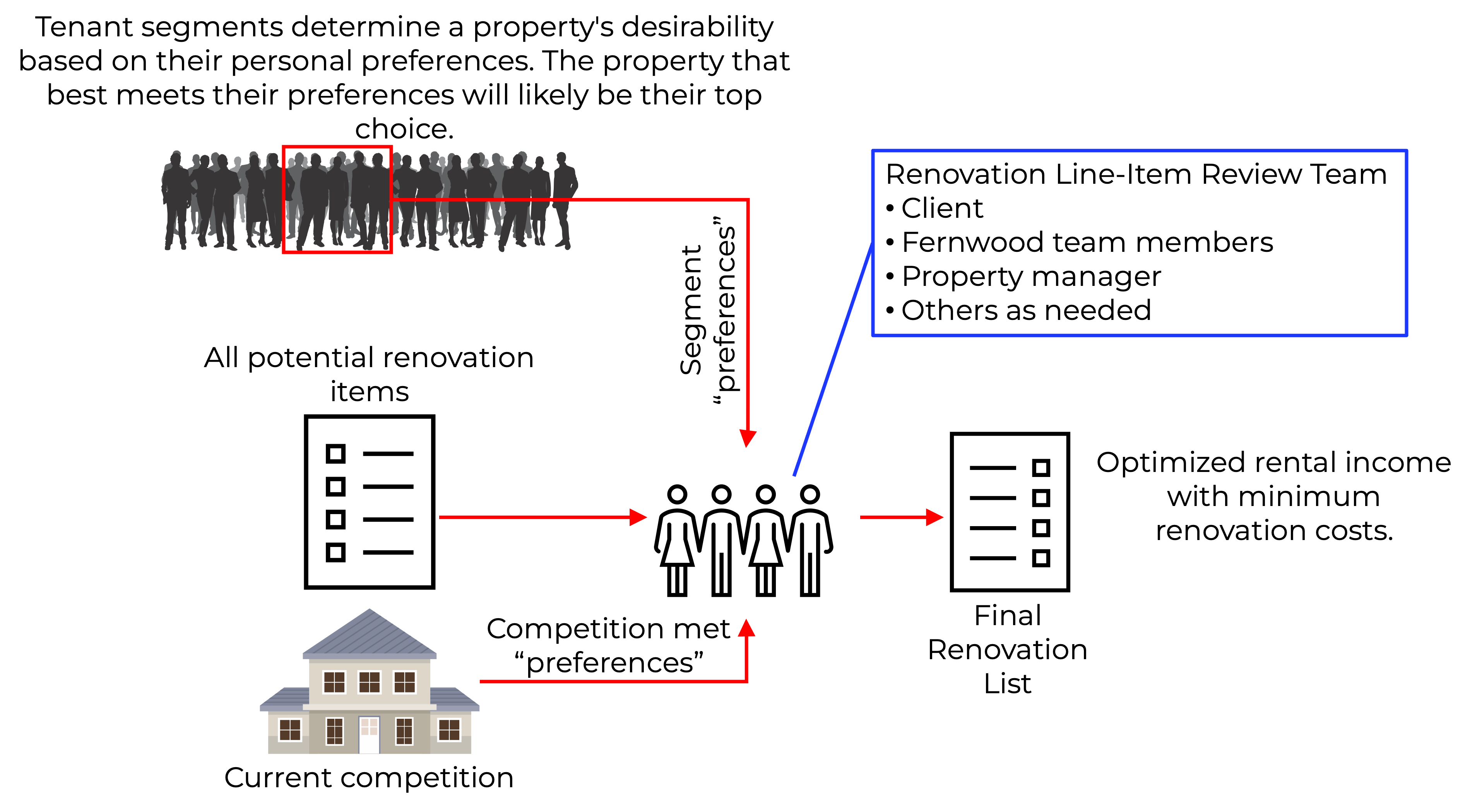

Determining what enhancements will significantly increase rent is more difficult than it seems. We do this in a two step process. First, we come up with a list of all renovation items that would make the house as attractive as possible to our target Tenant segment. We don't care about the cost at this point; we just want to get a consolidated list.

Next, we have a meeting with a team of people where we review each renovation line item and decide whether the ROI is sufficient. See the diagram below.

We start with a detailed list of potential renovations based on the preferences of our target tenant segment. Then we compare the property to competing available properties. Competition isn’t limited to the neighborhood—someone moving to Las Vegas for work may look on either side of town, so a comparable property could be across the city.

We also consider rent sensitivity. The more you spend on renovations, the higher the rent must be, which shrinks the pool of qualified tenants. Depending on market conditions, it can be smarter to limit upgrades to keep costs down and attract a broader tenant base.

As to using this on social media with a shoutout, please do. Thank you.

Joseph, if I wasn't clear or if you have other questions, please let me know.

Post: How Much Cash and Time Are Required to Invest with Us?

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

During new client meetings, the two questions I hear most frequently are, “How much will it cost?” and “How much of my time will be required?” These are important, fundamental questions any investor should consider. In this post, I will provide a detailed rundown on the cash and time required to acquire a good Las Vegas investment property with us.

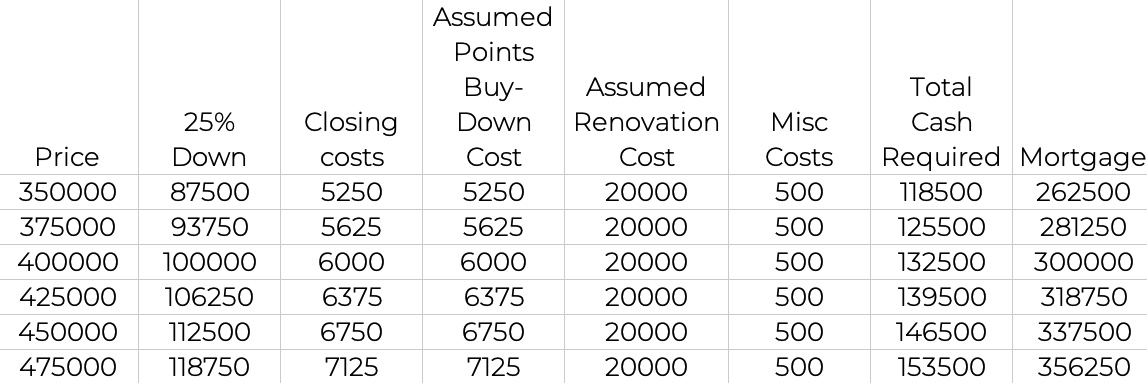

How Much Do You Need to Invest in a Good Las Vegas Investment PropertyMany people only consider the down payment when they’re estimating the cost. There are many additional costs, and below is a reasonable estimate of how much cash you will need to close and bring to (rental) market a $400,000 rental property. Note that some items are property-specific, for example, renovation cost.

- Purchase price: $400,000

- Down payment (25%): $100,000. I used 25% down because this is the most common amount our clients put down.

- Closing cost (financed, not a cash purchase): 1.5% x $400,000 = $6,000. This includes the cost of obtaining a loan, title and escrow fees, home inspection, etc.

- Typical interest rate buy-down cost: 1.5% x $400,000 = $6,000

- Typical renovation cost: $20,000

- Miscellaneous additional costs: $500

Total estimated cash required: $132,500 with a 25% down payment. This investment will also require a $300,000 mortgage. Below is a table showing how much cash and mortgage for different price points.

Notes:

- Property price: Obviously, higher-priced properties will cost more to acquire. However, the narrow property segment we target (to maximize chances of high performance) costs between $320,000 and $475,000 today.

- Our Fees: As outlined in our terms and conditions, we charge 2.5% of the gross sales price. What’s important to understand is that the seller, not you, almost always pays this fee. Out of 560+ properties, our clients have contributed to our fee only six to eight times or, about 1.4% of cases. If a seller refuses to pay our fees, we recommend finding another property.

- Renovation: I used $20,000 as an estimate, but actual costs depend on the property and market. We don’t use a standard upgrade list—just what’s needed to make the property competitive. We start with a full list of possible upgrades in the Property Report, then, during due diligence, narrow it down to only what’s needed to meet the rental goals.

- Buy Down Cost: I estimated the interest rate buy-down at 1.5% of the purchase price for simplicity, though the actual cost depends on your loan amount, down payment, and credit score, and is usually based on the loan amount, not the sales price. I used the sales price to be conservative. The buy-down lasts for the life of the loan, but I expect you’ll refinance to a lower rate if the interest rates drop significantly at some point.

- Down Payment: With the current high interest rates, you may need to put down more than 25% to have a neutral cash flow the first year. How much you need to actually put down depends on the cost to buy down the interest rate and the current interest rate at the time you buy. So there’s no simple answer. I just assumed 25% and 1.5% of the purchase price to buy down the interest rate.

- Miscellaneous Costs: I included a $500 buffer to cover unexpected minor expenses that may arise.

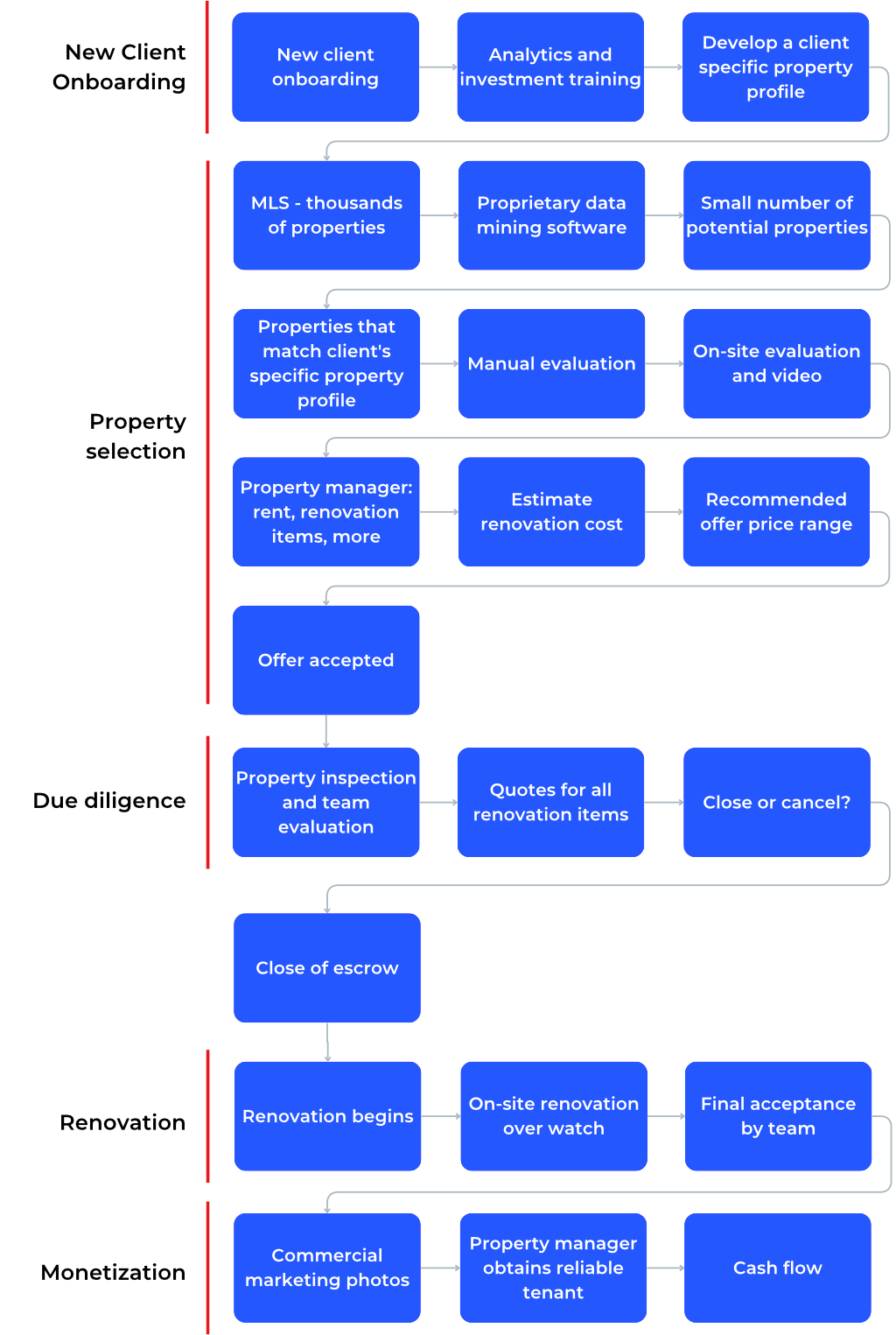

Due to our one-stop, done-for-you services, the typical amount of time that clients need to invest with us is very reasonable. I’ve asked multiple clients what the total amount of time is that they invested, including the first introductory call through getting their first rent check. The answers ranged between 8 and 12 hours total time. What does the amount of time include?

- Initial discovery call: 1 Hour. The purpose of this call is to understand your situation and goals and determine whether Las Vegas and our services are a good match for you. One-on-one with Eric Fernwood or Cleo Li.

- Processes and Fundamentals: 1 Hour. There are no secrets in real estate investing. In this session, we walk you through every step of our process. By the end, you’ll know exactly how we work and can decide if we’re the right fit for your goals. One-on-one with Eric Fernwood or Cleo Li.

- Review and Sign Terms and Conditions: 30 Minutes. Before we share property information, you’ll need to sign a buyer broker agreement. Because the standard agreement can be unclear, we add an addendum to spell out key points—like your right to cancel anytime by email or letter. If we’re not a good fit, you can walk away easily. Our terms and conditions cover several other important topics.

- Analytics and Portfolio Growth: 1 Hour. We show you how we analyze the property so that you understand the information we provide. Also, we explain how you can grow your portfolio with minimal incremental capital. One-on-one with Eric Fernwood or Cleo Li.

- Kickoff Call: in the kickoff call, you will meet with Cleo Li and the account manager. 1 Hour. The topics are typically about current market conditions and understanding your long-term goals so we can make informed property recommendations. One-on-one with Cleo Li and your assigned account manager.

- Property Report Review and Property Selection: Total: 30 minutes. On every property we evaluate that we believe matches your situation and goals, we create a detailed assessment. Initially, these could take a few minutes for you to read. Soon, you’ll be able to evaluate a property in about five minutes with the information we provide. On average, you will look at about six properties before we get one under contract.

- Review and eSign various documents: 30 minutes to an hour.

- Principal Forms of Ownership and Risk Reduction: Optional 1 hour meeting. In this meeting we will discuss what I have learned from sitting in on client attorney meetings. The goal is to be aware of the pros and cons of the various forms of ownership. Also, you will learn why we remove certain things from rental properties during renovation.

- Meet the Property Manager: 1 Hour. In this session, you’ll learn about being a landlord in Las Vegas, fees, tenant selection, maintenance, when rent is deposited, and more. This is a one-on-one meeting with the property manager.

- Final closing signing: 1 hour if financing, 15 – 30 minutes if cash.

The total time is about 7.5 to 9 hours, but most clients will spend 8 to 12 hours in total, including additional questions and meetings. This covers everything up to your first rent check. (For a more detailed description of our processes and services, click here.)

Other related questions:

- Do you need to come to Las Vegas to buy a property? No. If you’re in the U.S., the title company can send a mobile notary to you. This can also be arranged for clients in other countries (although some lenders may not allow this).

- What if I want to visit my property? I recommend seeing your first property in person. We’ll pick you up at the airport and take you to the property, where you’ll usually meet Selena (renovation manager), the property manager, and your account manager. We want you to know the team, since most clients buy multiple properties with us.

- How long does it take to buy additional properties? Usually much less time than the first. If it’s been a while, we’ll do a one-hour market update. Expect about two to three hours total per additional property.

- How much time will I spend each month? Most clients spend about 10 minutes a month reviewing their online portal. For any issues, contact the property manager first. If it’s not resolved quickly, contact me ([email protected]), and we’ll make sure it gets handled.

By focusing on a narrow property segment, we can provide you with a fairly accurate cash requirement. And due to our done-for-you services and heavy reliance on processes, your total time requirement to invest with us is minimal.

If you’re interested in exploring how the current Las Vegas market conditions could align with your goals, please use the link below to schedule a time that works best for you.

I wish you success.

Post: Looking to invest out of state into multi-family 4plex. I want to do a 1031 exchange.

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Cal Hollow,

I’ll comment in two parts: building a local investment team and multifamily investing.

Local Investment Team

Instead of starting from scratch, look for an experienced, established investment team. Begin by finding an investment realtor.

Most metro areas may have thousands of residential realtors, but they mainly provide MLS listings and property access to the properties you select. Residential realtors (or "investor-friendly") provide little or no value to an investor. I've bought several investment properties through residential realtors, and it took a lot of my time and cost more than necessary.

Investment realtors work with teams that handle everything—finding, validating, inspecting, renovating, and managing properties. Only an experienced team can provide all these resources. Residential realtors can’t.

While each team has its own unique approach, below is our process—you'll find that most investment teams operate in a similar fashion.

Finding and vetting an investment realtor can be challenging. In most areas, there may be only one or two investment realtors. If you want to know how to find and qualify one, let me know.

Multifamily

Multifamily properties are popular right now, but promoters rarely mention the downsides. Multi-family is similar to when Charles Lindbergh was advised to build a two-engine plane for his solo Atlantic flight in 1927. He did the calculations and determined that if he only had one engine operating, the plane would not fly for long. So the reality was that two engines doubled the risk without adding any value.

The same is true with multi-family. For example, with a four-plex, you have four units, which means four times the chance of vacancy compared to a single-family home. With even one unit vacant, you may not be able to cover your expenses. So the actual result is you have a high probability of losing money every month with a multifamily. Also, multifamily tenants are often singles or couples without children. Our research shows tenants with children choose single-family homes and perform better.

Our 17+ year results with 570+ single-family rentals:

- Only seven evictions in over 17 years, with more than 1,000 tenants

- Average tenant stays over five years

- Vacancy rate on 570+ properties is less than 2%

Don’t just follow trends—do your own research.

Post: August Las Vegas Rental Market Update

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

It's August, and it's time for another Las Vegas rental market update. For a more comprehensive look at the Las Vegas investment market, please DM me for a link to our blog. There, you'll find detailed information on investing, both in general and specifically in Las Vegas.

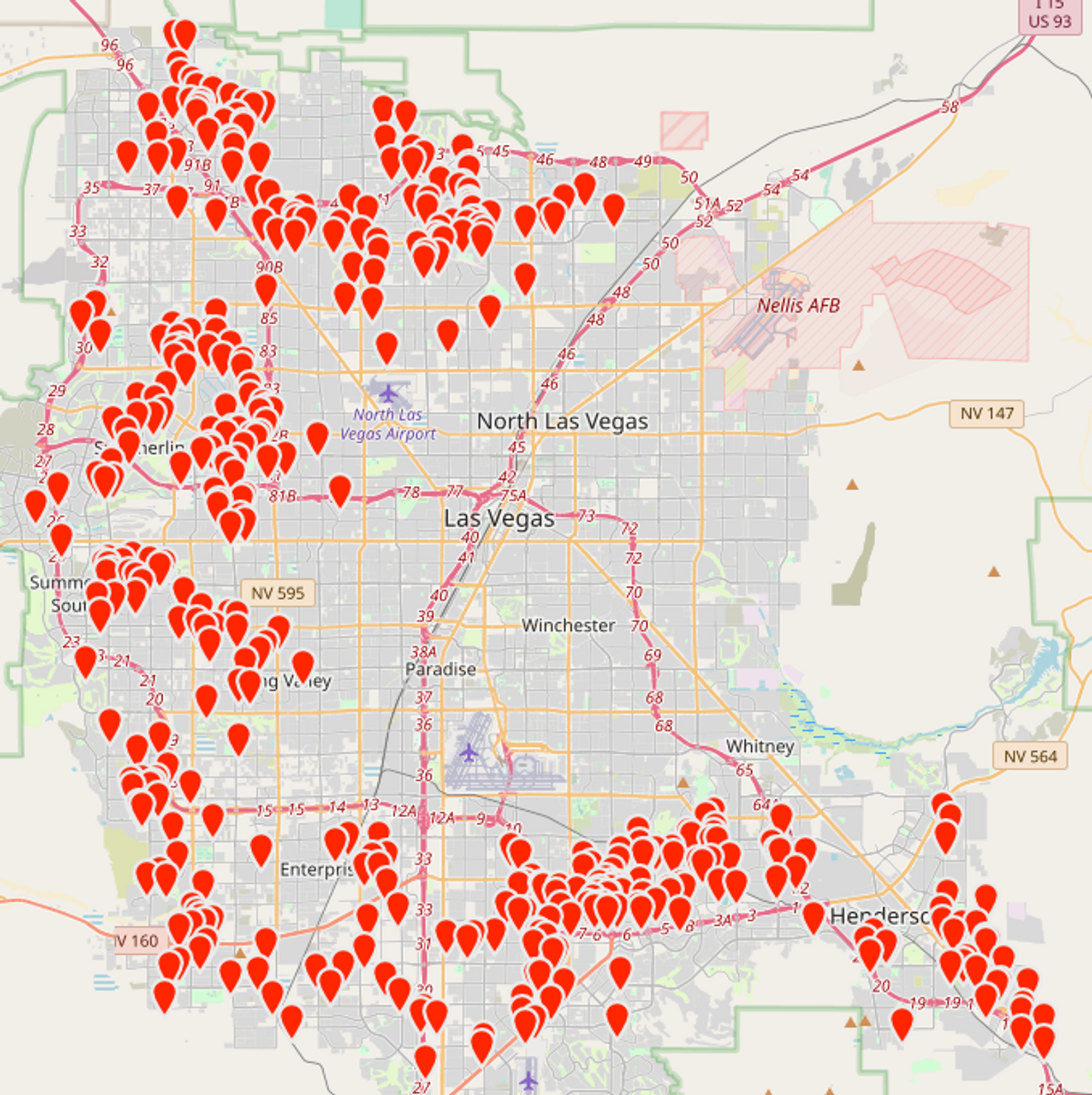

Before I continue, note that unless otherwise stated, the charts only include properties that match the following profile.

- Type: Single-family

- Configuration: 1,000 SF to 3,000 SF, 2+ bedrooms, 2+ baths, 2+ garages, minimum lot size is 3,000 SF.

- Price range: $320,000 to $475,000

- Location: See the map below

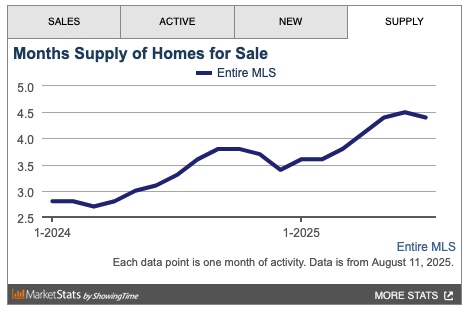

Overall Market Inventory

The chart below, from the MLS, includes ALL property types and price ranges. The overall inventory has stabilized and is now trending down.

“Bank-Owned Properties Rose 34% Nationwide”

I heard from some clients who had concerns about the "large number of distressed properties." Below is the actual MLS Las Vegas data for single-family homes in the Las Vegas metro area. (In 2023, there were 572,900 single family homes in the metro area.)

- Bank owned (REO): 9 for sale. (or 0.0016% of all homes)

- Short sales: 15 for sale. (or 0.0026% of all homes)

- Foreclosure started: 18 for sale. (or 0.0031% of all homes)

The article title was simply clickbait. Each location has its own unique market conditions, and national averages do not reflect the reality of any local market.

Rental Market Trends

The charts below are only relevant to the property profile that we target.

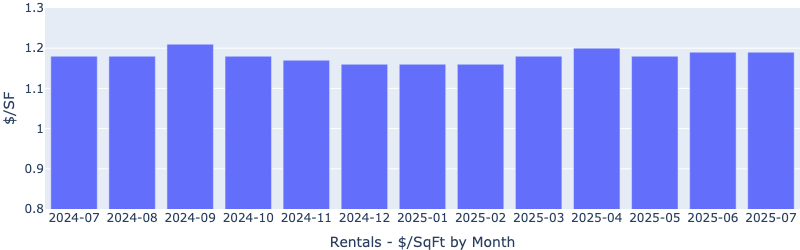

Rentals - Median $/SF by Month

Rents remained flat in June and July. Despite global tensions, rents remained reasonably stable.

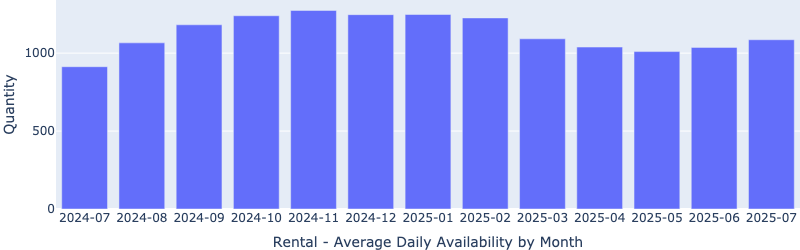

Rentals - Availability by Month

The number of homes for rent increased MoM in July, conforming to seasonal trend.

Rentals - Median Time to Rent

Time to rent increased MoM (from 20 days to 23 days), but remained healthy.

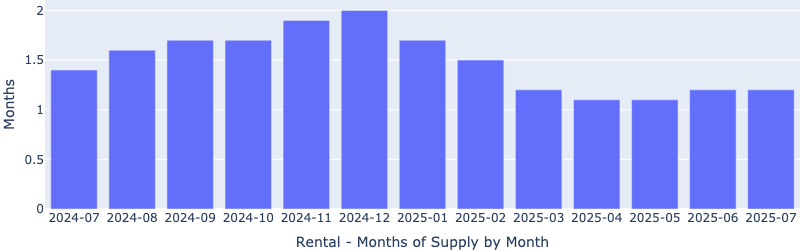

Rentals - Months of Supply

There are only 1.2 months of supply for our target rental property profile. This low inventory will continue to pressure up rents.

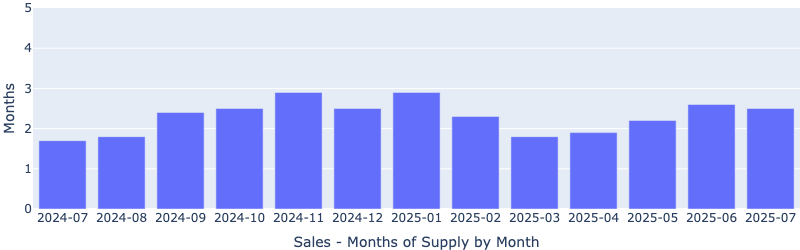

Sales - Months of Supply

Inventory decreased MoM to about 2.5 months. Six months is considered a balanced market where the number of buyers and sellers is roughly equal and prices remain stable. This is still a sellers market, despite the soundbites or clickbait you might hear or see in the media.

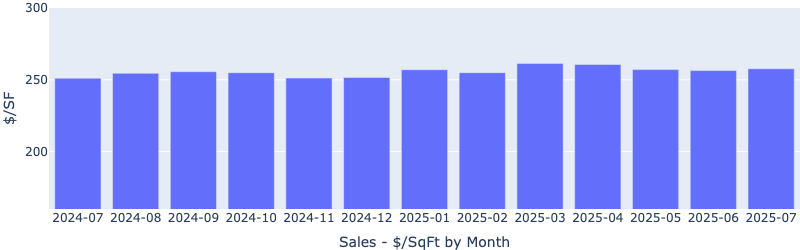

Sales - Median $/SF by Month

Despite all the volatility and alarming media headlines, the $/SF had a slight increase MoM. YoY is up 3%.

Why invest in Las Vegas?

The goal is to achieve and maintain financial freedom. Financial freedom means more than just matching your current income—it's about sustaining your lifestyle permanently. To accomplish this, you need income growth that exceeds inflation. Without this growth, you won't be able to keep up with the rising costs of goods and services.

What causes rents (and prices) to increase?

Supply & Demand

Unlike financial markets, real estate prices and rents are driven by supply and demand. What is the supply and demand situation in Las Vegas?

Supply

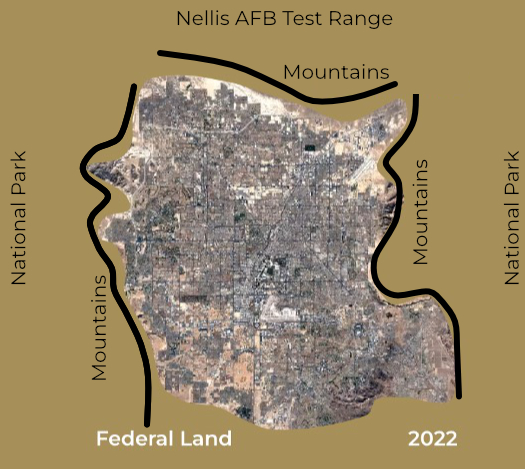

Las Vegas is unique because it is a tiny island of privately owned land in an ocean of federal land. See the 2022 aerial view below.

Very little undeveloped private land is left in the Las Vegas Valley, and desirable areas cost more than $1 million per acre. Consequently, new homes in these locations start at $550,000. Homes that appeal to our target tenant segment range from $350,000 to $475,000, so the supply of housing we target remains almost the same regardless of how many new homes are built.

Demand

Population growth drives housing demand and price and rent increases. Las Vegas's average annual population increases by 40,000 to 50,000 per year. What attracts people to Las Vegas? Jobs. Ongoing construction projects valued between $26 billion and $30 billion fuel both short-term and long-term employment opportunities. The most recent job fair featured over 20,000 open positions.

In Conclusion

While nothing is guaranteed, the combination of population growth and limited land for expansion virtually assures that prices and rents will continue to increase.

Thanks for reading my post. Reach out if you have questions or would like to discuss investing in Las Vegas.

Post: Where to invest?

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Dean Gustafson,

Whether the S&P 500 or another rental property is the best option for you depends on your financial situation and your goals. Real estate and stocks are very different; see below.

Stocks

The investment strategy with stocks (bonds, CDs, mutual funds, etc.) is to accumulate sufficient capital to enable monthly withdrawals that sustain your current standard of living throughout retirement. For example, if you need $10,000/month, and plan to withdraw funds for 30 years, and assume no inflation or market corrections (crashes), calculating the required initial capital is straightforward:

- $10,000/Mo x 12 Mo/Yr x 30 Yrs = $3.6M

This is an unattainable amount of capital for most people to accumulate. And, if there is inflation, you will need more initial capital. For example, if inflation averages 5%/Yr and there are no market corrections, you will need to accumulate over $8M.

Real Estate

Achieving financial independence through real estate is different. You accumulate sufficient rental income streams to replace your current income. And, if you invest in a city where rent increases faster than inflation, you will have the additional income to pay future inflated prices. Actually, inflation is beneficial. Your major expense (debt service) is fixed so as rents rise, your cash flow increases. Plus, if property prices rise rapidly, then you can reinvest the accumulated equity through cash-out refinance to buy additional properties. This is what I and many of my clients have done.

Another advantage of real estate is that you will not outlive your money. And, you have the additional advantage of creating generational wealth, plus many tax advantages. And, if you target the right tenant demographic, the rental income is dependable. For example, during the 2008 financial crash, our clients had no decrease in rent and no vacancies.

Achieving and sustaining financial independence totally depends on where you invest. If you invest in a good city, then:

- Rents will increase faster than inflation. This means that you will be able to maintain your current standard of living indefinitely.

- Prices will rise fast enough that you will be able to acquire additional properties using the accumulated equity through cash-out refinancing, thus requiring limited additional capital to achieve financial independence.

In summary, if your goal is liquidity, then stocks are your better option. If your goal is financial independence, buying additional properties in the right city is your best option.

Post: Multifamily mindset worth the cost?

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Umi Shafi,

There is a lot of confusing statements floating around. I had the same problem when I first set up my business. I read all the popular investment books and went to multiple investment seminars. To my surprise, all I discovered was a sea of self-professed “experts” touting their opinions as facts. They peddled clichés like “secrets the wealthy don’t want you to know.”

Frustrated, I turned to the commercial real estate world. National retailers base all their decisions on what their ideal customers want, not what retail management thinks. I adopted this retail strategy by first determining my ideal "customer."

My ideal “customer” stays for many years, pays rent on time, and takes good care of the property. Once I identified my customer, I determined what and where they were renting and bought similar properties. Every decision focused on attracting my ideal customer to meet my financial goals, not on my personal preferences or others' opinions. This could mean investing in any property type: high-rise, condo, multi-family, or single-family—it does not matter as long as it attracts your ideal customer.

The Multi-Family Fantasy

The multi-family "advantage" most commonly touted is that even with one vacant unit, you still have income from the others. However, this single vacancy often leaves insufficient cash flow to cover all expenses. In multi-family properties, the likelihood of having one or more vacant units is high. As a result, multi-family properties typically generate lower overall income than single-family properties occupied by reliable tenants. In my case, over 17+ years, with a property population of >560 properties, our vacancy rate has been <2%.

Multi-family properties also come with higher maintenance costs. In a 4-plex, you're responsible for four HVAC systems, four sets of plumbing, four sets of appliances, and so on. Every dollar lost to expenses is one less dollar in your pocket.

Another important consideration is that investors rarely sell performing assets. In my 17 years of completing hundreds of deals in Las Vegas, I have never seen an investor sell a property that was making money. Investors only sell properties when they are losing money. So, when you see a multi-family property for sale, it's almost certainly losing money.

Also, beware of paper returns. My first investment property was a C-class 4-plex in Houston that promised exceptional cash flow on paper. The reality was dramatically different. After accounting for vacancies, maintenance, evictions, tenant skips, and other unexpected costs, I was actually losing about $1,000 per month. Why did the previous owner sell? Because the property was losing money. In this case, the cause was both deferred maintenance and problematic tenants.

Summary

Real estate investing comes down to purchasing properties that align with your financial goals. These goals should drive all your investment decisions. Don't allow dogma or “conventional wisdom” push you toward investments that don't serve your financial objectives.

Post: Would you ever buy a STR if you know it won't break even on cash flow?

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Melissa J.

Whether buying a short-term rental (STR) that doesn't break even makes sense depends on your goals and financial situation. If you want to become a real estate professional, an STR can be the easiest way. Still, consider whether first-year tax benefits are enough to outweigh long-term losses.

Also, I don’t recommend buying a property only for short-term rental. Choose one that works as both a short- and long-term rental, so you won’t need to sell if you switch strategies.

Location matters. California is known for laws that favor tenants, and evictions can take up to a year. In other states, you can remove problem tenants in 17 to 45 days. Always research the legal environment before you invest.

Appreciation is crucial for financial independence. With steady appreciation, you can grow your portfolio using cash-out refinancing and minimal extra cash. Many of our clients and I have used this strategy, so it’s great you’re factoring in appreciation.

In summary:

- Buying a property for first year tax advantages depends on whether the tax savings offset long-term losses and the amount of time and effort you'll have to invest.

- Location is the most critical investment decision you'll make. You should invest in a city where existing home prices and rents consistently outpace inflation.

Post: When Is It Actually a Good Time to Sell Real Estate?

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Joseph Snyder,

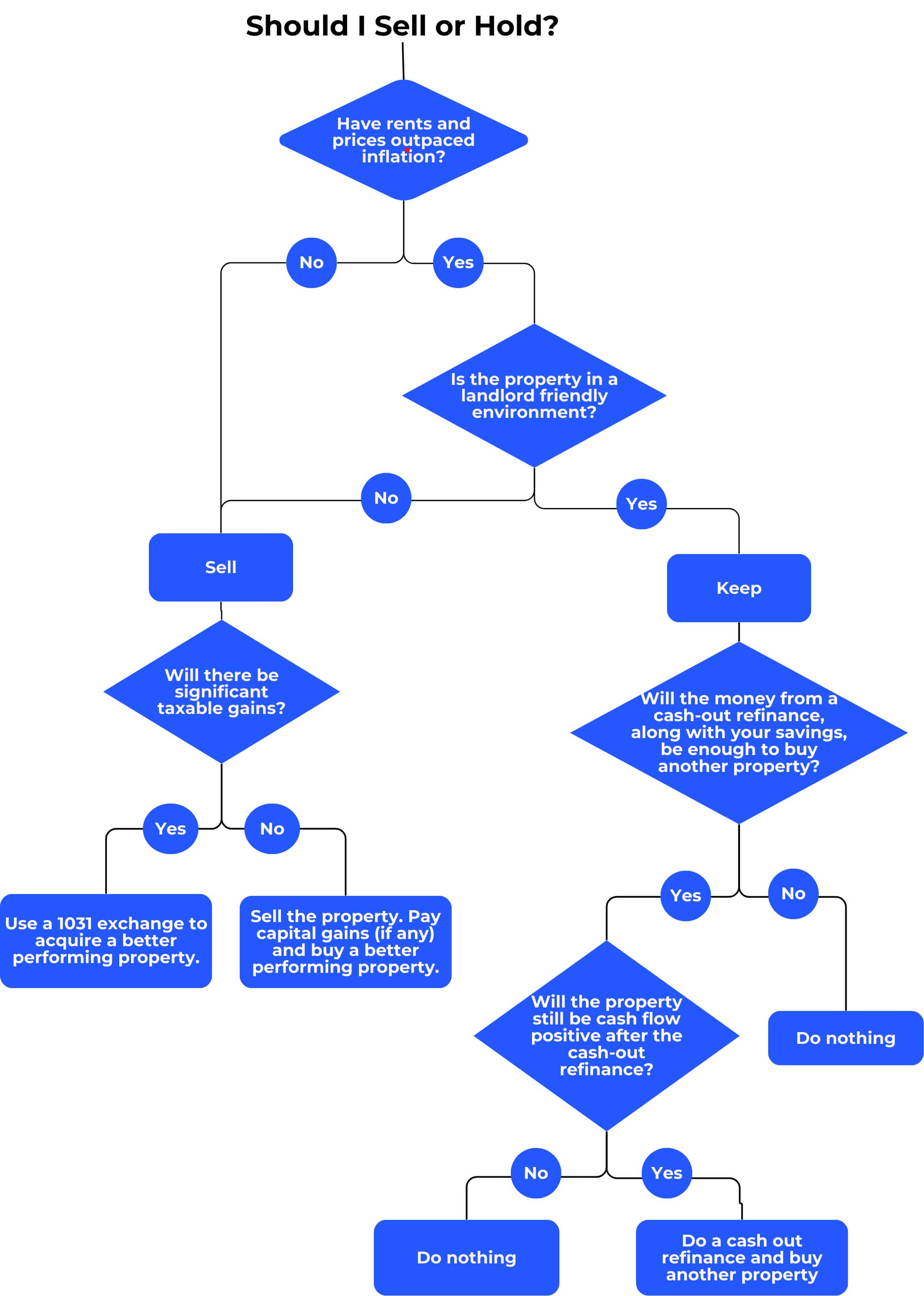

When it is a good time to sell depends on your financial goals. If your goal is financial independence, the decision process is relatively straightforward. I created the following decision tree which I hope you find useful.

In summary, there is no fixed date when you should sell. What you should do depends on the property's performance and your goals. If your goal is lifelong financial independence, then rents increasing faster than inflation is essential. Let the property’s performance and your goals make the sell/refinance/1031 decision.

Post: Why markets with low appreciation grow your net worth twice as fast

- Realtor

- Las Vegas, NV

- Posts 824

- Votes 1,574

Hello @Mike D.

If you're solely focused on immediate cash flow, cities with declining populations like Memphis (down 6% in the last 10 years) and Cleveland (down 7.6% in the last 10 years) typically offer the highest initial cash flow because properties are inexpensive. Why are properties inexpensive? Because there has been little demand for many years.

However, if you want lifelong financial independence, these markets won't work. Financial independence isn't about reaching a one-time number; it requires income that enables you to sustain your current standard of living for the rest of your life.

1. Rents Must Outpace Inflation

As living costs rise, your rental income needs to grow faster than inflation. In expensive cities, rising prices push more people to rent, increasing demand and rents. In low-cost, slow-growth cities, property prices and rents barely rise, so your income loses value over time. Meanwhile, expenses like taxes and insurance typically increase with inflation. At some point, your expenses will exceed your rental income.

2. Home Prices Must Appreciate Faster Than Inflation

In slow-growth markets, you must fund each purchase from your savings. For example, if you want $5,000 per month and each property nets $200, you need 25 properties. With a 25% down payment on $200,000 homes, that’s $1.25 million after taxes—unrealistic for most people. In rapidly appreciating markets, you can use equity from one property to buy the next, growing your portfolio with much less cash.

3. Rental Income Must Last a Lifetime

Tenants need stable, good-paying jobs to afford rent. In declining cities, companies leave, incomes drop, and city services like police and schools are cut due to falling tax revenue. Skilled and higher-income residents move away, causing a downward spiral of lower rents, higher vacancies, and shrinking property values.

4. Operating Costs

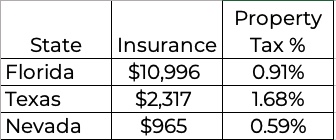

Operating costs vary tremendously by state. Below is a comparison between Nevada, Texas, and Florida.

- State average property tax source.

- Average insurance source.

- Florida's average insurance cost source

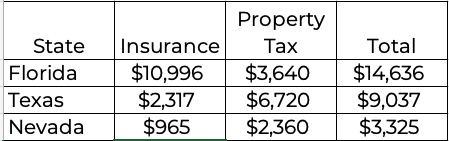

To put this in perspective, below are the estimated annual operating costs for a $400,000 property.

Compared to a property in Nevada, properties in other states require additional cash flow to compensate for their higher operating costs.

- Florida: +$11,311 ($14,636 - $3,325)

- Texas: +$5,712 ($9,037 - $3,325)

Summary

If you only care about initial cash flow, cities with declining populations like Memphis or Cleveland may meet your needs. But if you want lifelong financial independence, these markets cannot provide it, no matter how many properties you own.